Plan Smarter with Our Home Equity Loan Calculator

Table of Contents

- Introduction

- What Is a Pay Down Mortgage Calculator?

- Why Paying Down Your Mortgage Faster Changes Everything

- The Four Scenarios Our Calculator Covers

- Standard Down Payment – The Foundation of Every Purchase

- Investment Down Payment – Making Your Money Work Harder

- First-Time Buyer – Smart Entry Into Homeownership

- Luxury Down Payment – Managing Large-Scale Purchases

- Key Metrics Every Pay Down Mortgage Calculator Reveals

- Understanding Your Loan Amount vs. Down Payment

- How Monthly Costs Stack Up – Tax, Insurance, and Fees

- Strategies to Pay Down Your Mortgage Faster

- How to Use Our Pay Down Mortgage Calculator Step-by-Step

- Common Down Payment Mistakes That Cost You Thousands

- Frequently Asked Questions (FAQs)

- Conclusion

Introduction

Every mortgage payment you make is a step toward one of the most powerful financial milestones imaginable — the day you own your home free and clear, with no monthly payment, no lender, and complete financial freedom. But for most homeowners, that day feels impossibly distant. The path between your first mortgage payment and your last is long, and without a clear strategy and accurate numbers, most people simply follow the minimum payment schedule their lender set — often for 30 years.

A Pay Down Mortgage Calculator changes that. It shows you exactly where you stand, what your true costs are across every dimension of your purchase, and — most importantly — what happens when you accelerate your paydown strategy. Whether you are a first-time buyer, an experienced investor, or a luxury property owner, the numbers behind your down payment and mortgage structure determine your long-term financial trajectory.

In this comprehensive guide, you will learn how to use our free Pay Down Mortgage Calculator across four distinct purchase scenarios, understand every metric it produces, and implement proven strategies to pay off your mortgage faster and build equity more efficiently. The financial freedom that comes from owning your home outright begins with understanding your numbers today.

What Is a Pay Down Mortgage Calculator?

A Pay Down Mortgage Calculator is a multi-scenario financial tool that helps homeowners and prospective buyers calculate the full cost structure of a property purchase across different down payment strategies. It goes beyond simple payment calculation to reveal the complete financial picture — down payment amount, loan amount, extra acquisition costs, monthly obligations, insurance, taxes, fees, and more.

What makes a Pay Down Mortgage Calculator different from a basic mortgage calculator is its ability to model multiple purchase scenarios simultaneously. Standard purchases, investment properties, first-time buyer programs, and luxury real estate all have distinct cost structures, grant opportunities, income qualifications, and financial dynamics. A proper Pay Down Mortgage Calculator captures these differences and gives you scenario-specific insights.

Our free Pay Down Mortgage Calculator covers four distinct scenarios — Standard Down Payment, Investment Down Payment, First-Time Buyer, and Luxury Down Payment — each with eight carefully chosen input fields that capture every financially significant variable in that purchase type. The result is a clear, actionable summary of total price, down payment amount, loan amount, extra costs, monthly obligations, and total monthly commitment.

Why Paying Down Your Mortgage Faster Changes Everything

Your mortgage is likely the largest single debt of your life — and the interest you pay on it over 30 years can equal or exceed the original purchase price of the home. Understanding the financial magnitude of this is the first step to wanting to change it.

Consider a $200,000 mortgage at 5% interest over 30 years. Your monthly payment is approximately $1,074. Over 30 years, you pay a total of $386,640 — meaning you pay $186,640 in interest alone in addition to the $200,000 you borrowed. That is nearly as much as the home itself, paid purely for the privilege of borrowing.

A Pay Down Mortgage Calculator helps you see this reality clearly and then model what happens when you accelerate your paydown:

Extra Monthly Payments: Adding even $100 to $200 extra per month toward principal can shave years off your loan and save tens of thousands in interest. The Pay Down Mortgage Calculator makes the impact of extra payments immediately visible.

Lump Sum Payments: An annual lump sum payment — perhaps from a tax refund, bonus, or inheritance — applied directly to principal can dramatically reduce your loan balance and accelerate payoff.

