| Year | Principal Paid | Interest Saved | Escrow Paid | Remaining Loan |

|---|

| Year | Standard Paid | Extra Injected | Interest Saved | End Loan Balance |

|---|

See how your savings can grow over time with our free Savings Calculator.

Table of Contents

- Introduction

- What Is an Online Mortgage Payoff Calculator?

- Why Every Homeowner Needs an Online Mortgage Payoff Calculator

- Key Features of a Reliable Online Mortgage Payoff Calculator

- How to Use an Online Mortgage Payoff Calculator Step by Step

- Understanding the Offset Account Model

- How the Payment Accelerator Works

- The True Cost of Your Mortgage: Breaking Down the Numbers

- How Extra Payments Can Save You Thousands

- Property Taxes, Insurance, and Their Role in Mortgage Planning

- Real-Life Scenarios Using an Online Mortgage Payoff Calculator

- Common Mistakes Homeowners Make When Planning Mortgage Payoff

- Strategies to Pay Off Your Mortgage Faster

- How Interest Rates Impact Your Payoff Timeline

- Frequently Asked Questions (FAQs)

- Conclusion

Introduction

Buying a home is likely the largest financial commitment of your life — and the mortgage attached to it can feel like a weight you will carry for decades. But what if you had a clear, precise tool that showed you exactly how to lighten that load, slash your interest payments, and walk away from your mortgage years ahead of schedule?

That tool is the Online Mortgage Payoff Calculator — and it is transforming the way homeowners approach their biggest financial obligation. Whether you are wondering how much you can save by adding a small extra payment each month, or you want to understand the full impact of your offset account, this calculator delivers answers instantly.

In this comprehensive guide, we will explore every aspect of mortgage payoff planning — from the mechanics of compound interest and offset accounts to accelerated payment strategies and real-world scenarios. By the end, you will know exactly how to use an Online Mortgage Payoff Calculator to take control of your home loan and build genuine financial freedom.

What Is an Online Mortgage Payoff Calculator?

An Online Mortgage Payoff Calculator is a digital financial tool that helps homeowners determine how quickly they can pay off their mortgage, how much interest they will pay over the life of the loan, and how different strategies — such as offset accounts or extra payments — can reduce both their loan term and total interest cost.

Unlike a basic loan calculator that simply shows monthly repayments, a well-built Online Mortgage Payoff Calculator goes much deeper. It models two distinct scenarios:

The Offset Account Model — This calculates how maintaining a balance in an offset account reduces the effective principal on which your interest is charged, thereby lowering your total interest payable and shortening your loan term.

The Payment Accelerator Model — This shows you exactly how making additional regular payments — weekly, fortnightly, or monthly — compresses your loan term and eliminates tens of thousands of dollars in interest.

Together, these two features make the Online Mortgage Payoff Calculator one of the most powerful and practical financial tools available to homeowners today.

Why Every Homeowner Needs an Online Mortgage Payoff Calculator

Most homeowners sign a 25 or 30-year mortgage and simply make the minimum required repayments for decades without ever questioning whether a smarter approach could save them years of payments and tens of thousands of dollars.

The Online Mortgage Payoff Calculator exposes the real cost of passive mortgage management — and reveals the enormous upside of proactive repayment strategies.

Here is why this tool is indispensable:

Clarity on your true interest cost. Over a 30-year mortgage on a $350,000 loan at 5.5%, you could pay more than $380,000 in interest alone — more than the original loan amount. An Online Mortgage Payoff Calculator makes this shocking reality visible and motivates homeowners to act.

Instant scenario comparison. Want to know what happens if you move $20,000 into your offset account? Or increase your monthly payment by $300? The Online Mortgage Payoff Calculator answers these questions in seconds.

Goal-oriented planning. If your goal is to be mortgage-free by age 55, you can work backwards in the calculator to find exactly what it takes to achieve that milestone.

Better financial decisions. Understanding the real numbers stops homeowners from making costly mistakes, such as investing surplus cash in low-yield accounts while ignoring the guaranteed return of reducing mortgage principal.

Key Features of a Reliable Online Mortgage Payoff Calculator

Not all calculators are built equal. A high-quality Online Mortgage Payoff Calculator should include the following essential features:

Loan principal input. The ability to enter your current outstanding mortgage balance, not just the original loan amount.

Offset account analysis. The offset module should calculate interest charged on the net balance (principal minus offset) and show both the standard and offset-adjusted repayment schedules side by side.

Payment acceleration options. The ability to model the effect of additional weekly, fortnightly, or monthly payments on your loan term and total interest.

Property tax and insurance inclusion. A complete Online Mortgage Payoff Calculator includes fields for annual property taxes and home insurance, giving you a true picture of your total housing cost — not just the loan payment.

