Certificate of Deposit (CD) Calculator

Plan your college budget and future education costs using our College Cost Calculator

Table of Contents

- Introduction

- What Is a CD Calculator?

- Why You Should Always Use a CD Calculator Before Investing

- Key Inputs in a CD Calculator Explained

- How to Use a CD Calculator Step by Step

- Understanding Your CD Calculator Results

- Compounding Frequency and How It Affects Your CD Returns

- How Taxes Impact Your CD Earnings

- Smart Strategies to Maximize Your CD Investment

- CD Calculator vs. Other Investment Calculators

- Common Mistakes to Avoid When Using a CD Calculator

- Frequently Asked Questions (FAQs)

- Conclusion

Introduction

When it comes to safe, predictable, and guaranteed growth of your savings, a Certificate of Deposit — commonly known as a CD — is one of the most trusted financial instruments available to everyday investors. Whether you are saving for a short-term financial goal, building a dedicated emergency reserve, or simply looking for a low-risk and stable place to park a portion of your wealth, CDs offer a level of security that most other investment options simply cannot match. But knowing exactly how much your money will grow — and precisely how much you will actually keep after taxes and fees — requires far more than just glancing at an advertised interest rate.

That is exactly where a CD Calculator becomes completely indispensable. A CD Calculator takes every single variable that affects your final return — your principal deposit, the interest rate, the compounding frequency, your applicable tax rate, any additional deposits made during the term, any withdrawals, and all account fees — and produces a precise, accurate, and detailed picture of what your investment will look like at the end of your chosen term.

This guide is your complete, in-depth resource for understanding, using, and extracting maximum value from a CD Calculator. Whether you are a first-time CD investor trying to understand the basics or a seasoned saver comparing multiple CD options across different institutions, the insights in this article will help you make smarter, more confident, and more profitable financial decisions. We will walk through every input field, every output result, every proven strategy, and every common mistake — so that you walk away with total clarity on how to use a CD Calculator to your greatest possible advantage.

Every smart CD investment begins with accurate calculations. And accurate calculations begin with a CD Calculator. The earlier you start running your numbers, the better positioned you are to maximize every dollar you deposit and every cent of interest you earn over the life of your investment.

What Is a CD Calculator?

A CD Calculator is a specialized digital financial tool designed to calculate the precise growth and final maturity value of a Certificate of Deposit investment over a specific period of time. It goes dramatically beyond simple interest arithmetic — it models the compounding of interest across multiple time periods, accounts for all taxes owed on interest earnings each year, factors in any additional deposits made during the CD term, subtracts any planned withdrawals or recurring account fees, and delivers a fully detailed, year-by-year breakdown of exactly how your investment performs from the opening deposit to the final maturity date.

A Certificate of Deposit is a time-deposit savings product offered by FDIC-insured banks and NCUA-insured credit unions. When you open a CD, you enter into a formal agreement to deposit a fixed sum of money for a predetermined period of time — commonly ranging from three months to five years — in exchange for a contractually guaranteed interest rate that is typically significantly higher than a standard savings account or money market account. At the end of the agreed term, called the maturity date, you receive your original principal plus all of the accumulated interest that compounded throughout the term.

The CD Calculator brings this entire process to life in precise, personalized numbers. Instead of simply being told that you will earn “5 percent per year,” you use the CD Calculator to see exactly how much gross interest you earn each year, how much tax you owe annually on those earnings, what your net after-tax balance looks like at the end of each year, and what your total final payout will be — net of all deducted fees and taxes across the full term of the investment.

A good CD Calculator also produces a visual chart and a year-by-year table, giving you both a high-level graphical view of your CD’s growth trajectory and a granular row-by-row breakdown of every dollar earned and every dollar deducted throughout the investment period. This combination of summary, visual, and detailed table output makes the CD Calculator the most comprehensive planning tool available for CD investors of any experience level.

For anyone considering a CD investment — regardless of the amount or the term length — running the full numbers through a CD Calculator before committing is not optional. It is essential. The difference between a CD that looks attractive on paper and one that genuinely delivers strong after-tax, after-fee returns can only be fully revealed by a thorough and accurate calculation.

Why You Should Always Use a CD Calculator Before Investing

Many investors make the common and costly mistake of selecting a CD based entirely on the advertised interest rate. They see “5.00% APY” on a bank’s website and automatically assume that a $10,000 deposit will generate exactly $500 in earnings every year. In reality, the actual outcome depends on several interconnected factors that the advertised rate never captures — and only a CD Calculator can reveal the complete financial truth.

Here is exactly why using a CD Calculator before every CD investment decision is a non-negotiable financial planning step:

It reveals your real after-tax return — the only number that truly matters. Interest earned on CDs is fully taxable as ordinary income at both the federal and, in most states, the state income tax level. A 5 percent gross interest rate does not mean you keep 5 percent. If your combined federal and state marginal tax rate on ordinary income is 30 percent, your effective after-tax return drops to approximately 3.5 percent. If you are in a higher combined bracket of 40 percent, it falls to just 3.0 percent. A CD Calculator shows you the exact after-tax dollars you will actually keep — which is the only return metric that genuinely reflects the growth of your real wealth.

