Repayment Calculator

Calculate interest, monthly payments, and payoff time instantly with our Credit Card Calculator

Table of Contents

- Introduction

- What Is a Repayment Calculator?

- How Does a Repayment Calculator Work?

- Why You Should Use a Repayment Calculator

- How to Use the Repayment Calculator – Step by Step

- Key Terms You Must Know

- How Interest Rate Affects Your Repayment Plan

- The Power of Extra Payments

- Payment Frequency and How It Changes Your Total Cost

- Hidden Costs: Taxes, Insurance, and Fees

- Reading the Amortization Table

- Strategies to Pay Off Your Loan Faster

- Common Mistakes People Make

- Using a Repayment Calculator for Long-Term Financial Planning

- Frequently Asked Questions (FAQs)

- Conclusion

Introduction

A Repayment Calculator is a powerful financial tool designed to help you estimate your monthly loan repayments, total interest costs, and the overall amount payable over the life of a loan. By entering details such as the loan amount, interest rate, repayment term, and any additional payments, you can instantly see how your repayment schedule changes. This calculator also factors in taxes, insurance, fees, and other costs to provide a more accurate financial picture. Whether you’re planning a mortgage, personal loan, or other financing, this tool helps you make smarter borrowing decisions and manage your budget with confidence.

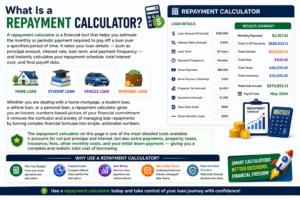

What Is a Repayment Calculator?

A repayment calculator is a financial tool that helps you estimate the monthly or periodic payment required to pay off a loan over a specified period of time. It takes your loan details — such as principal amount, interest rate, loan term, and payment frequency — and instantly calculates your repayment schedule, total interest cost, and final payoff date.

Whether you are dealing with a home mortgage, a student loan, a vehicle loan, or a personal loan, a repayment calculator gives you an honest, numbers-based picture of your financial commitment. It removes the confusion and anxiety of managing loan repayments by turning complex financial formulas into simple, actionable numbers.

The repayment calculator on this page is one of the most detailed tools available. It accounts for not just principal and interest, but also extra payments, property taxes, insurance, fees, other monthly costs, and your initial down payment — giving you a complete and realistic total cost of borrowing.

How Does a Repayment Calculator Work?

At its core, a repayment calculator uses the standard loan amortization formula. Amortization means your loan is paid off gradually through equal periodic payments, with each payment covering both interest and a portion of the principal.

The formula used is:

Monthly Payment = [P × r × (1 + r)ⁿ] ÷ [(1 + r)ⁿ − 1]

Where:

- P = Principal (loan amount minus down payment)

- r = Periodic interest rate (annual rate ÷ payment frequency)

- n = Total number of payments (years × payment frequency)

In the early stages of your loan, a larger share of each payment goes toward interest. As the loan matures, more of each payment reduces the principal. This is why paying extra toward the principal early in a loan has a disproportionately large positive effect on your total interest cost.

The repayment calculator on this page adds further precision by layering in extra monthly contributions, property tax, insurance, fee amounts, and your down payment — so the result reflects your true monthly obligation.

Why You Should Use a Repayment Calculator

The number one reason to use a repayment calculator is clarity. Most borrowers sign loan agreements without fully understanding how much they will pay in total over the life of the loan. The difference between the amount you borrow and the total amount you repay — when accounting for interest, fees, and other costs — is often shocking.

Here is what a repayment calculator does for you:

- Shows your exact monthly payment including all associated costs

- Reveals your total interest cost over the full loan term

- Helps you compare loan options by modeling different interest rates or terms

- Motivates faster payoff by showing how extra payments reduce your total cost

- Supports better budgeting by giving you a clear monthly commitment figure

- Helps you evaluate down payment size and its long-term impact

Financial advisors universally recommend using a repayment calculator before signing any loan agreement. Having the numbers in front of you empowers you to negotiate better terms, choose the right loan structure, and avoid costly surprises.