Visual progress bars and charts. Graphical representations of interest paid versus interest saved make the numbers more intuitive and the impact of your decisions more visceral.

Year-by-year amortization table. A detailed schedule showing how much of each payment goes to principal versus interest, and how your balance decreases over time.

When all these features work together, the Online Mortgage Payoff Calculator becomes a complete mortgage management command center.

How to Use an Online Mortgage Payoff Calculator Step by Step

Using the Online Mortgage Payoff Calculator effectively is straightforward — but entering accurate data is critical for meaningful results. Follow these steps:

Step 1 — Choose your calculation mode. Select either the Offset Savings Model or the Payment Accelerator tab, depending on which strategy you want to analyze first.

Step 2 — Enter your loan amount. Input your current outstanding mortgage principal. This is the balance you owe today, not your original loan amount.

Step 3 — Fill in your interest rate. Use your current annual interest rate. If you are on a variable rate, consider running two scenarios — one at your current rate and one slightly higher — to stress-test your plan.

Step 4 — Set your loan term. Enter the remaining years on your mortgage, not the original term.

Step 5 — Add offset balance or extra payment details. For the offset model, enter your current offset account balance. For the accelerator model, enter the additional amount you plan to pay each period.

Step 6 — Include property taxes and insurance. Enter your annual property tax and home insurance costs for a complete monthly cost breakdown.

Step 7 — Click Calculate. The Online Mortgage Payoff Calculator will instantly produce your results — including total interest payable, interest saved, revised payoff date, and a full amortization schedule.

Step 8 — Experiment with scenarios. The real power of the Online Mortgage Payoff Calculator lies in scenario testing. Adjust your offset balance, increase extra payments, or change the interest rate and watch in real time how your payoff timeline and interest cost shift.

Understanding the Offset Account Model

An offset account is a transaction account linked to your home loan. The balance in this account is “offset” against your outstanding mortgage principal, meaning you only pay interest on the difference.

For example: If your mortgage principal is $350,000 and your offset account holds $45,000, you only pay interest on $305,000. At a 5.5% interest rate, this saves you roughly $2,475 in interest in the first year alone — and the savings compound over time as your offset balance grows.

The Offset Savings Model in the Online Mortgage Payoff Calculator quantifies these savings precisely. It calculates:

- Standard monthly repayment (without offset)

- Effective monthly repayment (with offset applied to principal)

- Total interest payable with the offset account active

- Absolute interest saved compared to having no offset account

- Years shaved off your loan term as a result of the offset

The key insight is that every dollar sitting in your offset account earns a guaranteed, tax-free “return” equal to your mortgage interest rate. For most homeowners, this is far better than any savings account rate available. The Online Mortgage Payoff Calculator makes this comparison concrete and compelling.

How the Payment Accelerator Works

The Payment Accelerator is one of the most powerful features of the Online Mortgage Payoff Calculator. It is based on a deceptively simple principle: paying more than the minimum required repayment, even by a small amount, dramatically reduces the total interest you pay and the time it takes to clear your loan.

Here is why it works so powerfully:

Every extra dollar of principal you pay reduces the balance on which future interest is calculated. This means less interest is charged in the next period, more of your next repayment goes to principal, and the cycle accelerates — a virtuous compounding effect working in your favor rather than the bank’s.

The Payment Accelerator in the Online Mortgage Payoff Calculator allows you to model:

- Additional monthly payments — what happens if you pay an extra $200, $500, or $1,000 per month

- Lump sum contributions — the impact of directing a bonus or inheritance directly to your mortgage

- Frequency changes — switching from monthly to fortnightly payments, which effectively makes one extra monthly payment per year

The results are often stunning. On a 30-year $350,000 mortgage at 5.5%, adding just $300 per month in extra payments can cut your loan term by over 7 years and save more than $80,000 in interest. The Online Mortgage Payoff Calculator shows you exactly this — so you can decide with full information whether the sacrifice is worth it.

The True Cost of Your Mortgage: Breaking Down the Numbers

Most homeowners focus only on their monthly repayment amount without ever looking at the total cost of their loan. The Online Mortgage Payoff Calculator forces this reality into view — and for many people, it is a genuine wake-up call.

On a 30-year mortgage of $350,000 at 5.5%:

- Monthly principal and interest payment: approximately $1,987

- Total repayments over 30 years: approximately $715,600

- Total interest paid: approximately $365,600

- Interest as a percentage of the loan: over 100%

In other words, you pay for your house twice over the life of a standard mortgage. Understanding this figure is the first and most important step toward using the Online Mortgage Payoff Calculator strategically.

Beyond principal and interest, the calculator also factors in:

Property taxes — an annual cost that varies by location but significantly adds to your total housing expense over time.

