College Cost Calculator

Calculate monthly payments and total loan costs instantly with our Repayment Calculator

Table of Contents

- Introduction

- What Is a College Cost Calculator?

- Why Every Family Needs a College Cost Calculator

- Key Inputs You Need for the College Cost Calculator

- How to Use the College Cost Calculator Step by Step

- Understanding Your College Cost Calculator Results

- Smart Saving Strategies Based on Your College Cost Calculator Output

- Common Mistakes When Using a College Cost Calculator

- How Inflation and Investment Returns Affect Your Calculations

- Tips to Reduce the Financial Burden of College Costs

- Frequently Asked Questions (FAQs)

- Conclusion

Introduction

Planning for college is one of the most critical financial decisions a family will ever make. With tuition fees rising every single year, the cost of sending a child to college can feel completely overwhelming — especially for families who delay their planning. That is exactly why using a college cost calculator is no longer optional for modern families. It is absolutely essential.

A college cost calculator gives you a clear, data-driven picture of what college will actually cost by the time your child is ready to enroll. It takes into account tuition inflation, your current savings, your monthly contributions, investment returns, taxes, and much more. Instead of guessing, you get real, personalized numbers — and those numbers empower you to make smarter financial decisions starting right now.

Whether you are a parent of a newborn, a parent of a middle schooler, or a parent of a teenager just a few years away from graduation, this guide will walk you through absolutely everything you need to know about using a college cost calculator effectively. We will explain every input field, break down every output result, and share proven strategies to help you reach your college savings goal with full confidence.

The earlier you plan, the less pressure you face later. College costs will not wait — and neither should your savings strategy. Every month you delay is a month of compound growth you can never recover.

What Is a College Cost Calculator?

A college cost calculator is a financial planning tool that helps families estimate the true total cost of a college education — not just what tuition costs today, but what it will realistically cost in the future after accounting for consistent annual price increases over your specific timeline.

Today, the average annual cost of attending a four-year public university in the United States is approximately $30,000 to $35,000, which includes tuition, mandatory fees, room and board, textbooks, transportation, and personal living expenses. For private universities, that total can easily exceed $60,000 to $70,000 per year. Over four years, you are potentially looking at a total bill anywhere between $120,000 and $280,000 or more — and that number grows larger every single year.

A college cost calculator does not just display this scary total and leave you guessing. It goes far deeper. It provides you with:

- A precise monthly savings target so you know exactly how much to set aside each month starting today

- A projection of how your current savings will grow through compound interest before college begins

- A clear picture of what percentage of total costs your savings plan will realistically cover

- The actual projected freshman year cost — fully adjusted for tuition inflation over your specific timeline

Most importantly, a college cost calculator transforms an overwhelming multi-decade financial challenge into a single, manageable monthly action. Instead of being paralyzed by the thought of a $200,000 future bill, you discover that a specific and achievable monthly savings amount — starting today — will get you to your goal. That shift from anxiety to clarity is the real power of this tool.

A well-designed college cost calculator is not just a number-crunching machine. It is a strategic planning partner that helps you ask the right questions, set the right goals, and take the right actions — consistently, month after month, year after year.

Why Every Family Needs a College Cost Calculator

Many families make the painful mistake of avoiding the numbers until it is far too late. They tell themselves they will “figure it out” when the time comes — but without a concrete savings plan, the result is almost always last-minute student loans, severe financial stress, and significantly compromised educational choices for their children.

Here is exactly why using a college cost calculator changes everything for every family:

It reveals the real future cost — not just today’s sticker price. College costs increase by approximately 4 to 6 percent every year on average. A child who is 10 years away from starting college will face a first-year tuition bill that is 50 to 80 percent higher than what families are paying today. A college cost calculator automatically applies this annual growth rate to every year of your projection, so you see the true future financial burden — not a falsely comforting present-day number.