How to Use the Repayment Calculator – Step by Step

Using the repayment calculator on this page is completely straightforward. Here is a complete walkthrough of each field:

Step 1 — Enter Your Principal

This is the total loan amount before your down payment is applied. For example, if you are borrowing $100,000 for a home, enter 100000.

Step 2 — Enter Your Interest Rate (%)

Enter the annual interest rate offered by your lender. Even a half-percent difference in rate can add or save thousands of dollars over a long loan term.

Step 3 — Enter Loan Term in Years

The longer the term, the lower your monthly payment — but the more total interest you pay. A 30-year mortgage costs significantly more in total than a 15-year mortgage, even at the same rate.

Step 4 — Enter Payment Frequency

Enter how many times per year you make payments. Monthly = 12, bi-weekly = 26, weekly = 52. Higher frequency payments reduce your balance faster and lower total interest.

Step 5 — Enter Extra Payment Amount

If you plan to pay more than the minimum each period, enter that extra amount. This is one of the most powerful variables in the repayment calculator.

Step 6 — Enter Tax Rate (%)

For mortgage loans, property tax is often included in monthly payments. Enter your local tax rate as a percentage of the loan for an accurate monthly cost.

Step 7 — Enter Insurance, Fees, and Other Costs

These are the hidden costs many borrowers overlook. Include monthly insurance premiums, lender fees, and any other recurring costs for a complete picture.

Step 8 — Enter Down Payment

Your down payment reduces the principal balance immediately. A larger down payment means lower monthly payments and less total interest over the life of the loan.

Once all fields are filled, click CALCULATE. The repayment calculator will instantly display your monthly payment, total interest, and total payment amount — plus a visual bar chart and a full year-by-year amortization table.

Key Terms You Must Know

Understanding these terms will help you use a repayment calculator more effectively:

- Principal: The original loan amount you borrowed before any payments are made

- APR (Annual Percentage Rate): The yearly cost of borrowing expressed as a percentage

- Amortization: The process of gradually paying off a loan through scheduled, equal payments

- Down Payment: An upfront lump-sum payment that directly reduces your loan principal

- Equity: The portion of the asset you own — calculated as current value minus remaining loan balance

- Extra Payment: Any amount paid beyond your required scheduled payment, which directly reduces principal

- Escrow: A third-party account used to hold and disburse tax and insurance payments on your behalf

- Balance: The remaining loan amount you still owe at any given point in time

How Interest Rate Affects Your Repayment Plan

The interest rate is the single most important variable in any repayment calculator. Even a 1% difference in rate can result in tens of thousands of dollars in additional interest over a long loan term. This is why shopping around for the best rate before borrowing is one of the most valuable financial decisions you can make.

Consider a $100,000 loan over 30 years at different rates:

| Interest Rate | Monthly Payment | Total Interest Paid |

|---|---|---|

| 3% | ~$422 | ~$51,777 |

| 5% | ~$537 | ~$93,256 |

| 7% | ~$665 | ~$139,511 |

| 9% | ~$805 | ~$189,664 |

The difference between a 3% rate and a 9% rate is nearly $138,000 in additional interest on the same $100,000 loan. Use the repayment calculator to model your specific rate and understand exactly what your lender is charging you over the full life of the loan.

The Power of Extra Payments

One of the most impactful features of a repayment calculator is the extra payment field. Making additional payments — even modest ones — above your required monthly amount directly reduces your principal balance. Since interest is calculated on your remaining balance, a lower balance means less interest the following month, compounding your savings over time.

Strategies for making effective extra payments include:

- Bi-weekly payments: Paying half your monthly amount every two weeks results in 26 half-payments per year — equivalent to 13 full monthly payments instead of 12

- Annual lump sums: Apply tax refunds, bonuses, or inheritance directly to your loan principal

- Monthly top-ups: Add a fixed extra amount each month — even $50 to $100 makes a measurable difference

- Rounding up payments: If your payment is $537, consistently round it up to $600

Use the extra payment field in the repayment calculator to model exactly how much each strategy saves you — both in total interest and in years off your loan. The results will motivate you to commit immediately.