It shows the precise impact of compounding frequency on your final balance. The same 5 percent annual interest rate produces meaningfully different final balances depending on whether interest is compounded annually, semi-annually, quarterly, monthly, or continuously. The CD Calculator calculates each compounding scenario with exact precision, allowing you to identify and select the CD that maximizes your actual dollar growth — not just the one with the highest quoted rate that may compound less favorably.

It quantifies the true cost of account fees over the full term. Many CDs carry annual maintenance fees, account administration charges, or other recurring costs. A CD Calculator subtracts these fees from your balance year by year and compounds that reduction forward, showing you clearly whether a higher-rate CD with annual fees actually outperforms a lower-rate CD with no fees — a comparison that is impossible to make accurately without running the full numbers.

It produces a detailed year-by-year growth roadmap for confident planning. Instead of vaguely wondering what your balance might look like in year 3 or year 5 of a long-term CD, the CD Calculator generates a complete table showing every year’s deposit, gross interest, tax paid, and net ending balance. This level of transparency is invaluable for coordinating your CD maturity dates with specific financial goals — a home down payment, a tuition bill, a business launch, or a retirement milestone.

It empowers direct, apples-to-apples comparisons between multiple CD offers. When you are choosing between a CD from Bank A offering 4.75% with monthly compounding and Bank B offering 5.00% with annual compounding and a $50 annual fee, intuition cannot reliably tell you which is better. The CD Calculator runs both scenarios simultaneously and shows you which specific combination puts more actual money in your pocket — after accounting for every real-world variable including taxes, fees, and compounding schedule.

It removes dangerous financial assumptions from your planning process. Many people assume that all 5% CDs are equal, that fees are too small to matter, or that monthly compounding makes no meaningful difference. The CD Calculator proves all of these assumptions wrong with precise numbers — replacing guesswork with mathematical certainty that protects your financial interests every single time.

Key Inputs in a CD Calculator Explained

Accurate inputs produce accurate results — and incorrect inputs produce dangerously misleading projections. Here is a thorough, detailed explanation of every field in a CD Calculator and exactly what each one means for the precision and reliability of your output:

Principal ($)

This is the initial lump-sum amount you deposit when you open the CD account. It is the foundation of your entire investment — the base upon which all compound interest will be calculated throughout the full term. CD minimum deposit requirements typically range from $500 to $10,000 at traditional banks, though many online banks and credit unions now offer CDs with no stated minimum. Always enter the exact dollar amount you are planning to commit — even modest differences in principal compound into meaningful differences in your final maturity balance over multi-year terms.

Rate (%)

The annual interest rate offered by the bank or credit union on the CD. Always verify whether the institution is quoting APR (Annual Percentage Rate) or APY (Annual Percentage Yield) before entering this figure into the CD Calculator. APY already incorporates the effect of compounding into the stated rate, while APR does not. The CD Calculator applies compounding mathematically based on your selected frequency — so entering APY alongside a non-annual compounding setting will artificially inflate your projected results. When in doubt, ask the institution for the APR specifically, or confirm what their base rate is before compounding is applied.

Years

The length of your CD term — the number of years you contractually agree to leave the money on deposit before accessing it. CD terms commonly range from 3 months to 5 years, though some institutions offer 7-year or even 10-year CDs for savers who want to lock in a favorable long-term rate. Longer terms generally carry higher offered rates in exchange for reduced access to your money during the term. Run the CD Calculator with multiple term lengths to see how significantly your final balance and total interest change across different commitment periods.

Tax (%)

Your effective marginal tax rate on interest income. In the United States, all CD interest is classified and taxed as ordinary income — at the same rates as wages and salary, not at the preferential capital gains rates applied to long-term stock investments. Enter your combined federal and state marginal rate for the most accurate after-tax projection. For most middle-income American households, this combined rate falls between 25 and 40 percent. If you are unsure of your exact rate, consult your most recent tax return or reference the current federal income tax bracket table. Never leave this field at zero.

Additional Deposits ($)

Some specialized “add-on CDs” permit you to make supplemental deposits during the term, allowing you to increase the principal balance earning interest as you go. Enter the annual dollar amount of additional deposits you plan to make if this feature applies to your CD. For the vast majority of standard fixed-term CDs — which do not permit additional deposits after the initial opening — enter zero in this field. Entering an incorrect amount here will significantly distort your projected end balance.

Withdrawals ($)

The annual dollar amount you plan to withdraw from the CD account during the term. Most standard fixed-term CDs impose significant early withdrawal penalties, so this field is primarily relevant for liquid CDs and no-penalty CDs that contractually permit withdrawals without penalty. Enter zero for a standard CD where you do not plan to access the funds before maturity. The CD Calculator subtracts any entered withdrawal amount from your annual balance before compounding the remaining balance forward into the next year.