It creates urgency that drives early action. When families see the actual projected total cost displayed clearly, the urgency to act becomes impossible to ignore. A family that starts using a college cost calculator and begins saving when their child is born has the extraordinary power of compounding growth working for them for 18 full years. A family that waits until high school does not. The difference in required monthly contributions between an early starter and a late starter can be three to four times higher — sometimes the difference between an affordable monthly amount and a crushingly large one.

It quantifies the value of savings you already have. A good college cost calculator takes your current savings balance — whatever it is — and calculates exactly how much it will grow through compound interest by the time college begins. Every dollar you have already set aside is working actively for you, and the calculator shows you precisely how much growth you can expect from what you have today.

It enables realistic, personalized goal-setting. Not every family aims to cover 100 percent of college costs from personal savings. Many families plan to cover 35 percent, others 50 percent, and others 70 percent — with the remaining portion coming from merit scholarships, need-based grants, part-time student employment, or modest and manageable loans. The college cost calculator lets you define your own coverage goal percentage and immediately calculates exactly what you need to save each month to hit that precise target.

It removes emotional guesswork from a mathematical problem. College savings decisions made without data are almost always either dangerously optimistic or so pessimistic that families give up before starting. The calculator eliminates emotion from the equation entirely and replaces it with accuracy, clarity, and a concrete direction forward.

Key Inputs You Need for the College Cost Calculator

Accurate inputs produce accurate results. Here is a thorough, detailed breakdown of every field in a college cost calculator and what each one means for your overall plan:

Annual Cost ($):

This is the current total annual cost of the college you are planning for — not just tuition, but the complete cost of attendance, which includes tuition, mandatory fees, room and board, textbooks, transportation, and personal expenses. For a four-year public university, a realistic estimate is $28,000 to $35,000 per year. For private universities, use $55,000 to $70,000 per year. Always use the school’s official cost of attendance figure, not just the advertised tuition rate.

Increase % (Annual Tuition Inflation):

The expected annual percentage increase in college costs. College tuition in the United States has historically increased at 4 to 6 percent per year, significantly faster than general consumer inflation. Using 5 percent is the widely accepted planning standard that provides a realistic and conservative buffer against underestimating future costs.

Years Until College:

The number of years remaining before your child begins college. This is arguably the most impactful variable in the entire college cost calculator. More years means more compounding growth, a lower required monthly contribution, and dramatically less financial pressure. Even one or two extra years of saving makes a measurable difference in your final outcome.

Duration (Years in College):

How many years your child is expected to attend college. For a standard four-year bachelor’s degree, enter 4. For students pursuing extended programs, pre-professional tracks, or double degrees, it is wise to budget for 5 years as a conservative planning assumption.

Return % (Annual Investment Return):

The average annual return you expect to earn on your college savings investments. A well-diversified 529 plan or index fund portfolio might realistically average 5 to 8 percent per year over a long time horizon. For conservative planning, use 5 to 6 percent to avoid overestimating growth and ending up short.

Goal % (Your Savings Coverage Target):

The percentage of total projected college costs you personally plan to cover through your own savings. Entering 35 percent tells the college cost calculator to calculate exactly what you need to save to fund that specific portion of the total bill. This is a critical field because it lets you plan around reality — acknowledging that other funding sources will contribute alongside your savings.

Inflation % (General Consumer Inflation):

The broad economic inflation rate — not tuition-specific inflation, but the general rate at which prices rise across the economy. This is used to convert your future college savings goal into today’s purchasing power dollars, helping you understand the real financial burden in terms you can relate to right now.

Current Savings ($):

The total amount you have already accumulated and set aside specifically for college. Enter this number completely honestly. Even a modest amount — $500 or $2,000 — grows substantially over 10 or 15 years when invested appropriately. This existing balance reduces your required monthly contribution.

