FHA Loan Calculator

Calculate rental income, cash flow, and ROI with our Rental Property Calculator

Table of Contents

- Introduction

- What Is an FHA Calculator?

- Understanding FHA Loans and Why They Exist

- Who Qualifies for an FHA Loan?

- Key Inputs Every FHA Calculator Requires

- Breaking Down PITI – Your True Monthly Housing Cost

- Mortgage Insurance Premium (MIP) Explained

- Cash to Close – What You Actually Need on Closing Day

- Debt-to-Income Ratio and FHA Loan Approval

- The Amortization Schedule – Your 30-Year Repayment Roadmap

- FHA Loan Limits by Location

- How to Use Our FHA Calculator Step-by-Step

- FHA Loan vs. Conventional Loan – Key Differences

- Common FHA Loan Mistakes to Avoid

- Tips to Strengthen Your FHA Loan Application

- Frequently Asked Questions (FAQs)

- Conclusion

Introduction

For millions of Americans, homeownership feels financially out of reach — tight savings, imperfect credit, and the intimidating size of a conventional down payment create barriers that seem impossible to clear. The Federal Housing Administration created the FHA loan program specifically to remove those barriers and make homeownership accessible to more people. But before you apply for an FHA loan, you need to understand exactly what it will cost you — every month, at closing, and over the full life of the loan.

That is precisely what an FHA Calculator is designed to do. It takes all the financial variables of an FHA loan — purchase price, down payment, interest rate, mortgage insurance, property taxes, insurance, HOA fees, and all closing costs — and combines them into a complete, clear financial picture that shows you whether the loan is affordable and manageable for your specific situation.

In this comprehensive guide, you will learn everything about using an FHA Calculator to plan your home purchase intelligently. We will cover how FHA loans work, what makes them different from conventional mortgages, what inputs the calculator needs, how to interpret every output, and what steps you can take to put yourself in the strongest possible position before applying.

Whether you are a first-time homebuyer exploring your options or someone rebuilding after a financial setback, this guide — and our free FHA Calculator — gives you the knowledge and tools to move forward with confidence.

What Is an FHA Calculator?

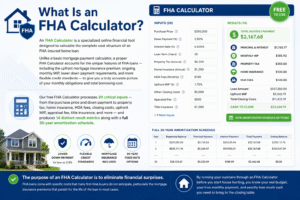

An FHA Calculator is a specialized online financial tool designed to calculate the complete cost structure of an FHA-insured home loan. Unlike a basic mortgage payment calculator, a proper FHA Calculator accounts for the unique features of FHA loans — including the upfront mortgage insurance premium, ongoing monthly MIP, lower down payment requirements, and more flexible credit standards — to give you a truly accurate picture of your monthly obligations and total borrowing cost.

Our free FHA Calculator processes 20 critical inputs — from the purchase price and down payment to property tax, home insurance, HOA fees, closing costs, upfront MIP, appraisal fee, title insurance, and more — and produces 14 distinct result metrics along with a full 30-year amortization schedule.

The purpose of an FHA Calculator is to eliminate financial surprises. FHA loans come with specific costs that many first-time buyers do not anticipate, particularly the mortgage insurance premiums that persist for the life of the loan in most cases. By running your numbers through an FHA Calculator before you start house hunting, you know your real budget, your true monthly payment, and exactly how much cash you need to bring to the closing table.

Understanding FHA Loans and Why They Exist

FHA loans are government-backed mortgages insured by the Federal Housing Administration, a division of the U.S. Department of Housing and Urban Development (HUD). Because the federal government insures these loans against default, private lenders are willing to extend mortgage credit to borrowers who would not qualify for conventional financing.

The FHA loan program was created in 1934 during the Great Depression to stabilize the housing market and expand homeownership access. Today it remains one of the most widely used mortgage programs in the United States, particularly among first-time buyers, low-to-moderate income households, and borrowers with less-than-perfect credit histories.