Bi-Weekly Payment Strategy: Switching from monthly to bi-weekly payments means you make one extra full payment per year, reducing a 30-year loan to roughly 26 years without changing your lifestyle.

Larger Down Payment: Putting more money down at the start reduces the principal balance, lowers every subsequent payment, reduces total interest, and may eliminate PMI — all benefits quantified by a Pay Down Mortgage Calculator.

Refinancing to a Shorter Term: Moving from a 30-year to a 15-year mortgage increases monthly payments but dramatically reduces total interest and the time until you own your home outright.

The Four Scenarios Our Calculator Covers

Our Pay Down Mortgage Calculator is built around four real-world purchase scenarios, each representing a distinct type of buyer with different financial circumstances, goals, and cost structures:

Standard Down Payment: The most common purchase scenario — a primary residence with a conventional down payment typically between 10% and 20%. This is the baseline scenario for most homebuyers.

Investment Down Payment: A property purchased for rental income or appreciation, typically requiring a larger down payment (20% to 25%) due to lender requirements. This scenario includes renovation costs, rental income projections, vacancy rates, and management fees — variables that do not apply to primary residences.

First-Time Buyer: A purchase optimized for entry-level affordability, often featuring a lower down payment (3% to 5%), government grants, closing cost assistance, and income-based qualification constraints. This scenario is specifically designed to help new buyers understand how assistance programs affect their true financial picture.

Luxury Down Payment: A high-value property purchase requiring a larger absolute down payment and incorporating additional cost categories unique to luxury real estate — furnishings, premium fees, higher maintenance costs, and significant insurance premiums.

Using the Pay Down Mortgage Calculator across all four scenarios helps you understand not just your immediate purchase but the full spectrum of real estate investment options available to you.

Standard Down Payment – The Foundation of Every Purchase

The Standard Down Payment scenario is the starting point for most homebuyers and the most straightforward application of the Pay Down Mortgage Calculator.

Price: The purchase price of the home — the base figure for all calculations. All other values are derived from or added to this number.

Down Percentage: Expressed as a percentage of the purchase price. A 20% down payment on a $200,000 home means $40,000 down and a $160,000 loan. The Pay Down Mortgage Calculator converts this percentage instantly into dollar amounts, making the relationship between your down payment size and your loan amount immediately clear.

Rate: The interest rate on your mortgage. Even a 0.5% difference in rate has a substantial impact on total interest paid over 30 years. Always enter the actual rate you have been quoted, then experiment with slightly higher and lower rates to understand your sensitivity.

Years: The loan term. A 30-year loan has lower monthly payments but much higher total interest. A 15-year loan significantly increases monthly payments but dramatically cuts total interest. The Pay Down Mortgage Calculator lets you instantly compare these options.

Taxes, Insurance, HOA, and Other: These monthly cost fields complete your total monthly housing obligation — the true cost of owning the home, not just the mortgage payment. Never budget based on P&I alone; always include these items for an accurate picture of your monthly commitment.

The Standard Down Payment results reveal: Total Price, Down Payment in dollars, Loan Amount, Extra Costs, Monthly Tax, Insurance, Misc Fees, and Total Monthly Obligation — the complete financial summary of your purchase.

Investment Down Payment – Making Your Money Work Harder

The Investment Down Payment scenario transforms the Pay Down Mortgage Calculator into a rental property analysis tool, capturing the unique cost structure and income dynamics of investment real estate.

Price: The purchase price of the investment property. Investment properties typically trade at similar prices to comparable primary residences in the same market.

Down Percentage: Lenders typically require 20% to 25% down on investment properties — higher than primary residence requirements — to compensate for the increased default risk of non-owner-occupied properties.

Renovation: The cost to bring the property to rentable condition. Renovation costs are a critical investment calculation that many buyers underestimate. Even cosmetic renovations — paint, flooring, appliances — can easily reach $10,000 to $20,000 on an older property.

Closing Costs: Transaction costs including lender fees, title insurance, attorney fees, and recording fees. Investment properties typically carry the same closing costs as primary residences — 2% to 5% of the purchase price.