Fees ($)

The total annual cost of all recurring account charges associated with your CD — maintenance fees, administration fees, wire transfer fees for interest distributions, or any other periodic charges disclosed in your account agreement. Even fees that seem trivially small compound negatively over a multi-year term. A $50 annual fee on a 5-year CD does not simply cost you $250 — it costs you $250 plus all the compounding growth those dollars would have earned if they had remained invested throughout the term. Always check the full fee schedule and enter all annual charges accurately.

Compounding Frequency

This is one of the two most impactful inputs in the entire CD Calculator — second only to the interest rate itself. Compounding frequency determines how often your accumulated interest is added back to your principal balance, enabling that larger balance to earn interest in the subsequent period. Standard options include:

- Annually — interest added to principal once every 12 months

- Semi-Annually — interest added twice per year, every 6 months

- Quarterly — interest added four times per year, every 3 months

- Monthly — interest added twelve times per year, every month

- Continuously — interest compounds at every theoretical instant using the exponential growth formula, producing the mathematically maximum possible growth for any given rate

More frequent compounding consistently produces a higher final balance, even when the stated annual interest rate is identical across all options. Always match this field precisely to what your bank specifies in the CD’s written agreement — not what you assume or prefer.

How to Use a CD Calculator Step by Step

Using a CD Calculator effectively requires a thoughtful, methodical approach to ensure your results are as accurate and actionable as possible. Follow these steps in sequence for the most reliable outcomes:

Step 1 — Research and gather your CD details before touching the calculator. Before entering any numbers, visit the official website of the bank or credit union you are evaluating and note the complete CD disclosure: the exact annual interest rate as APR, the compounding frequency, the full term length, the minimum deposit required, any annual account fees, and the early withdrawal penalty terms. Having all of these verified details ready before you open the CD Calculator ensures that your inputs reflect contractual reality, not assumption.

Step 2 — Enter your exact principal amount. Type the precise dollar amount you are planning to deposit as your opening balance. Use your actual committed investment amount — not a round number chosen for convenience. The CD Calculator compounds every dollar from day one, so accuracy in the principal field directly affects every subsequent calculation throughout the full term projection.

Step 3 — Enter the annual interest rate as APR. If the institution has provided you the APY rather than the APR, and you are using a compounding frequency other than annual, convert the APY to APR using the standard conversion formula before entering it. Entering APY into the rate field while simultaneously selecting monthly compounding will double-count the compounding effect and significantly overstate your projected balance — one of the most common and consequential errors in CD Calculator usage.

Step 4 — Set the term length in years. Enter how many years you plan to hold the CD to full maturity. If you are comparing a 2-year CD against a 4-year CD, run the CD Calculator separately for each term and compare the resulting end balances, total after-tax interest, and annual effective return side by side to make a fully informed term selection based on data rather than instinct.

Step 5 — Enter your realistic tax rate. Use your best informed estimate of your effective combined marginal tax rate for ordinary income — federal plus state. For taxable accounts, never leave the tax field at zero — doing so produces pre-tax results that overstate your actual take-home earnings by a significant margin. For CDs held inside a Traditional IRA or Roth IRA, the tax treatment differs significantly and you should consult a tax professional for guidance on that specific scenario.

Step 6 — Enter additional deposits, withdrawals, and fees accurately. For standard fixed-term CDs, additional deposits and withdrawals are typically zero. For any CD with disclosed annual fees, enter that exact annual amount. Even a small fee entered accurately significantly improves the real-world precision of your CD Calculator results by compounding that cost correctly forward through every year of the projection.

Step 7 — Select the correct compounding frequency. Choose the compounding schedule from the dropdown that exactly matches what your CD’s written agreement specifies. Do not select monthly compounding if the bank actually compounds quarterly — matching this field to the bank’s actual practice is essential for accurate results and meaningful comparisons across institutions.

Step 8 — Click Calculate and review every element of the output fully. The CD Calculator will instantly display your projected end balance, total gross interest, total taxes paid, and total after-tax net interest. It will also generate a visual bar chart and a detailed year-by-year breakdown table. Study all of these outputs completely — do not stop at reading only the final balance number. The annual table in particular reveals how your balance grows over time and exposes years where fees or taxes create meaningful drag on your compounding trajectory.

Step 9 — Run multiple comparison scenarios before making any final decision. Repeat the full calculation process with inputs from every competing CD offer you are evaluating. The genuine power of a CD Calculator is realized when you use it comparatively — running three, four, or five complete scenarios side by side to identify which specific combination of rate, term, compounding frequency, and fee structure delivers the strongest real-world, after-tax, after-fee outcome for your specific financial situation.