Home insurance — essential protection that adds to your monthly outgoings and must be included in any realistic budget.

When all these costs are visible in one place, the Online Mortgage Payoff Calculator gives you a genuinely complete picture of what homeownership actually costs — and what you stand to save with smart strategies.

How Extra Payments Can Save You Thousands

One of the most powerful revelations from the Online Mortgage Payoff Calculator is how small, consistent extra payments can compound into massive savings over time.

Consider these scenarios on a $350,000 loan at 5.5% over 30 years:

Scenario A — No extra payments: Pay $365,600 in total interest over 30 years.

Scenario B — Extra $200 per month: Save approximately $44,000 in interest and pay off the loan 4.5 years early.

Scenario C — Extra $500 per month: Save approximately $90,000 in interest and pay off the loan over 8 years early.

Scenario D — Extra $1,000 per month: Save over $130,000 in interest and reduce your loan term by more than 12 years.

The Online Mortgage Payoff Calculator makes these numbers concrete and personalised to your exact loan situation — so you can find the extra payment amount that balances your current cash flow with your long-term savings goal.

Property Taxes, Insurance, and Their Role in Mortgage Planning

Many homeowners focus exclusively on the principal and interest component of their mortgage and overlook the significant ongoing costs of property taxes and insurance. A complete Online Mortgage Payoff Calculator includes these fields to give you a true monthly cost figure.

Property taxes vary significantly depending on your location and property value. In the United States, average property tax rates range from under 0.5% to over 2% of assessed value per year. On a $350,000 home, this could mean anywhere from $1,750 to $7,000 per year, or $146 to $583 per month added to your housing cost.

Home insurance is not optional for mortgaged properties — lenders require it. Annual premiums typically range from $800 to $2,000 or more depending on your property size, location, and coverage level.

When these costs are included in the Online Mortgage Payoff Calculator, the true monthly cost of homeownership becomes clear — and budgeting for mortgage payoff acceleration becomes far more realistic and achievable.

Real-Life Scenarios Using an Online Mortgage Payoff Calculator

Example 1 — The Offset Account Maximiser: James and Linda have a $400,000 mortgage at 6% with 25 years remaining. They have $60,000 in savings sitting in a standard savings account earning 2%. They use the Online Mortgage Payoff Calculator to model moving this to an offset account and discover they would save over $75,000 in interest and cut 4 years from their loan. The decision is immediate and obvious once the numbers are clear.

Example 2 — The Accelerated Payer: Priya receives an annual bonus of $5,000. Rather than spending it, she uses the Online Mortgage Payoff Calculator to see the impact of directing this lump sum to her $280,000 mortgage each year. The results show she could pay off her loan 6 years early and save over $60,000 in total interest.

Example 3 — The Fortnightly Switch: Michael discovers through the Online Mortgage Payoff Calculator that switching from monthly to fortnightly repayments on his $300,000 mortgage effectively adds one full month’s payment per year. Over a 30-year term, this simple change saves him over $35,000 and cuts 2.5 years from his loan.

Common Mistakes Homeowners Make When Planning Mortgage Payoff

Even with the right tools, homeowners sometimes make avoidable errors. Here are the most common mistakes — and how the Online Mortgage Payoff Calculator helps you avoid them:

Focusing on the monthly payment rather than total cost. A lower monthly payment over a longer term often costs far more in total. Always check the total interest figure, not just the monthly repayment.

Neglecting the offset account. Millions of homeowners have offset accounts they barely use. Maximising your offset balance is one of the highest-return financial moves available to any mortgaged homeowner.

Making irregular extra payments without a plan. Sporadic lump sum payments help, but consistent extra payments create a more powerful compounding effect. Use the Online Mortgage Payoff Calculator to find a regular extra amount that works within your budget.

Not revisiting the calculator when interest rates change. If your rate rises or falls, your payoff timeline changes significantly. Always re-run your numbers after any rate adjustment.

Underestimating total housing costs. Leaving out property taxes and insurance creates a false sense of affordability. The Online Mortgage Payoff Calculator prevents this error by including all major cost inputs.

Strategies to Pay Off Your Mortgage Faster

Armed with the insights from the Online Mortgage Payoff Calculator, here are the most effective strategies for accelerating your mortgage payoff:

Maximise your offset account balance. Keep as much of your liquid savings in your offset account as possible. Every dollar offset saves you mortgage interest at your full loan rate — a guaranteed, tax-efficient return.

Switch to fortnightly repayments. This alone reduces your interest bill meaningfully and shaves years off your loan term with zero additional lifestyle sacrifice.

Round up your repayments. If your monthly payment is $1,987, round it up to $2,200. The extra $213 per month compounds powerfully over time.