Rent: Projected monthly rental income. This is your top-line revenue figure, and it should be based on current market comparable rents — not optimistic projections.

Vacancy Rate: The percentage of time the property sits unoccupied between tenants or during slow rental periods. A realistic vacancy assumption of 5% to 10% is important for accurate cashflow modeling.

Management Fee: If you hire a property manager, their fee (typically 8% to 12% of monthly rent) must be subtracted from gross income to determine net rental income.

Tax: Annual property tax divided by 12, representing your monthly tax obligation as a landlord.

The Investment Down Payment results show you the relationship between your initial capital investment (down payment plus renovation plus closing costs) and your ongoing monthly costs — the foundation of any rental property cashflow analysis.

First-Time Buyer – Smart Entry Into Homeownership

The First-Time Buyer scenario in our Pay Down Mortgage Calculator is specifically designed for new homebuyers who are entering the market with limited savings, potentially lower down payments, and eligibility for various assistance programs.

Price: The purchase price — often lower for first-time buyers who are entering at the affordable end of the market.

Down Percentage: First-time buyers frequently use programs that allow 3% to 5% down payments. FHA loans require just 3.5% with a qualifying credit score of 580 or higher. The Pay Down Mortgage Calculator shows exactly what your loan amount will be at these lower down payment percentages.

Grant: Many state and local governments, as well as non-profit organizations, offer down payment assistance grants to first-time buyers. Entering your grant amount into the Pay Down Mortgage Calculator shows how this assistance reduces your out-of-pocket requirement and improves your financial position from day one.

Closing Costs: First-time buyers are sometimes eligible for seller concessions or lender credits that reduce closing costs. Enter your estimated net closing cost obligation after any credits.

Rate: Interest rate quoted for your specific loan product — FHA, conventional 3%, or other first-time buyer programs. Rates vary by program and credit score.

Income: Your gross monthly income — used to calculate your debt-to-income ratio, which determines the maximum loan amount for which you qualify.

Debts: Existing monthly debt payments that affect your DTI ratio and reduce your qualifying mortgage amount.

Tax: Monthly property tax obligation — an important component of total monthly housing cost that first-time buyers must account for in their budget.

Understanding the First-Time Buyer scenario through the Pay Down Mortgage Calculator helps new homeowners avoid the common trap of focusing only on the down payment while ignoring the full monthly cost picture.

Luxury Down Payment – Managing Large-Scale Purchases

The Luxury Down Payment scenario addresses the unique financial dynamics of high-value property purchases. When a home costs $1,000,000 or more, even a 30% down payment means $300,000 in cash — and the associated costs scale proportionally.

Price: The purchase price of the luxury property. Luxury real estate markets have their own dynamics, appreciation patterns, and financing structures.

Down Percentage: Luxury properties often require 30% or more down, both because jumbo loan requirements tend to be stricter and because higher-value properties carry more risk for lenders.

Furniture: High-end properties are often sold unfurnished or with minimal staging furniture. Furnishing a luxury home appropriately can cost $50,000 to $200,000 or more. The Pay Down Mortgage Calculator includes this as a distinct cost line because it is a real capital outlay that affects total acquisition cost.

Fees: Premium transaction fees, luxury transfer taxes (in some jurisdictions), attorney fees for complex transactions, and any concierge or advisory fees.

Tax, Insurance, Maintenance, and Other: At luxury price points, these monthly obligations scale significantly. A $1,000,000 home in a high-tax area might carry property taxes of $10,000 to $20,000 per year — costs that must be reflected in your monthly budget analysis.

The Luxury Down Payment results from the Pay Down Mortgage Calculator provide a comprehensive view of total acquisition cost and ongoing monthly obligations — essential for any high-net-worth buyer making a considered purchase decision.

Key Metrics Every Pay Down Mortgage Calculator Reveals

Each scenario in our Pay Down Mortgage Calculator produces eight standardized result points that together tell the complete financial story of your purchase:

Total Price: The full purchase price you are considering. This is your starting reference point.