Key features that distinguish FHA loans from conventional mortgages:

Low Down Payment: FHA loans require a minimum down payment of just 3.5% of the purchase price for borrowers with a credit score of 580 or higher. Borrowers with scores between 500 and 579 may still qualify with a 10% down payment. This is dramatically lower than the 20% typically required for a conventional loan without PMI.

Flexible Credit Requirements: FHA loans accept credit scores as low as 500 in some cases — far more accommodating than the 620 to 640 minimum typically required for conventional financing.

Competitive Interest Rates: Because lenders bear less risk on FHA loans (due to government insurance), interest rates are often competitive with or lower than conventional loan rates — especially for borrowers with lower credit scores.

Mortgage Insurance Requirement: In exchange for these flexible terms, FHA loans require both an upfront mortgage insurance premium (UFMIP) and an ongoing annual mortgage insurance premium (MIP) — costs that an FHA Calculator helps you quantify precisely.

Who Qualifies for an FHA Loan?

Understanding the basic eligibility requirements helps you use an FHA Calculator more accurately, because the inputs you enter should reflect your real financial profile:

Credit Score: A minimum of 580 for 3.5% down payment; 500 to 579 for 10% down. Most lenders prefer 620 or higher for the most favorable terms.

Down Payment: As little as 3.5% of the purchase price. On a $300,000 home, that is $10,500 — a figure our FHA Calculator uses as its default to reflect a typical FHA purchase scenario.

Debt-to-Income Ratio: FHA guidelines generally allow a maximum DTI of 43%, though lenders may approve up to 50% with compensating factors such as significant cash reserves or a high credit score.

Employment History: Lenders typically require a minimum of two years of consistent employment history, preferably with the same employer or in the same field.

Primary Residence Requirement: FHA loans are only available for primary residences — not investment properties or vacation homes.

Loan Limits: FHA loan amounts are capped by county, with limits set annually by HUD. In most areas, the 2024 FHA loan limit for a single-family home is $498,257, with higher limits in high-cost markets.

Running your specific figures through an FHA Calculator — including your actual purchase price, credit score, income, and existing debts — is the fastest way to determine whether an FHA loan is financially viable for your situation.

Key Inputs Every FHA Calculator Requires

Our FHA Calculator is built around 20 input fields that collectively capture every financially significant aspect of your FHA loan scenario. Here is what each one means:

Purchase Price: The agreed sale price of the home you want to buy. This is the base figure from which your loan amount and down payment are derived.

Down Payment: For FHA loans, this is typically 3.5% of the purchase price (e.g., $10,500 on a $300,000 home). A larger down payment reduces your loan amount and may reduce your MIP duration.

Loan Term: FHA loans are available in 15-year and 30-year terms. A 30-year term is the most common, offering lower monthly payments. The FHA Calculator defaults to 30 years to reflect the most typical scenario.

Interest Rate: The annual interest rate on your FHA loan. FHA rates are competitive but vary by lender, credit score, and market conditions. Even a 0.25% difference has a significant impact over 30 years.

Property Tax: Your estimated monthly property tax. This varies widely by location and is included in your total PITI payment through escrow.

Home Insurance: Monthly homeowner’s insurance premium. Lenders require this coverage on all mortgaged properties.

Mortgage Insurance (Monthly MIP): FHA’s ongoing annual MIP, divided into monthly installments. For most FHA loans, this is 0.55% to 0.85% of the loan balance annually — a cost unique to FHA financing that significantly affects your monthly payment.

Credit Score: Your current FICO score affects your interest rate, MIP rate, and lender approval likelihood. Enter your actual score for the most accurate FHA Calculator results.

Annual Income: Your gross annual income, used to calculate your debt-to-income ratio and maximum qualifying loan amount.

Monthly Debts: All existing monthly debt payments — car loans, student loans, credit cards, personal loans. Combined with the new mortgage payment, this determines your DTI.