Understanding Your CD Calculator Results

The CD Calculator produces several distinct categories of output, each illuminating a different and important dimension of your investment’s performance. Understanding what every number means ensures you draw accurate conclusions and make well-informed decisions about every CD commitment.

End Balance is the total dollar amount you will receive when your CD reaches its maturity date — your original principal plus all net interest earned throughout the term, plus any additional deposits made, minus all withdrawals and fees deducted over the full term. This is the single most important number the CD Calculator produces. It represents the actual payout you will receive — the real, concrete result of your entire CD investment strategy.

Total Interest is the gross cumulative total of all interest earned across every year of the CD term, calculated before any taxes or fees are subtracted. This number reflects the raw earning power of your CD at the stated rate and selected compounding frequency in isolation. It is useful for understanding how much gross interest your money generated and for comparing the productivity of different rate and compounding combinations on equal terms without the variable of tax rates.

Total Tax is the cumulative total of all income taxes owed on your CD interest earnings across the complete term. This is the most consistently underestimated cost in CD investment planning. For a high-income earner subject to a combined 38 percent federal and state rate, taxes alone can consume more than one-third of every dollar of gross CD interest earned. The CD Calculator makes this invisible cost visible and precisely quantified — year by year — so it can never sneak up on you.

Interest After Tax is the real, genuine return on your CD investment — the net interest dollars you actually add to your wealth after the government has taken its statutory share. This is the number you must use in every comparison — not gross interest, not the advertised annual rate, but actual after-tax dollars earned. A CD with a higher gross rate but held in a higher tax bracket may deliver fewer after-tax dollars than a CD with a slightly lower rate held in a tax-advantaged account — and only this figure reveals that critical truth.

The Year-by-Year Breakdown Table produced by the CD Calculator shows five data points for every year of the term: the year number, the additional deposit contributed that year, the gross interest earned that year, the tax paid on that year’s interest earnings, and the ending balance after all additions and deductions are applied. This table is the most analytically rich output the calculator produces. It allows you to see exactly when your balance crosses specific financial milestones, how your annual interest earnings grow as the compounding balance increases, and how taxes and fees gradually interact with your growth trajectory year after year.

The Visual Growth Chart stacks your annual additional deposit contribution and net interest side by side for every year of the term, providing an immediate visual impression of how your investment grows over time and what proportion of each year’s growth comes from compounding interest versus fresh capital contributions. The chart is particularly useful for quickly communicating your CD’s growth story to a spouse, co-planner, or financial advisor who may benefit more from a visual representation than a numerical table filled with precise figures.

Compounding Frequency and How It Affects Your CD Returns

Compounding frequency is one of the most consequential and most frequently misunderstood variables in CD investing — and the CD Calculator makes its precise financial impact completely clear with exact dollar figures.

Compounding is the mathematical process by which earned interest is added to your principal balance at the end of each compounding period, after which that larger, newly increased balance earns interest during the next period. The more frequently this cycle repeats within a given year, the faster your balance grows — even when the stated annual interest rate is completely identical across all compounding options being compared.

Here is a concrete, real-world example using a $10,000 CD at 5.00 percent for a 5-year term, with no taxes, no fees, and no additional deposits:

- Annual compounding (once per year): Final balance = $12,762.82

- Semi-annual compounding (twice per year): Final balance = $12,800.85

- Quarterly compounding (four times per year): Final balance = $12,820.37

- Monthly compounding (twelve times per year): Final balance = $12,833.59

- Continuous compounding: Final balance = $12,840.25

The difference between annual and monthly compounding in this example is $70.77. While that may seem small on a $10,000 deposit, scale this to a $100,000 deposit and the difference becomes $707.70 — the equivalent of more than two months of additional interest earned purely from the compounding schedule difference, with no change in rate whatsoever. Scale to $500,000 and the difference exceeds $3,500 in additional earnings.

When evaluating CD offers from competing institutions, never compare stated rates directly without also accounting for each institution’s compounding schedule. A CD offering 4.90 percent with monthly compounding may actually generate a higher final balance than a CD offering 5.00 percent with annual compounding — and only the CD Calculator will reveal this comparison with precision. Many investors unknowingly select the worse CD simply because they compared headline rates without running the actual numbers.

Continuous compounding, available from some institutions, applies interest mathematically at every theoretical instant using the exponential formula A = Pe^(rt). While the real-world difference between monthly and continuous compounding is relatively small for most deposit sizes and standard CD terms, continuous compounding is always the highest possible return for any given stated rate — and the CD Calculator calculates it precisely using the mathematical constant e.

The practical takeaway is straightforward: when comparing CDs, always enter each institution’s actual compounding frequency into the CD Calculator separately for each option. Never assume that the CD with the highest quoted rate is automatically the best performer — only the after-compounding, after-tax, after-fee end balance tells the complete and honest story.

How Taxes Impact Your CD Earnings

Taxes are the single most overlooked and underestimated factor in CD investment planning, and the CD Calculator directly addresses this by incorporating your tax rate into every year of the projection with full compounding accuracy.