Down Payment (in dollars): Your down percentage converted to a dollar amount. Seeing your down payment as a dollar figure — rather than a percentage — makes the cash requirement concrete and tangible.

Loan Amount: Total Price minus Down Payment. This is the principal balance you will finance and on which you will pay interest for the duration of the loan. Minimizing this number through a larger down payment is the most direct way to reduce total interest cost.

Extra Costs: The sum of any additional acquisition costs specific to your scenario — renovation and closing costs for investors, grants and closing for first-time buyers, furniture and fees for luxury buyers. These costs represent your true total capital deployment, not just the down payment.

Monthly Tax: Your monthly property tax obligation. Escrowed by most lenders, this is a non-negotiable recurring cost.

Insurance: Monthly homeowner’s insurance premium. Required by lenders and essential for protecting your asset.

Misc Fees: HOA dues, management fees, maintenance reserves, or other recurring monthly obligations specific to your purchase scenario.

Total Monthly: The sum of all monthly obligations — the true cost of owning the property each month. This is the most important number in the Pay Down Mortgage Calculator because it is the figure you must sustain indefinitely as long as you own the property.

Understanding Your Loan Amount vs. Down Payment

The relationship between your down payment and your loan amount is the central financial lever in any home purchase — and it is the relationship that a Pay Down Mortgage Calculator makes most clear.

Every additional dollar you put down reduces your loan amount by one dollar. But its impact extends far beyond that one-to-one relationship:

Interest Savings: A smaller loan means less interest over the entire loan term. On a 30-year loan at 5%, each $10,000 reduction in principal saves approximately $9,300 in total interest.

Monthly Payment Reduction: A lower loan amount reduces your monthly P&I payment immediately — improving your monthly cashflow from day one.

PMI Elimination: On conventional loans, a down payment of 20% or more eliminates the requirement for Private Mortgage Insurance (PMI), saving $50 to $200 per month on a typical loan.

Equity Position: A larger down payment means you start with more equity in the property — protecting you from going underwater if values decline and giving you immediate access to equity for future borrowing needs.

Better Rates: Higher down payments often qualify for better interest rates, further reducing total cost.

Use the Pay Down Mortgage Calculator to model different down payment percentages — 5%, 10%, 20%, 25% — and observe how each changes your loan amount, monthly payment, and total financial commitment. The results often reveal that stretching to a larger down payment, even if it requires delaying purchase by a few months to save more, produces dramatically better long-term financial outcomes.

How Monthly Costs Stack Up – Tax, Insurance, and Fees

One of the most common budgeting errors in home buying is planning based on the mortgage payment alone. In reality, your monthly housing cost includes several mandatory components that can add 30% to 50% to your base P&I payment:

Property Taxes: Collected monthly by most lenders through an escrow account, property taxes range from 0.5% to 2.5% of home value annually depending on your location. On a $300,000 home with a 1% tax rate, that is $250 per month — a substantial addition to your mortgage payment.

Homeowner’s Insurance: Required by all mortgage lenders, annual premiums for a $300,000 home typically range from $1,200 to $2,400. That is $100 to $200 per month added to your payment.

HOA Dues: Applicable to condominiums, townhomes, and many planned communities, HOA dues can range from $100 to several hundred dollars per month. These dues are non-negotiable and must be paid regardless of financial circumstances.

Maintenance Reserve: Even if not included in a formal monthly payment, setting aside a maintenance reserve is essential. Industry standard guidance is 1% of home value per year — or $200 per month on a $200,000 home.

Our Pay Down Mortgage Calculator includes fields for all of these costs and totals them into the Total Monthly figure — giving you the true, all-in monthly cost of homeownership for your specific situation rather than a misleading partial figure.

Strategies to Pay Down Your Mortgage Faster

Once you understand your mortgage structure through the Pay Down Mortgage Calculator, these proven strategies help you accelerate payoff and save significantly on total interest:

Make Bi-Weekly Payments Instead of Monthly: By making half your monthly payment every two weeks, you effectively make 13 full payments per year instead of 12. This simple change can pay off a 30-year mortgage in approximately 26 years with no other changes.