HOA Fees, Closing Costs, Upfront MIP, State Taxes, Utility Estimate, Repair Reserve, Admin Fee, Appraisal Fee, Survey Fee, and Title Insurance: These fields ensure every financial component of the FHA transaction is captured — providing a complete, realistic cost picture rather than an optimistic partial estimate.

Breaking Down PITI – Your True Monthly Housing Cost

One of the most critical outputs of our FHA Calculator is the Total PITI figure — and understanding what this means is essential for realistic budget planning.

PITI stands for Principal, Interest, Taxes, and Insurance — the four components that make up your complete monthly housing payment:

Principal: The portion of your monthly payment that reduces your outstanding loan balance.

Interest: The cost of borrowing, based on your loan balance and interest rate. In the early years of a 30-year FHA loan, interest represents the majority of each payment.

Taxes: Your monthly property tax obligation, typically collected by your lender through an escrow account and paid directly to the tax authority.

Insurance: Your monthly homeowner’s insurance premium, also typically escrowed by your lender.

For FHA loans, there is a fifth component that makes the total monthly cost higher than a conventional loan of the same size:

MIP (Mortgage Insurance Premium): FHA’s monthly mortgage insurance adds to your effective PITI, making the true comparison between FHA and conventional loans more nuanced than just comparing interest rates. The FHA Calculator adds MIP to your PITI automatically, giving you a fully loaded monthly housing cost figure.

Always evaluate affordability based on the Total PITI (including MIP), not just the principal and interest payment. Many first-time buyers budget for the P&I payment only to be surprised by the additional monthly costs. Our FHA Calculator prevents this by surfacing the complete monthly obligation upfront.

Mortgage Insurance Premium (MIP) Explained

No aspect of FHA financing confuses borrowers more than the Mortgage Insurance Premium, and no tool clarifies it better than a well-designed FHA Calculator.

FHA MIP comes in two forms:

Upfront Mortgage Insurance Premium (UFMIP): A one-time charge equal to 1.75% of the base loan amount, due at closing. On a $289,500 loan (a $300,000 purchase with 3.5% down), the UFMIP is approximately $5,066. This can be paid in cash at closing or rolled into the loan amount.

Annual Mortgage Insurance Premium (Annual MIP): Charged annually but paid in monthly installments as part of your mortgage payment. For most FHA loans originated after 2023, the annual MIP rate is 0.55% for 30-year loans with an LTV above 90%. This monthly MIP payment continues for the life of the loan if your down payment is less than 10%.

This lifetime MIP requirement is one of the most important differences between FHA and conventional loans. With a conventional loan, PMI (private mortgage insurance) can be cancelled once your equity reaches 20%. With an FHA loan, MIP typically persists for the entire loan term unless you refinance into a conventional loan after reaching sufficient equity.

Our FHA Calculator makes the monthly MIP cost explicit and includes it in your total monthly payment — so you can make a truly informed comparison between FHA financing and conventional alternatives.

Cash to Close – What You Actually Need on Closing Day

One of the most valuable outputs of our FHA Calculator is the Cash to Close figure — the total amount of money you need to bring to the closing table to complete your home purchase.

Cash to Close includes:

Down Payment: Your 3.5% (or more) FHA down payment contribution.

Closing Costs: FHA loans cap certain closing costs, but buyers are still responsible for a range of fees including lender origination fees, appraisal fees, title insurance, title search fees, survey fees, recording fees, prepaid interest, and escrow setup for taxes and insurance.

Upfront MIP: If you choose not to roll the upfront MIP into the loan, it must be paid at closing.

Prepaid Expenses: Lenders typically require the first year of homeowner’s insurance, several months of property tax, and prepaid mortgage interest to be paid at closing.

Total closing costs on an FHA loan typically range from 2% to 5% of the loan amount, in addition to the down payment. On a $300,000 purchase with the minimum down payment, total cash to close can easily exceed $18,000 to $24,000 — a figure that surprises many first-time buyers who only budgeted for the down payment.

Our FHA Calculator captures all of these cost components and adds them together in the Cash to Close output, ensuring you know exactly how much you need to have saved before moving forward with your home purchase.