In the United States, all interest earned on CDs is classified as ordinary income for federal tax purposes. This means it is taxed at your marginal income tax bracket rate — the same rate applied to your wages, salary, self-employment income, and business earnings — rather than at the significantly lower long-term capital gains rates that apply to stocks or real estate held for more than one year. For most working American households, the federal marginal tax rate on CD interest income falls between 22 and 32 percent. When state income taxes are added — which apply in most states — the combined effective tax rate on CD interest commonly ranges from 25 to 40 percent or higher for upper-middle-income earners.

The practical financial effect of this tax treatment is substantial and compounds negatively over multi-year CD terms. A CD earning 5.00 percent gross annual interest does not deliver 5.00 percent to your net worth after taxes. At a combined federal-plus-state effective rate of 30 percent, your true after-tax return on that CD is approximately 3.50 percent. At a combined rate of 40 percent, your real after-tax return falls to just 3.00 percent — a 40 percent reduction in the effective yield of an investment you selected specifically for its guaranteed, predictable return.

The CD Calculator handles this tax reduction automatically and with compounding accuracy. When you enter your tax rate, the tool calculates the tax owed on each year’s gross interest, deducts that tax from the year’s earnings, and then compounds only the net after-tax interest forward into the following year’s balance. This produces a genuinely accurate after-tax compounding projection — not an optimistic pre-tax estimate that flatters the investment with returns you will never actually receive in your bank account.

A critical strategic implication of CD tax treatment is the substantial value of holding CDs inside tax-advantaged accounts. Placing a CD inside a Traditional IRA defers all taxes on interest earnings until withdrawal — which may occur during a lower-income retirement period when your marginal rate is reduced, significantly improving your net return over the full investment lifecycle. Placing a CD inside a Roth IRA allows interest to accumulate completely tax-free, with qualifying withdrawals also fully tax-free — potentially the most financially advantageous structure available for long-term CD savers.

Use the CD Calculator to calculate your after-tax return in a standard taxable account, then compare that figure against the projected tax-advantaged growth of the same CD held inside an IRA wrapper. The dollar difference this comparison reveals can represent thousands of dollars over a disciplined, long-term CD investment strategy — and making that comparison accurately requires the precise after-tax modeling that only a proper CD Calculator can provide.

Smart Strategies to Maximize Your CD Investment

Once you have mastered the CD Calculator and fully understand your personalized projections, these proven strategies will help you extract maximum value from every dollar you commit to CDs:

Build a comprehensive CD Ladder for optimal liquidity and continuous rate access. A CD ladder is a structured strategy where you split your total available CD investment across multiple CDs with staggered maturity dates — for example, allocating equal amounts to 1-year, 2-year, 3-year, 4-year, and 5-year CDs simultaneously. When each shorter-term CD matures, you reinvest the full proceeds — principal plus all accumulated interest — into a new 5-year CD at whatever the prevailing interest rate is at that time. Within five years, your entire investment is concentrated in 5-year CDs carrying the highest available rates, while one CD matures every single year, giving you regular, predictable access to funds without paying early withdrawal penalties. Run each individual rung of your ladder through the CD Calculator to project its precise growth, then combine the results to understand your full ladder’s total performance and annual cash flow.

Always compare every CD offer using the CD Calculator before committing to any institution. Interest rates, compounding schedules, and fee structures vary widely across traditional banks, online banks, and credit unions. Online banks and credit unions frequently offer CD rates significantly higher than those at traditional brick-and-mortar banks — sometimes by a full percentage point or more. That 1 percent difference, compounded over 5 years on a $50,000 deposit, can represent more than $2,500 in additional after-tax earnings. Use the CD Calculator to compare the actual after-tax, after-fee end balance from every institution you are considering — never make a final selection based on advertised rate alone.

Time your CD commitments strategically around Federal Reserve interest rate cycles. When the Federal Reserve is in a rate-hiking cycle, short-term CDs of 6 to 12 months allow you to reinvest at progressively higher rates as each CD matures without locking in a rate that will soon be surpassed. When rates are at or near their cyclical peak and a decline is expected, locking in a 3 to 5-year CD secures the favorable rate for an extended period before it drops. Use the CD Calculator to model how locking in at today’s rate across different term lengths would perform compared to rolling shorter-term CDs in a changing rate environment — this analysis frequently reveals clear, mathematically superior strategies for your specific situation.

Model early withdrawal scenarios before committing to any CD. Most standard CDs impose early withdrawal penalties ranging from 3 to 12 months of interest. Before opening a CD, use the CD Calculator to determine your net return if you were forced to exit the CD at year 1, year 2, or year 3 — by shortening the term and adjusting the inputs to reflect the applicable penalty. Then compare this penalized return against a no-penalty CD at a slightly lower rate. Many investors discover through this analysis that a no-penalty CD is the superior financial choice once the full penalty scenario is modeled accurately.