Payment Frequency and How It Changes Your Total Cost

The frequency field in the repayment calculator allows you to model monthly, bi-weekly, or weekly payment schedules. Most borrowers default to monthly payments, but switching to more frequent payments can shorten your loan term and reduce total interest significantly.

Here is why it works: With bi-weekly payments, you make 26 payments per year instead of 24. This is equivalent to one extra full monthly payment per year, directly reducing your principal faster. On a 30-year mortgage, bi-weekly payments can shorten the loan by several years and save thousands in interest — with virtually no change to your lifestyle.

The repayment calculator handles all frequencies — simply enter 12 for monthly, 26 for bi-weekly, or 52 for weekly, and it instantly recalculates your full repayment schedule and total interest cost.

Hidden Costs: Taxes, Insurance, and Fees

One of the biggest mistakes borrowers make is calculating only principal and interest — and forgetting the full monthly cost of a loan. A mortgage, for example, typically includes property tax held in escrow, homeowner’s insurance, and lender fees. These costs can add hundreds of dollars to your actual monthly payment and are often a surprise to first-time borrowers.

The repayment calculator on this page includes fields for:

- Tax %: Annual property tax as a percentage of the loan amount, divided into monthly contributions

- Insurance: Monthly homeowner’s or borrower’s insurance premium

- Fees: Recurring lender or loan servicing fees charged monthly

- Other: Any additional costs such as HOA fees, private mortgage insurance (PMI), or maintenance reserves

By including all of these in your repayment calculator inputs, you get a true PITI payment (Principal, Interest, Taxes, Insurance) — the real number that determines whether the loan genuinely fits within your budget.

Reading the Amortization Table

The amortization table generated by the repayment calculator is one of its most valuable outputs. It shows you, year by year, exactly how much of each payment goes toward principal versus interest — and what your remaining balance will be at any point in the future.

How to read the table:

- Year: The loan year (1 through end of term)

- Principal: Amount applied to the outstanding loan balance in that year

- Interest: Amount paid purely as interest in that year

- Total: Combined yearly payment (principal + interest + fees)

- Balance: Remaining loan balance at the end of each year

Notice in the early years, the interest column is much larger than the principal column. This reflects the front-loaded nature of amortized loans. As the loan ages, this ratio flips — you pay more principal and less interest with each passing year. Understanding this helps you see why the first several years of a loan are the most costly — and why making extra payments early in the loan has the greatest financial impact.

Strategies to Pay Off Your Loan Faster

Once you understand how to read a repayment calculator, you can use it to model and commit to powerful payoff strategies:

Refinance to a Lower Rate

If interest rates drop significantly after you take out your loan, refinancing can reduce your rate and your monthly payment. Use the repayment calculator to compare your current loan versus a refinanced version — accounting for any closing costs — to determine whether refinancing is worth it financially.

Shorten Your Loan Term

Switching from a 30-year to a 15-year term typically means a higher monthly payment but significantly less total interest. Model this in the repayment calculator to see whether your budget can support the increased monthly commitment.

Increase Payment Frequency

As discussed earlier, bi-weekly payments add one extra monthly payment per year. This simple change can shave years off your loan with no change in your day-to-day lifestyle.

Make Lump-Sum Principal Payments

Any windfall — a tax refund, bonus, inheritance, or side income — applied directly to your loan principal has an outsized effect on total interest. Use the extra payment field in the repayment calculator to measure the impact before you receive the funds, so you are ready to act immediately.

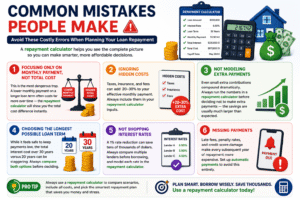

Common Mistakes People Make

Avoid these costly errors when planning your loan repayment:

Focusing Only on Monthly Payment, Not Total Cost

This is the most dangerous trap. A lower monthly payment on a longer loan term often costs far more over time — the repayment calculator will show you the total cost difference instantly.