Debt-to-Income Ratio and FHA Loan Approval

Your debt-to-income (DTI) ratio is one of the primary factors FHA lenders use to evaluate your ability to repay the loan, and our FHA Calculator computes it automatically based on your income and debt inputs.

DTI measures the percentage of your gross monthly income consumed by debt payments. FHA guidelines specify two DTI limits:

Front-End DTI (Housing Ratio): Your total monthly housing payment (PITI + MIP) divided by your gross monthly income. FHA guidelines prefer this to be 31% or lower, though lenders may allow up to 40% or more with strong compensating factors.

Back-End DTI (Total Debt Ratio): Your total monthly housing payment plus all other monthly debt obligations, divided by gross monthly income. FHA guidelines generally cap back-end DTI at 43%, though some lenders allow up to 50% with compensating factors such as strong credit or significant cash reserves.

If the FHA Calculator’s Debt-to-Income output shows a ratio above 43%, you have several options: increase your income, pay down existing debts before applying, choose a less expensive property, or make a larger down payment to reduce the monthly P&I payment.

Understanding your DTI before applying allows you to address any issues proactively — potentially saving your loan application from rejection and the credit inquiry from damaging your score unnecessarily.

The Amortization Schedule – Your 30-Year Repayment Roadmap

Our FHA Calculator generates a complete 30-year amortization table that shows how your FHA loan balance evolves year by year from origination to payoff. This schedule is one of the most powerful planning tools available to any homebuyer.

What the amortization schedule reveals:

Interest-Heavy Early Years: In the early years of a 30-year FHA loan, the majority of each payment goes toward interest rather than principal. This is a mathematical feature of amortization — and understanding it helps you appreciate why building equity is slow in the early years of homeownership.

Equity Growth Over Time: As the years progress, the principal portion of each payment increases and your balance decreases more rapidly. The amortization table makes this equity-building progression visible and tangible.

The Impact of Extra Payments: By reviewing where your balance stands in specific years, you can evaluate the benefit of making extra principal payments. Paying even one extra payment per year can shave years off the loan and save thousands in interest.

Total Interest Cost: Adding up the interest column across all 30 years reveals the true total cost of your FHA loan — a figure that often surprises first-time buyers. Seeing the full interest cost motivates smarter financial planning from day one.

FHA Loan Limits by Location

FHA loan limits are set by HUD annually and vary by county based on local median home prices. Understanding your local limit is important when using an FHA Calculator — entering a purchase price that exceeds the FHA limit for your area will produce results for a scenario that does not actually qualify for FHA financing.

For 2024, the standard FHA loan limit for a single-family home is:

Floor Limit (low-cost areas): $498,257

Ceiling Limit (high-cost areas): $1,149,825

Alaska, Hawaii, Guam, and U.S. Virgin Islands have even higher limits due to their unique high-cost housing markets.

To find the exact FHA loan limit for your specific county, visit the HUD website and look up your location. Then use that figure as the maximum loan amount in your FHA Calculator to ensure your analysis reflects what is actually available to you.

How to Use Our FHA Calculator Step-by-Step

Our free FHA Calculator is intuitive and comprehensive. Here is exactly how to get accurate, actionable results:

Step One – Enter Purchase and Loan Details: Input the purchase price of the home you are considering, your planned down payment (minimum 3.5% for FHA), the loan term (typically 30 years), and the interest rate you have been quoted or are estimating.

Step Two – Enter Monthly Housing Costs: Fill in your estimated monthly property tax, homeowner’s insurance premium, monthly mortgage insurance premium, and HOA fees if applicable. These amounts form the non-P&I portion of your PITI.

Step Three – Enter Your Financial Profile: Input your credit score, gross annual income, and total existing monthly debt payments. These three inputs drive the DTI calculation and help you evaluate whether you fall within FHA qualifying guidelines.