Always reinvest the complete maturity value — both principal and accumulated interest — into a new CD. When a CD matures, the single biggest compounding mistake investors make is withdrawing the accumulated interest for discretionary spending and redepositing only the original principal into a new CD. Reinvesting the full maturity value allows your interest itself to begin earning compound interest in the next CD cycle. Use the CD Calculator to compare the 10-year outcome of consistently reinvesting full maturity values versus reinvesting only original principal — the difference is striking and provides powerful motivation for disciplined reinvestment behavior.

Explore FDIC and NCUA insurance limits when managing large CD portfolios. Individual deposits are FDIC-insured up to $250,000 per depositor per institution. If your total CD holdings approach or exceed this threshold, spread deposits across multiple FDIC-insured banks to ensure every dollar remains fully protected. Run each institution’s CD separately through the CD Calculator to project the growth of each allocation and ensure your total projected balance at maturity remains within insured limits throughout the full investment term.

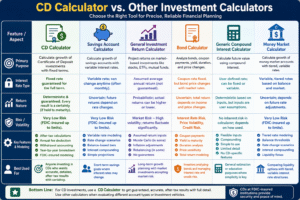

CD Calculator vs. Other Investment Calculators

A CD Calculator is a specialized financial tool with unique capabilities, and understanding how it differs from other commonly used financial calculators helps you select exactly the right tool for every specific financial planning scenario:

CD Calculator vs. Savings Account Calculator: Both tools calculate interest growth on deposited funds, but a savings account calculator must model variable interest rates that the bank can change at any time — often month to month in response to Federal Reserve policy changes. A CD Calculator, by contrast, models a fixed, contractually guaranteed rate that cannot change for the full agreed term regardless of what happens to market interest rates. For any financial planning scenario requiring absolute certainty of return, the CD Calculator is the definitively appropriate tool because it reflects the contractual, legally binding nature of CD interest rate guarantees.

CD Calculator vs. General Investment Return Calculator: A general investment return calculator projects the growth of market-based assets — stocks, index funds, ETFs, mutual funds — using assumed average annual returns. These projections are inherently probabilistic estimates; the actual future return may be meaningfully higher or lower than the assumed average in any given period. A CD Calculator, by contrast, produces deterministic, guaranteed results because CD interest rates are contractual. Every number the CD Calculator produces is not a statistical prediction — it is a mathematical certainty, contingent only on holding the CD to maturity at an FDIC-insured institution.

CD Calculator vs. Bond Calculator: Bond calculators model coupon payment streams, yield-to-maturity calculations, duration sensitivity, and price volatility in response to interest rate changes. Bonds trade actively on secondary markets, their prices fluctuate continuously with interest rate movements, and calculating their true total return requires modeling potential price changes alongside income streams. A CD Calculator is simpler and more directly applicable to low-risk, fixed-term savings planning — without the secondary market price complexity, duration risk, or credit risk analysis that comprehensive bond calculations require.

CD Calculator vs. Generic Compound Interest Calculator: A general compound interest calculator is broader and more flexible in its inputs, but it typically lacks the specific after-tax deduction modeling, annual fee subtraction, withdrawal accounting, and detailed year-by-year breakdown table output that make the CD Calculator specifically powerful for CD investment evaluation. When evaluating a CD specifically, always use a dedicated CD Calculator with all of these CD-specific features rather than a generic compound interest tool — the additional output detail makes a meaningful, practical difference in the quality and usability of your planning results.

CD Calculator vs. Money Market Calculator: Money market calculators typically model variable, tiered interest rates that change based on balance levels and prevailing market conditions. A CD Calculator models a single fixed rate guaranteed for a defined term. When comparing a CD against a money market account for the same investment amount and time horizon, run both through their respective calculators under conservative rate assumptions to see which genuinely delivers better after-tax returns given your specific circumstances and liquidity requirements.

Common Mistakes to Avoid When Using a CD Calculator

These are the most frequent and consequential errors that cause investors to draw inaccurate or misleading conclusions from their CD Calculator results — along with exactly how to avoid each one:

Mistake 1 — Entering APY instead of APR with a non-annual compounding setting. This is the single most common technical error in CD Calculator usage. If a bank quotes you a 5.00% APY and you enter that figure while also selecting monthly compounding, the calculator will apply monthly compounding on top of a rate that already incorporates annual compounding — producing an inflated, unrealistic result that significantly overstates your actual projected balance. Always determine the base APR rate before compounding and enter that figure, or switch the compounding frequency to annual if you are working exclusively with APY figures.

Mistake 2 — Leaving the tax rate at zero. Leaving the tax field blank or at zero produces pre-tax projections that overstate your actual take-home returns by a very significant margin. A 5 percent gross CD return becomes approximately 3.5 percent after-tax at a 30 percent combined rate — a 30 percent reduction in real earnings that the CD Calculator will only capture correctly if you enter your actual combined federal and state tax rate. Always enter your realistic effective marginal rate to see what you will genuinely keep.