Round Up Your Payments: If your monthly payment is $1,247, round up to $1,300 or even $1,500. The extra amount goes directly to principal and accelerates your payoff timeline meaningfully.

Apply Windfalls to Principal: Tax refunds, work bonuses, inheritances, or any unexpected income applied directly to your mortgage principal can shave years off your loan term and save thousands in interest.

Refinance to a Shorter Term: When interest rates are favorable, refinancing from a 30-year to a 15-year mortgage significantly accelerates payoff. Use the Pay Down Mortgage Calculator alongside a refinance calculator to determine whether the increased monthly payment is sustainable within your budget.

Avoid Recasting Temptations: Some homeowners refinance repeatedly to extend terms and lower monthly payments. While this provides short-term relief, it significantly increases total interest cost and delays mortgage freedom. Commit to your paydown timeline and use the Pay Down Mortgage Calculator to keep your goals visible.

Make One Extra Full Payment Annually: Even one extra payment per year — perhaps using a year-end bonus — reduces total interest cost significantly and shortens the loan term by several years on a typical 30-year mortgage.

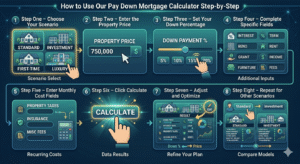

How to Use Our Pay Down Mortgage Calculator Step-by-Step

Our Pay Down Mortgage Calculator is intuitive and fast. Here is the complete step-by-step process for getting accurate, useful results:

Step One – Choose Your Scenario: Select the scenario that matches your purchase type — Standard Down Payment, Investment Down, First-Time Buyer, or Luxury Down Payment. Each scenario has input fields tailored to its unique financial dynamics.

Step Two – Enter the Property Price: Input the purchase price of the property you are evaluating. This is the base figure from which all other calculations flow.

Step Three – Set Your Down Percentage: Enter the down payment percentage you are planning or evaluating. Try multiple percentages — 5%, 10%, 15%, 20% — to see how each affects your loan amount and monthly cost.

Step Four – Complete the Scenario-Specific Fields: Fill in the remaining six fields for your chosen scenario — interest rate and loan term for Standard; renovation and rent for Investment; grant and income for First-Time; furniture and fees for Luxury.

Step Five – Enter Monthly Cost Fields: Fill in the tax, insurance, and miscellaneous fee fields specific to your scenario. These are critical for getting an accurate Total Monthly figure.

Step Six – Click Calculate: Instantly view all eight result metrics — Total Price, Down Payment, Loan Amount, Extra Costs, Monthly Tax, Insurance, Misc Fees, and Total Monthly.

Step Seven – Adjust and Optimize: Change your down payment percentage, adjust the price, or modify any field to model different scenarios. The Pay Down Mortgage Calculator makes it easy to find the purchase structure that maximizes affordability and minimizes long-term cost.

Step Eight – Repeat for Other Scenarios: Run the same property through a different scenario if applicable — for example, compare buying as a primary residence versus as an investment property to see which structure makes more financial sense.

Common Down Payment Mistakes That Cost You Thousands

Even well-prepared buyers make costly errors in down payment planning. Here is what to watch for — and how the Pay Down Mortgage Calculator helps you avoid each mistake:

Putting Down the Minimum Without Modeling the Cost: The minimum down payment keeps your savings intact but maximizes your loan amount, monthly payment, and total interest. Always use the Pay Down Mortgage Calculator to model 5%, 10%, and 20% down scenarios side by side before deciding on your down payment amount.

Draining Emergency Savings for a Larger Down Payment: A larger down payment improves your loan terms, but leaving yourself with no liquid emergency fund creates a different kind of financial risk. The best strategy balances down payment size with maintaining 3 to 6 months of expenses in accessible savings.

Ignoring Grant and Assistance Programs: Thousands of dollars in down payment grants and closing cost assistance are left unclaimed every year by first-time buyers who simply did not know about available programs. The First-Time Buyer scenario in the Pay Down Mortgage Calculator includes a grant field — make sure you research what is available in your area before assuming you need the full down payment from personal savings.