Direct windfalls to your mortgage. Tax refunds, bonuses, and inheritance payments applied directly to your principal generate guaranteed returns equal to your interest rate.

Review and refinance regularly. If interest rates have dropped or your credit profile has improved, refinancing to a lower rate can free up cash for extra repayments. Use the Online Mortgage Payoff Calculator to model the impact before committing.

Avoid extending your loan term when refinancing. Restarting a 30-year clock to lower monthly payments is rarely a good long-term move. Check the total interest cost in the Online Mortgage Payoff Calculator before making this decision.

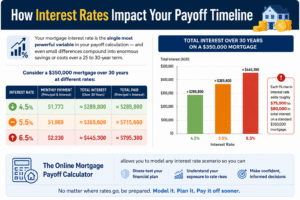

How Interest Rates Impact Your Payoff Timeline

Your mortgage interest rate is the single most powerful variable in your payoff calculation — and even small differences compound into enormous savings or costs over a 25 to 30-year term.

Consider a $350,000 mortgage over 30 years at different rates:

- At 4.5%: Total interest ≈ $289,800

- At 5.5%: Total interest ≈ $365,600

- At 6.5%: Total interest ≈ $445,300

Each 1% rise in interest rate adds roughly $75,000 to $80,000 in total interest on a standard $350,000 mortgage. This is why rate shopping, refinancing, and using every available offset or extra payment strategy matters so profoundly.

The Online Mortgage Payoff Calculator allows you to model any interest rate scenario so you can stress-test your financial plan, understand your exposure to rate rises, and make confident, informed decisions regardless of where rates go.

Frequently Asked Questions (FAQs)

What is the difference between an offset account and making extra repayments?

Both strategies reduce the interest you pay and shorten your loan term. An offset account keeps your money liquid — you can access it at any time — while extra repayments permanently reduce your loan balance. For homeowners who value flexibility, an offset account is usually the better choice. The Online Mortgage Payoff Calculator lets you compare both strategies side by side.

How much can I save by paying fortnightly instead of monthly?

Switching to fortnightly payments results in 26 half-payments per year, which equals 13 full monthly payments instead of 12. On a $350,000 loan at 5.5%, this can save over $35,000 in interest and cut approximately 2.5 years from your loan term. Run your specific numbers in the Online Mortgage Payoff Calculator for a precise figure.

Is it better to invest surplus cash or pay off my mortgage faster?

This depends on your mortgage interest rate versus expected investment returns, your tax situation, and your risk tolerance. If your mortgage rate is 5.5% or higher, paying off the mortgage is a guaranteed, risk-free return that is hard to beat. Use the Online Mortgage Payoff Calculator to quantify the mortgage payoff benefit before making this decision.

How does an offset account actually work?

An offset account is a savings or transaction account linked to your mortgage. The balance in this account is subtracted from your outstanding loan balance before interest is calculated each day. If you have $45,000 in your offset account and owe $350,000 on your mortgage, you only pay interest on $305,000. This significantly reduces your interest bill without locking away your money.

Can I use the Online Mortgage Payoff Calculator if I am on a variable rate?

Yes. Simply enter your current rate. It is also wise to run a second scenario with your rate 1-2% higher to understand how a rate rise would affect your payoff timeline and total interest cost. Good financial planning means stress-testing your assumptions — and the Online Mortgage Payoff Calculator makes this fast and easy.

Does paying off my mortgage early affect my credit score?

In most cases, paying off your mortgage early has a neutral to slightly positive impact on your credit score. It removes a large debt obligation from your profile, which can be beneficial. However, it also removes a long-standing account, which may slightly reduce your average credit age. The financial savings from early payoff typically far outweigh any minor credit score considerations.

How often should I revisit my payoff plan using the calculator?

At minimum, revisit the Online Mortgage Payoff Calculator once a year — or whenever your interest rate changes, your income increases, or you receive a lump sum you are considering applying to your mortgage. Regular reassessment ensures your strategy stays optimal as your circumstances evolve.

Conclusion

Your mortgage is not a fixed, immovable burden — it is a financial structure that responds powerfully to the strategies you apply. Whether you choose to maximise your offset account, make regular extra repayments, switch to fortnightly payments, or apply windfalls directly to your principal, the results can be life-changing: years of freedom gained and tens of thousands of dollars saved.

The Online Mortgage Payoff Calculator puts all of this insight at your fingertips. By entering your real numbers and experimenting with different scenarios, you move from a passive mortgage holder to an active, informed homeowner with a clear plan and a defined finish line.

The most important step is the first one — running your numbers and seeing the truth of your mortgage in full. Once you see what proactive strategies can achieve, the motivation to act follows naturally.

Use the Online Mortgage Payoff Calculator today. Model the scenarios. Find your strategy. And start building the financial future where your home is truly, completely yours.