Mistake 3 — Ignoring or significantly underestimating annual account fees. Investors routinely overlook small annual fees because they seem financially inconsequential in isolation. But the CD Calculator demonstrates clearly that fees compound negatively over multi-year terms — a $75 annual fee over 5 years is not just $375. It is $375 plus all the compound growth those dollars would have generated if they had remained invested earning the CD’s rate throughout. Always check the full fee disclosure document provided by the institution and enter every recurring annual charge accurately.

Mistake 4 — Comparing CDs with different compounding frequencies at face value without running the numbers. A 5.00% annually compounding CD and a 4.85% monthly compounding CD cannot be meaningfully compared by their stated rates alone. Running both through the CD Calculator with their respective compounding settings reveals which one actually produces the larger after-tax end balance over your target term — and the result often surprises investors who automatically assumed the higher quoted rate was definitively the better choice.

Mistake 5 — Using the CD Calculator only once and never running alternative scenarios. The CD Calculator delivers its full value when used comparatively across multiple scenarios — different institutions, different term lengths, different rates, different compounding frequencies, different fee structures. Investors who run only one scenario use the tool at perhaps 20 percent of its actual potential value. The most productive habit is to run a minimum of three to five complete scenarios before making any CD commitment, then select the option with the best verified after-tax, after-fee end balance.

Mistake 6 — Not accounting for the reinvestment rate when modeling multi-year CD strategies. Many investors project a single CD’s growth in isolation without considering what rate they will reinvest at when that CD matures. If you open a 5-year CD today at 5 percent and rates fall to 3 percent by maturity, your reinvestment return will be significantly lower. Use the CD Calculator to run reinvestment scenarios at different future rates to stress-test your long-term CD strategy and understand your range of possible outcomes before committing to specific term lengths.

Mistake 7 — Selecting CD term lengths based on gut feeling rather than calculated comparison. Many investors choose a 1-year or 5-year CD based on instinct or a general preference for short or long commitments, without running the numbers to see which term actually delivers the best after-tax return per year of commitment. Always run the CD Calculator for every available term length at each institution you are evaluating, then compare the annualized after-tax returns to make a data-driven term selection rather than an intuition-driven one.

Frequently Asked Questions (FAQs)

Q1: What exactly does a CD Calculator calculate and show me?

A CD Calculator calculates the complete financial performance of a Certificate of Deposit investment across every year of the chosen term. It shows you the projected end balance at maturity, the total gross interest earned across the full term, the total taxes owed on those interest earnings each year, the net after-tax interest you actually keep, and a detailed year-by-year breakdown table of every deposit, gross interest payment, annual tax deduction, and ending balance for every year. Many CD Calculators also produce a visual bar chart for immediate graphical understanding of the investment’s growth trajectory and the relative contributions of deposits versus compounding interest.

Q2: How accurate are CD Calculator projections?

CD Calculator projections are among the most accurate available in any personal finance planning tool — because CD interest rates are contractually fixed and guaranteed for the full agreed term by an FDIC-insured or NCUA-insured institution. Unlike stock market calculators that produce probabilistic estimates of future returns based on historical averages, the CD Calculator produces deterministic calculations of guaranteed outcomes. The results are mathematically precise as long as you input accurate, verified data from your CD’s written agreement — especially the correct APR (not APY), the correct compounding frequency, and your honest, realistic effective tax rate.

Q3: What compounding frequency gives the best CD returns?

More frequent compounding always produces higher returns at an identical stated annual interest rate. The ranking from lowest to highest return at the same rate is: annual < semi-annual < quarterly < monthly < continuous. Continuous compounding produces the theoretical mathematical maximum return for any given rate. In practice, the real-world difference between monthly and continuous compounding is very small for most deposit sizes. However, the difference between annual and monthly compounding can be meaningfully larger — especially for high principal amounts over multi-year terms. Always use the CD Calculator to compare exact dollar outcomes across the specific compounding frequencies offered by the institutions you are evaluating — never assume without calculating.

Q4: Is the interest earned on a CD taxable?

Yes — in the United States, all interest earned on CDs is fully taxable as ordinary income at both the federal level and in most states. CD interest is reported by your bank or credit union on IRS Form 1099-INT, which you must report on your annual tax return. It is taxed at your marginal income tax bracket rate — not at the lower long-term capital gains rate applied to qualifying stock investments. The CD Calculator’s tax rate field allows you to account for this obligation accurately, giving you a precise after-tax net return figure rather than a misleading pre-tax gross figure that significantly overstates the real benefit of the investment.

Q5: Can I use a CD Calculator to compare multiple CD offers from different banks?