Tax Rate %:

The applicable tax rate on investment earnings in your savings account. This field is especially important if you are using a taxable brokerage account rather than a tax-advantaged 529 plan. In a 529 plan, qualified withdrawals are completely tax-free, which dramatically improves the effective after-tax return on your savings.

Monthly Contribution ($):

The amount you plan to add to your college savings every single month going forward from today. This is the single most controllable and impactful variable in the entire college cost calculator. Small, consistent increases in your monthly contribution — even $50 more per month — compound into tens of thousands of additional dollars over a decade.

Other Income ($) and Miscellaneous ($):

Additional expected funds that will reduce your total savings gap — such as annual contributions from grandparents, tax refunds dedicated to the college fund, or anticipated financial aid. Be conservative and realistic with these fields. Overestimating other income sources leads to dangerous underplanning and an ugly surprise later.

How to Use the College Cost Calculator Step by Step

Using a college cost calculator effectively requires a thoughtful, step-by-step approach. Here is a clear, detailed walkthrough that will help you extract the most accurate and actionable results possible:

Step 1 — Research the actual cost of attendance first.

Before touching any calculator field, visit the official financial aid or admissions website of the school or type of school you are planning for. Download or note the complete cost of attendance breakdown — including tuition, fees, room, board, books, and personal expenses. Using a real number rather than a guess dramatically improves the accuracy of your results.

Step 2 — Enter the current annual cost accurately.

Type the full cost of attendance into the first input field. If you do not yet have a specific target school in mind, use $31,000 per year as a solid public university baseline or $60,000 per year for a private university estimate.

Step 3 — Set your annual tuition increase rate.

Enter 5 percent as the standard planning assumption. If you have historical data showing that your target school increases costs at a different rate — 3 percent or 7 percent — use that specific figure for greater precision.

Step 4 — Enter your timeline with precision.

Count the exact number of years from today until your child’s first semester. If your child is currently 9 years old and will start college at 18, you have 9 years. Do not round up. Every year that you are precise about translates to more accurate monthly savings requirements.

Step 5 — Enter your complete financial profile.

Carefully fill in your expected annual investment return, your current savings balance, your planned monthly contribution, your effective tax rate, and any additional income sources. Take your time with these fields — they determine the accuracy of your entire projection. Use honest, realistic numbers, not optimistic best-case scenarios.

Step 6 — Set a realistic and achievable goal percentage.

Decide honestly what percentage of total costs your savings alone will target. For most families with a standard income, 35 to 50 percent is both realistic and achievable when starting at least 8 to 10 years before college, especially when combined with active scholarship applications and financial aid.

Step 7 — Click Calculate and carefully study both result boxes.

The college cost calculator will instantly display two complete scenarios. Read both results carefully and fully. The numbers may be higher than you expected — but that is precisely the value of the tool. Knowing accurate numbers now is always better than being shocked by reality when college begins.

Step 8 — Run multiple scenarios to find your optimal plan.

If the required monthly savings from your first calculation seems too high for your budget, adjust your inputs. Try increasing your monthly contribution slightly, extending your timeline, adjusting your goal percentage, or factoring in additional income sources. Keep running scenarios until you find a plan that is both realistic for your current budget and sufficient to meet your college savings goal.

Understanding Your College Cost Calculator Results

The college cost calculator delivers two distinct result sets, each providing a different financial perspective that together give you a complete, 360-degree view of your savings challenge.

Result Set 1 — If You Pay College Costs in Full From Savings:

This scenario assumes your savings will cover 100 percent of the projected college bill. It shows you four specific numbers:

Total Cost — The complete projected expense of every year of college combined, after applying annual tuition increases across your full timeline. This number is the one that typically surprises families most, because it reflects the real future cost — not today’s seemingly manageable annual tuition.

Today’s Money — This is the inflation-adjusted equivalent of that future total, expressed in current purchasing power. It tells you: if you had to write a check for this amount today, how large would it need to be in today’s dollars? This figure helps you internalize the real financial burden without being overwhelmed by inflated future dollar amounts.