Step Four – Enter Closing Costs and Fees: Fill in all applicable closing cost fields — closing costs estimate, upfront MIP, state taxes, utility estimate, repair reserve, admin fee, appraisal fee, survey fee, and title insurance. This comprehensive fee section is what separates our FHA Calculator from basic payment tools.

Step Five – Click Calculate: Instantly view all 14 result metrics: Loan Amount, Down Payment, Monthly P&I, Monthly MIP, Monthly Tax, Monthly Insurance, Total PITI, Debt-to-Income, Cash to Close, Max Loan, Reserves, Net Income, Annual Cost, and Status.

Step Six – Review the Amortization Schedule: Examine the 30-year table to understand how your balance, principal payments, and interest payments evolve over time.

Step Seven – Experiment with Scenarios: Adjust the purchase price, down payment, or interest rate and click Calculate again to instantly see how each change affects your monthly payment, DTI, and cash to close. This scenario modeling is where the FHA Calculator delivers its greatest value.

FHA Loan vs. Conventional Loan – Key Differences

Before finalizing your financing choice, use the FHA Calculator to compare your FHA scenario against a conventional loan option. Here are the key differences that affect which is better for your situation:

| Feature | FHA Loan | Conventional Loan |

|---|---|---|

| Minimum Down Payment | 3.5% (580+ score) | 3% to 5% |

| Minimum Credit Score | 500 (10% down) / 580 (3.5% down) | Typically 620+ |

| Mortgage Insurance | Required for life of loan (if <10% down) | Cancellable at 20% equity |

| Loan Limits | Set by HUD county limits | Higher limits (conforming) |

| Property Requirements | Must meet FHA standards | Less restrictive |

| Seller Concessions | Up to 6% | Up to 3% (with <10% down) |

For buyers with strong credit (720+) and a 20% down payment available, a conventional loan is usually more cost-effective because it avoids mortgage insurance entirely. For buyers with lower credit scores or limited down payment savings, the FHA loan often provides access to homeownership that would otherwise be unavailable — and the FHA Calculator helps you quantify exactly what that access costs.

Common FHA Loan Mistakes to Avoid

Even with the advantages of FHA financing, several common mistakes can derail your home purchase or cost you significantly more money. Awareness of these pitfalls — and using an FHA Calculator to catch them early — is essential:

Underestimating the Total Monthly Payment: Many buyers focus only on the principal and interest payment and ignore taxes, insurance, and MIP. Always use the Total PITI output from the FHA Calculator as your true budget benchmark.

Ignoring the Upfront MIP: The 1.75% upfront mortgage insurance premium adds a significant amount to either your closing costs or your loan balance. Factor this into your cash planning using the FHA Calculator before assuming you have enough saved.

Choosing a Home That Fails FHA Appraisal: FHA loans require the property to meet specific health and safety standards set by HUD. Homes with structural issues, peeling paint (in older homes), roof problems, or other deficiencies may not pass FHA appraisal. This can kill deals or require sellers to make repairs.

Making Large Purchases Before Closing: Any major credit-affecting event between pre-approval and closing — buying a car, opening a new credit card, taking out a personal loan — can change your DTI ratio and jeopardize your loan approval.

Not Shopping Multiple FHA Lenders: FHA guidelines set the minimum standards, but individual lenders set their own rates and fees. Comparing offers from three or more lenders and running each through your FHA Calculator can save thousands of dollars.

Tips to Strengthen Your FHA Loan Application

A stronger application means better rates, faster approval, and more confidence. Here are the most effective strategies:

Improve Your Credit Score Before Applying: Pay down revolving credit balances below 30% of limits, dispute any inaccurate negative items, and avoid opening new accounts. Even moving from a 620 to a 680 score can meaningfully improve your FHA interest rate.

Save More Than the Minimum Down Payment: While 3.5% is the FHA minimum, putting more down reduces your loan balance, lowers your monthly MIP rate, and may shorten your MIP duration — all improvements you can model instantly in the FHA Calculator.

Reduce Your Monthly Debt Load: Paying off a car loan, a credit card balance, or a personal loan before applying can dramatically improve your DTI ratio — potentially the difference between approval and denial.