Overestimating Investment Property Rental Income: In the Investment Down Payment scenario, setting rent too high produces falsely optimistic cashflow projections. Always base rental income on actual comparable rents in the immediate neighborhood, not on what you need the rent to be.

Forgetting Closing Costs When Planning Cash to Close: Many buyers save the exact down payment amount and then discover at closing that they also need 2% to 5% of the purchase price in closing costs. Always budget for both down payment and closing costs when using the Pay Down Mortgage Calculator.

Frequently Asked Questions (FAQs)

What is a Pay Down Mortgage Calculator? A Pay Down Mortgage Calculator is a multi-scenario financial tool that calculates the total cost, down payment requirements, loan amount, and monthly obligations for different types of home purchases — helping buyers plan their down payment strategy and understand the full financial commitment of homeownership.

Is the Pay Down Mortgage Calculator free to use? Yes. Our Pay Down Mortgage Calculator is completely free with no account or registration required. Simply select your scenario, enter your figures, and receive instant detailed results.

How much should I put down on a home? The ideal down payment depends on your financial goals. A 20% down payment eliminates PMI and minimizes total interest. A lower down payment preserves cash but increases monthly costs. Use the Pay Down Mortgage Calculator to model different down payment amounts and find the right balance for your situation.

What is the difference between the four calculator scenarios? Each scenario is tailored to a different buyer type: Standard covers primary residence purchases, Investment covers rental property analysis, First-Time Buyer addresses entry-level purchases with grant opportunities, and Luxury covers high-value property purchases with premium cost structures.

Can the Pay Down Mortgage Calculator help me decide between renting and buying? Yes. By using the Total Monthly figure from the Pay Down Mortgage Calculator and comparing it to your current rent plus the opportunity cost of your down payment capital, you can make a more informed rent-vs-buy decision.

What is the minimum down payment for a conventional mortgage? Conventional mortgages are available with as little as 3% down for qualifying buyers, though PMI is required for down payments below 20%. FHA loans allow 3.5% down with a 580+ credit score.

How does my down payment affect my interest rate? A larger down payment generally qualifies you for a better interest rate because it reduces lender risk. Use the Pay Down Mortgage Calculator to model both the rate reduction and the lower loan balance to see the combined savings impact.

What is included in “Total Monthly” in the calculator results? Total Monthly is the sum of your monthly property tax, homeowner’s insurance, HOA dues (or management fees for investors), and any other recurring monthly costs entered in the scenario fields. This figure represents your true monthly housing cost beyond the mortgage payment itself.

How can I use this calculator to pay down my mortgage faster? Use the Pay Down Mortgage Calculator to understand your current loan structure, then model scenarios with larger down payments, shorter terms, or extra monthly contributions to see the impact on your payoff timeline and total interest cost.

Is the First-Time Buyer scenario only for buyers who have never owned a home? Most first-time buyer programs define “first-time buyer” as someone who has not owned a primary residence in the past three years — not necessarily someone who has never owned before. Always check your specific program’s definition when entering grant amounts into the Pay Down Mortgage Calculator.

Conclusion

Your mortgage is the largest financial commitment of your life — and every dollar of down payment you bring to the table, every extra payment you make, and every financially smart decision you take along the way compounds into either enormous savings or unnecessary cost over the decades ahead.

Our free Pay Down Mortgage Calculator gives you the tools to make those decisions wisely. Across four distinct scenarios — Standard Down Payment, Investment Property, First-Time Buyer, and Luxury Purchase — it captures every significant financial variable, converts them into clear result metrics, and shows you exactly what your purchase truly costs and what your monthly obligations will be.

Whether you are deciding how much to put down, comparing two properties, evaluating a rental investment, or planning your journey from first payment to final payoff, the Pay Down Mortgage Calculator is your essential financial companion. It replaces guesswork with precision, assumptions with data, and financial anxiety with informed confidence.

Use our Pay Down Mortgage Calculator today. Enter your numbers, explore your scenarios, understand your true costs — and take the first step toward the financial freedom that comes from owning your home on your terms.

Your path to mortgage freedom starts with knowing exactly where you stand — and that starts with the Pay Down Mortgage Calculator.