Monthly Savings Required — The precise amount you need to deposit into your college savings account every single month from today until the first college bill arrives, assuming your existing savings also grow at your specified return rate. This is your primary action number — the one you carry forward into your actual financial plan.

Freshman Year Cost — The projected cost of the very first year of college after your child enrolls, fully adjusted for annual tuition inflation compounded over your timeline. This is the first check you will actually write, and knowing this number years in advance is enormously valuable for financial planning.

Result Set 2 — If X% of Costs Come From Your Savings:

This is typically the more practical and realistic scenario for most families. It assumes that only your chosen percentage of total costs will come from personal savings, with the remaining percentage coming from other sources.

Amount You Need to Save — The specific total dollar target for your savings pool, based on your goal percentage applied to the total projected cost. This is your real savings finish line — the number you are working toward month by month.

Monthly Savings Required for Partial Coverage — The adjusted monthly contribution needed to reach your partial-savings goal, accounting for your existing savings balance, expected investment growth, and any additional income sources you entered. This number is almost always lower and more achievable than the full-coverage monthly requirement.

Freshman Year Partial Cost — The portion of first-year costs that your savings plan will directly fund. The remaining portion represents the gap to be filled by scholarships, grants, work-study earnings, or modest student loans — all of which you should be actively planning for simultaneously.

Reading both result sets together gives you a complete picture — the maximum you would need to save to go it entirely alone, and the more realistic monthly target when you plan to use multiple funding sources in combination.

Smart Saving Strategies Based on Your College Cost Calculator Output

Once you have your personalized numbers from the college cost calculator, here is exactly how to turn those numbers into a concrete, high-performing savings strategy:

Open a 529 College Savings Plan immediately.

A 529 plan is the single most powerful financial vehicle available for college savings. All investment growth inside the account is completely tax-free, and every dollar withdrawn for qualified education expenses — including tuition, fees, books, and housing — is also tax-free. Most states additionally offer a state income tax deduction for annual contributions. There is no reason not to open one today.

Automate your monthly contributions without exception.

Set up automatic transfers from your checking account to your 529 or investment account on the same day your paycheck arrives. Automation is the most powerful habit in personal finance because it removes the decision entirely. You never have to choose whether to contribute this month — it happens automatically, every month, no matter what.

Increase your contributions incrementally every year.

Every January, increase your monthly college savings contribution by a small, manageable amount — even $25 or $50 more per month. An increase of just $50 per month, sustained for 15 years with 6 percent growth, adds more than $14,000 to your college fund — completely from a change most families would barely notice in their monthly budget.

Invest for growth during the early years.

When your child is young and college is more than 8 years away, your savings have time to recover from market downturns. Allocate a larger portion of your college fund to growth-oriented index funds or stock-heavy 529 portfolios during these early years. As college approaches within 3 to 4 years, gradually shift toward more conservative, stable-value investments to protect what you have built.

Invite family contributions directly into the 529.

Educate grandparents, aunts, uncles, and close family friends about the option to contribute directly to your child’s 529 plan. Suggest it as an alternative to traditional birthday and holiday gifts. Even $100 from three or four family members twice a year adds up to more than $600 to $800 annually — which, invested over 15 years, can grow into a significant college fund contribution.

Revisit the college cost calculator every single year.

Tuition costs increase, investment returns fluctuate, your savings balance grows, and family finances evolve. Running an updated calculation every year — ideally in January after you review your family’s financial picture — ensures that your plan stays accurately calibrated and gives you the opportunity to make small adjustments before any savings gap becomes large.

Common Mistakes When Using a College Cost Calculator

Avoiding these widespread planning errors will dramatically improve both the accuracy of your projections and the long-term strength of your college savings strategy:

Mistake 1 — Underestimating the annual tuition increase rate.