Document Your Income Thoroughly: FHA lenders require documented, verifiable income. Self-employed borrowers need two years of tax returns. W-2 employees need recent pay stubs and W-2s. Being prepared with documentation speeds up approval significantly.

Get Pre-Approved Before House Hunting: A pre-approval gives you a realistic, lender-verified budget and demonstrates to sellers that you are a serious buyer. Use the FHA Calculator to run your numbers first so your pre-approval search is focused and efficient.

Frequently Asked Questions (FAQs)

What is an FHA Calculator? An FHA Calculator is a specialized online tool that calculates the complete monthly cost of an FHA loan — including principal, interest, property taxes, homeowner’s insurance, and mortgage insurance — along with cash-to-close requirements, debt-to-income ratios, and a full amortization schedule.

Is the FHA Calculator free to use? Yes. Our FHA Calculator is completely free with no registration or account required. Enter your details and receive instant, comprehensive results.

What is the minimum down payment for an FHA loan? The minimum FHA down payment is 3.5% of the purchase price for borrowers with a credit score of 580 or higher. Enter your specific purchase price and down payment into the FHA Calculator to see how this affects your monthly payment and cash-to-close requirement.

How long do I pay mortgage insurance on an FHA loan? For FHA loans with a down payment of less than 10%, the annual MIP is charged for the entire life of the loan. For loans with a 10% or greater down payment, MIP is charged for 11 years. Our FHA Calculator includes MIP in every monthly payment projection.

What credit score do I need for an FHA loan? A minimum credit score of 580 is required for the 3.5% down payment program. Scores between 500 and 579 may qualify with a 10% down payment, though many lenders set their own minimums at 620 or higher.

Can I use gift funds for my FHA down payment? Yes. FHA guidelines allow the entire down payment to come from a documented gift from a family member or eligible donor. The gift must be documented with a signed gift letter.

What is the FHA loan limit in my area? FHA loan limits vary by county and are updated annually by HUD. For 2024, limits range from $498,257 to $1,149,825 depending on your location. Enter your specific loan amount into the FHA Calculator to ensure your scenario is within the applicable limit.

Can I refinance out of an FHA loan to eliminate MIP? Yes. Once you have built sufficient equity (typically 20%), you can refinance into a conventional loan to eliminate the ongoing MIP requirement. Use an FHA Calculator alongside a refinance calculator to determine when this transition makes financial sense.

What is Cash to Close on an FHA loan? Cash to Close is the total amount of money you need to bring to the closing table, including your down payment, closing costs, upfront MIP (if not financed), and prepaid expenses. Our FHA Calculator computes this figure automatically based on all your inputs.

Is an FHA loan better than a conventional loan? It depends on your financial profile. For buyers with lower credit scores or limited down payment savings, FHA is often the best available option. For buyers with strong credit and 20% down, conventional financing is typically more cost-effective due to the absence of MIP.

Conclusion

The dream of homeownership is achievable — even for buyers who do not have perfect credit or a large down payment. FHA loans exist specifically to make that dream possible, and millions of Americans have used them successfully to purchase homes they could not have financed any other way.

But understanding an FHA loan fully — every cost, every requirement, every monthly obligation — is the difference between a home purchase that builds wealth and one that becomes a financial burden. Our free FHA Calculator gives you that complete understanding before you ever speak to a lender, sign an application, or make an offer on a home.

By entering your purchase price, down payment, interest rate, income, debts, and all associated fees into the FHA Calculator, you get instant clarity on your true monthly payment, your debt-to-income ratio, your total cash to close, and a full 30-year amortization schedule showing exactly how your loan balance decreases over time.

Do not make one of the most important financial decisions of your life based on incomplete information. Use our FHA Calculator today, run your specific numbers, understand every cost, and take your first step toward homeownership with complete financial confidence.

Knowledge is the foundation of every great home purchase — and your FHA Calculator is where that knowledge begins.