Absolutely — and this is one of the most powerful and valuable uses of the CD Calculator. Run the calculator once for each CD offer you are evaluating, entering each institution’s specific APR, compounding frequency, annual fees, and term length. Then compare the resulting after-tax end balances side by side. This process consistently reveals that the CD with the highest advertised rate is not necessarily the one that puts the most actual money in your pocket — particularly when compounding frequencies differ between institutions or when one CD carries annual fees that the other does not. The CD Calculator transforms a confusing multi-variable comparison into a simple, clear financial decision.

Q6: What is a CD ladder and how does the CD Calculator help me build one?

A CD ladder is a disciplined investment strategy where you divide your total CD investment across multiple CDs with staggered maturity dates — typically 1-year, 2-year, 3-year, 4-year, and 5-year CDs held simultaneously. Each time a shorter-term CD matures, you reinvest the full proceeds into a new 5-year CD at the prevailing rate. This strategy provides the high yields of long-term CDs while giving you access to funds every year as each rung matures without paying early withdrawal penalties. Use the CD Calculator separately for each rung of your ladder to project the exact growth of every individual CD, then aggregate all results to understand your full ladder’s annual cash flow, total growth, and complete performance picture over your full investment time horizon.

Q7: What happens financially if I withdraw from a CD before its maturity date?

Most standard fixed-term CDs impose an early withdrawal penalty — typically equal to 3 to 12 months of accrued interest — if you access the funds before the contractual maturity date. Use the CD Calculator to model an early withdrawal scenario by shortening the term to the year you would need access and adjusting your inputs to subtract the applicable penalty from that year’s interest earnings. Then compare the penalized return against a no-penalty or liquid CD at a slightly lower rate. This comparison, run carefully through the CD Calculator, often reveals that a no-penalty CD is the more financially sound choice for investors who have any meaningful probability of needing early access to their funds during the investment period.

Q8: Should I hold my CD inside a tax-advantaged IRA or in a regular taxable account?

The optimal answer depends on your current tax rate, your expected future tax rate in retirement, your time horizon, and your overall retirement savings strategy. Holding a CD inside a Traditional IRA defers all tax on interest earnings until withdrawal — potentially beneficial if you expect to be in a lower marginal tax bracket during retirement than you are today. Holding a CD inside a Roth IRA allows all interest to accumulate and be withdrawn completely tax-free — often the most financially advantageous long-term structure for younger investors in lower current tax brackets. Use the CD Calculator to calculate your precise after-tax return in a standard taxable account, then compare that figure against the tax-advantaged growth projection to quantify the specific dollar benefit of each account structure for your individual situation before making a final decision.

Q9: How often should I use a CD Calculator to review my CD strategy?

You should use a CD Calculator every single time you make a CD-related financial decision — not just when opening a new CD. Run a fresh calculation whenever an existing CD approaches its maturity date and you need to evaluate reinvestment options. Run it when interest rates change significantly and you are considering whether to break an existing CD and reinvest at a higher rate. Run it when your income changes and your tax rate shifts, altering your after-tax return on existing CDs. The CD Calculator is not a one-time planning tool — it is a recurring financial analysis resource that should be part of every CD investment review, renewal, and comparison decision you make throughout your savings journey.

Conclusion

A Certificate of Deposit is one of the most reliable, most accessible, and most trustworthy wealth-preservation and growth tools available to ordinary savers and investors at every income level. Its defining strength — a contractually guaranteed, fixed interest rate for a fixed and known term — provides a level of financial certainty that no stock, bond, mutual fund, or market-based investment product can offer. But that guarantee only translates into genuine, meaningful wealth growth when you fully understand your real after-tax, after-fee return — not just the advertised rate prominently displayed on a bank’s homepage or promotional flyer.

That is precisely why the CD Calculator is not merely a useful convenience for CD investors. It is the essential, non-negotiable foundation of every sound CD investment decision. It strips away the marketing gloss of advertised rates, exposes the true and total cost of taxes and account fees, quantifies the powerful compounding impact of different compounding frequencies, and delivers a transparent, personalized financial roadmap that no intuition, no mental arithmetic, and no rough back-of-the-envelope estimate can reliably replicate.

Use the CD Calculator every single time you evaluate a new CD — whether you are comparing options at three different banks, deciding between a 2-year and a 5-year term, modeling the financial risk of early withdrawal before committing, or projecting the long-term growth of your CD ladder’s reinvestment cycles. Every decision deserves the precision and clarity that only accurate calculation can provide.

The difference between a good CD strategy and a great one is not access to exclusive investment products, special bank relationships, or insider financial knowledge. It is the consistent discipline of running accurate numbers — using a CD Calculator — before every decision. And that discipline, applied consistently over years and decades of smart CD investing, compounds into financial outcomes that far exceed what intuition and guesswork could ever deliver.

Your guaranteed returns deserve accurate calculations. Your financial future deserves the clarity of a CD Calculator. Start with your numbers today — because every month of precise planning is a month of compounding growth you will never have to leave on the table.