Many families default to entering 2 or 3 percent as the tuition inflation rate because that matches general consumer inflation. This is one of the most dangerous planning mistakes a family can make. College costs have consistently risen at 4 to 6 percent per year, far outpacing broader inflation. Using too low an increase rate causes a serious and growing savings shortfall that compounds every year until college begins.

Mistake 2 — Using tuition alone instead of total cost of attendance.

Tuition is only one component of the actual college bill. Room and board, required fees, textbooks, supplies, transportation between home and campus, and personal expenses can easily add $10,000 to $18,000 per year on top of tuition. Always enter the complete, full cost of attendance into the college cost calculator — not just the tuition line.

Mistake 3 — Ignoring taxes on investment earnings.

If your college savings are held in a standard taxable brokerage account rather than a 529 plan, every year of capital gains, dividends, and interest is subject to federal and state income taxes. The tax rate field in the college cost calculator exists for this exact reason. Entering your real marginal tax rate gives you an accurate after-tax return picture. Ignoring it overstates your effective savings growth.

Mistake 4 — Overestimating scholarships and financial aid.

It is natural to assume your child will qualify for generous scholarships or substantial need-based aid — but scholarship competition is extraordinarily fierce, and aid packages vary widely by institution and year. Be very conservative when entering the “Other Income” and “Miscellaneous” fields. Plan for the worst and let scholarships be a pleasant surprise that reduces your loan burden — rather than a cornerstone of your plan that fails to materialize.

Mistake 5 — Setting an unrealistically high goal percentage.

Committing to cover 100 percent of projected college costs from personal savings requires monthly contributions that most families genuinely cannot sustain over 15 to 18 years without severely compromising other financial goals. Starting with a targeted goal of 35 to 50 percent and supplementing with scholarships, work-study earnings, and modest student loans is a far more balanced and sustainable strategy for the majority of American families.

Mistake 6 — Running the calculator once and never returning to it.

Life changes dramatically over a 15-year savings journey. Investment markets shift, tuition increases at varying rates each year, family income evolves, and your savings balance grows. Treating the college cost calculator as a one-time exercise rather than an annual planning ritual creates silent, invisible drift away from your savings target — drift that becomes a crisis only when it is almost too late to correct.

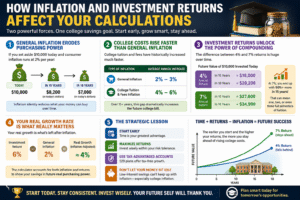

How Inflation and Investment Returns Affect Your Calculations

Two of the most powerful and most misunderstood variables inside the college cost calculator are inflation and investment return rate. Understanding how these two forces interact over time is the difference between a college savings plan that works and one that falls dangerously short despite years of disciplined saving.

General inflation steadily erodes the purchasing power of your money.

If you set aside $10,000 today and consumer inflation runs at 2 percent per year, that same $10,000 will only purchase approximately $8,200 worth of goods and services in 10 years. In 18 years, it purchases only about $7,000 worth in today’s terms. This is why the college cost calculator shows your savings goal expressed in today’s dollars — to help you understand the real, inflation-adjusted purchasing power required, not just a nominal future figure that sounds large but means less.

College-specific inflation is dramatically more severe than general inflation.

While general consumer inflation typically runs at 2 to 3 percent per year, college tuition and fees have historically increased at 4 to 6 percent annually — more than twice the rate of general inflation. This compounding tuition-specific inflation is the primary reason that a college bill 15 years from now looks so much larger than today’s numbers suggest. The college cost calculator captures this separately from general inflation to give you an accurate dual-factor projection.

Investment returns grow your savings through the extraordinary power of compounding.

The difference between a 4 percent and a 7 percent annual return — seemingly just 3 percentage points — is massive when compounded over 15 to 18 years. At 4 percent, $10,000 invested today grows to approximately $18,000 in 15 years. At 7 percent, that same $10,000 grows to nearly $27,600 — more than 50 percent more. Over an entire 18-year college savings journey, the choice of investment vehicle and its expected return can represent tens of thousands of dollars — the equivalent of one, two, or even three full semesters of tuition.

Your real growth rate is the net difference between return and inflation.

If your college savings earn 6 percent annually on investments but general inflation runs at 2 percent, your real inflation-adjusted growth rate is approximately 4 percent. The college cost calculator factors in both forces simultaneously, giving you a genuinely accurate picture of how much your savings will be worth in future real purchasing power — not just how large the nominal dollar balance will appear.

The strategic lesson is clear and unambiguous: start saving as early as possible, maximize your investment return within your appropriate risk tolerance, use tax-advantaged accounts like 529 plans that compound growth tax-free, and never let your college fund sit idle in a low-interest savings account that fails to keep pace with even general inflation — let alone the much steeper college cost inflation curve.

Tips to Reduce the Financial Burden of College Costs

Even with years of disciplined saving and consistent annual use of a college cost calculator, many families will still face a meaningful gap between their accumulated savings and the full projected college bill. That gap is not a personal failure — it is an expected and manageable part of the college funding reality for most American families. Here are the most proven, practical, and impactful strategies to close that gap:

Apply aggressively and early for every scholarship available.

Hundreds of billions of dollars in scholarship money are awarded every year in the United States — and a genuinely surprising portion of that money goes unclaimed every year because eligible families never apply. Build a scholarship application habit starting in 9th grade and maintain it consistently through senior year. Target large national scholarships, regional scholarships, local community foundation awards, employer-sponsored scholarships, and smaller niche scholarships — which frequently receive only a handful of applications and offer odds far better than any national competition.

Consider community college for the first two years.

Completing general education requirements at a local community college and then transferring with full credit to a four-year university to complete your degree can cut the total cost of a bachelor’s degree by 30 to 50 percent — without any reduction in the credential or reputation of the four-year degree you ultimately earn. Many states have formal, guaranteed transfer agreements that ensure admission to top state universities for community college graduates who meet academic standards.

Prioritize in-state public universities as a strategic default.

Public universities charge dramatically lower tuition for state residents compared to out-of-state students, and the difference is not small. In-state tuition at a quality public university can be two to three times lower than out-of-state tuition at the same institution — and often comparable in cost to attending a private university with partial financial aid. If your state has strong universities aligned with your child’s academic interests, in-state enrollment is one of the highest-impact cost-reduction decisions available.

Submit the FAFSA every single year — starting as early as October 1st.

The Free Application for Federal Student Aid determines eligibility for federal Pell Grants, work-study program placements, and low-interest federal student loans. Many families who believe their income is too high to qualify for meaningful aid still receive valuable benefits through the FAFSA process, including unsubsidized loans with significantly lower interest rates than private alternatives and access to work-study programs. Submit as early as possible each year — many aid programs distribute funds on a first-come, first-served basis until the money runs out.

Negotiate financial aid award letters confidently.

Many families never realize that financial aid packages offered by colleges and universities are frequently negotiable. If your child receives a more generous aid offer from one institution, you can present that offer letter to another institution and respectfully ask whether they can match or improve their package. Admissions and financial aid offices often have discretion to increase awards for desirable candidates — and many families who ask receive improved offers simply because they had the confidence to make the request.

Encourage your student to work part-time responsibly during college.

Research consistently shows that students who work between 10 and 15 hours per week during college maintain academic performance comparable to full-time students while meaningfully funding their own living expenses. Even modest part-time earnings of $600 to $900 per month can cover groceries, transportation, textbooks, and personal expenses — directly reducing the amount of savings or loans needed to sustain the college experience.

Explore employer tuition assistance programs.

A large number of mid-size and large employers offer tuition reimbursement or assistance programs as part of their benefits packages — for employees and sometimes for dependents as well. Check your employer’s complete benefits package carefully, and if your company offers this benefit, take full advantage of it. This is one of the most consistently underutilized sources of college cost assistance available to working families.

Apply for college credits in high school through AP, IB, and dual enrollment.

Students who earn Advanced Placement credits, International Baccalaureate credits, or dual enrollment college credits while still in high school can enter college with a semester or even a full year of credit already completed. Finishing college in three years instead of four — or three and a half years instead of four — eliminates an entire semester or year of tuition, room, board, and fees, which represents a direct cost saving of $15,000 to $35,000 or more depending on the school.

Frequently Asked Questions About the College Cost Calculator

1. What is a College Cost Calculator?

A College Cost Calculator is a financial planning tool that helps estimate the total cost of college, including tuition fees, education expenses, and future costs. It allows students and parents to create a smart college savings plan and prepare for rising education costs.

2. How accurate is this College Cost Calculator?

This College Cost Calculator provides estimates based on your annual college cost, inflation rate, current savings, and investment returns. While actual expenses may vary, it offers a reliable estimate of future college costs.

3. Can the College Cost Calculator estimate future tuition costs?

Yes. The College Cost Calculator projects future tuition costs by applying annual cost increases over time. This helps families understand how much college may cost when a student is ready to enroll.

4. How does the College Cost Calculator calculate total education expenses?

The College Cost Calculator combines projected tuition, duration of study, inflation adjustments, and other financial factors to estimate the total college cost for a complete degree program.

5. Does the College Cost Calculator include current savings?

Yes. The College Cost Calculator factors in your current savings balance, monthly contributions, and expected investment growth to estimate how much money will be available for future education expenses.

6. How much should I save each month for college?

The College Cost Calculator calculates the monthly savings amount needed to reach your education funding goal. This feature makes it easier to create an effective college savings strategy.

7. Can I use this College Cost Calculator for private and public colleges?

Absolutely. The College Cost Calculator can be used for public universities, private colleges, community colleges, and other educational institutions by entering the appropriate annual cost figures.

8. What is the Goal Percentage in the College Cost Calculator?

The Goal Percentage represents the portion of future college expenses you want to cover through savings. The College Cost Calculator then estimates how much money you need to save to achieve that target.

9. Why should I use a College Cost Calculator before starting a savings plan?

Using a College Cost Calculator helps you estimate future education expenses, set realistic savings goals, and make informed decisions about funding college without unnecessary financial stress.

10. Who should use this College Cost Calculator?

The College Cost Calculator is ideal for parents, students, guardians, and financial planners who want to estimate college costs, compare savings scenarios, and prepare for future education expenses with confidence.

Conclusion

The cost of college is not going down. Year after year, tuition, fees, and the total cost of attendance continue climbing at rates that significantly outpace general inflation — and families who fail to plan proactively find themselves trapped in burdensome debt, forced to compromise on their child’s educational opportunities, or watching their children begin adult professional life burdened by student loans that will take a decade or more to repay.

The most powerful and impactful thing you can do for your child’s future right now is to start planning — and that planning starts with using a college cost calculator. Not next year. Not when your child starts middle school. Not when senior year of high school arrives. Today.

A college cost calculator removes guesswork, eliminates false comfort, and replaces anxiety with clarity. It tells you exactly where you stand financially. It tells you exactly what monthly action you need to take. And it tells you exactly how much time you have remaining to take it.

The numbers may feel large on first reading. The required monthly savings figure may seem ambitious relative to your current budget. But the alternative — no plan, no savings discipline, and the full weight of a $150,000 to $280,000 college bill arriving all at once when your child turns 18 — is far more daunting and far more damaging.

With a clear plan guided by a college cost calculator, you approach that bill with years of compounding growth behind you, a realistic and achievable savings goal directing you, and a monthly habit that has been quietly building your child’s future all along.

Use the college cost calculator today. Revisit it every year. Adjust your contributions when life allows. And let the math — not hope, not guesswork, not anxiety — guide every decision along the way.