Ignoring Hidden Costs

Taxes, insurance, and fees can add 20–30% to your effective monthly payment. Always include them in your repayment calculator inputs.

Not Modeling Extra Payments

Even small extra contributions compound dramatically. Always run the numbers in a repayment calculator before deciding not to make extra payments — the savings are usually much larger than expected.

Choosing the Longest Possible Loan Term

While it feels safe to keep payments low, the total interest cost over 30 years versus 20 years can be staggering. Always compare both options before deciding.

Not Shopping Interest Rates

A 1% rate reduction can save tens of thousands of dollars. Always compare multiple lenders before borrowing, and model each rate in the repayment calculator.

Missing Payments

Late fees, penalty rates, and credit score damage make every subsequent year of repayment more expensive. Set up automatic payments to avoid this entirely.

Using a Repayment Calculator for Long-Term Financial Planning

A repayment calculator is not just a one-time tool — it is a long-term financial planning instrument. Here are the ways you should integrate it into your ongoing financial strategy:

- Before buying a home: Model different purchase prices, down payment sizes, and interest rates to find the right budget

- When comparing lenders: Input each lender’s rate and fee structure to find the true lowest-cost option

- When considering refinancing: Compare your current loan balance and remaining term against refinance options

- After income changes: If you receive a raise or face a pay cut, use the repayment calculator to adjust your payment strategy accordingly

- When setting a payoff goal: Input your target debt-free date and work backward to find the required monthly payment

The most financially successful people are those who review and model their loan situations regularly — not just once at signing. A repayment calculator makes this fast, free, and easy to do at any time.

Frequently Asked Questions (FAQs)

What is the difference between a repayment calculator and a loan calculator?

They are essentially the same tool. A repayment calculator specifically focuses on breaking down how you pay back a loan over time — showing you the interest vs. principal split, total cost, and remaining balance year by year. The repayment calculator on this page is focused entirely on your payoff strategy and true cost of borrowing.

How accurate is the repayment calculator?

The repayment calculator uses the standard amortization formula and is highly accurate for fixed-rate loans. Variable-rate loans will change as rates fluctuate, so model a range of possible rates to plan for different scenarios. For the most precise figures, consult your lender’s official amortization schedule.

What happens if I miss a payment?

Missing a payment adds a late fee and may trigger a higher penalty interest rate. Your balance also increases because unpaid interest accrues. Use the fees field in the repayment calculator to model the cumulative cost of occasional late payments over your loan term.

Should I make a large down payment or keep cash for savings?

A larger down payment reduces your principal, your monthly payment, and your total interest. It may also help you avoid private mortgage insurance (PMI). However, depleting emergency savings carries its own risk. Use the repayment calculator to model both scenarios — a 10% down payment versus a 20% down payment — and weigh the interest savings against the risk of reduced liquidity.

How much does an extra $100 per month really save?

On a 30-year, $100,000 loan at 5% interest, paying an extra $100 per month can save over $25,000 in interest and shorten the loan by more than 7 years. Enter your specific numbers into the extra payment field of the repayment calculator to see your exact personal savings.

Can I use this repayment calculator for student loans or car loans?

Yes. The repayment calculator works for any fixed-rate amortizing loan — mortgage, auto loan, personal loan, student loan, or business loan. Simply enter the relevant loan details and it will produce an accurate repayment schedule and interest breakdown.

What is the best loan term to choose?

The best loan term balances monthly affordability with total cost. A shorter term means higher monthly payments but significantly less interest paid overall. Use the repayment calculator to find the term that fits your budget while minimizing your total borrowing cost.

Conclusion

Understanding your loan is not optional — it is essential. Every month you make a payment without understanding the interest vs. principal split, you are managing one of the most important areas of your financial life without full information.

A repayment calculator gives you instant clarity, complete transparency, and the power to make better financial decisions every single day. It shows you the true cost of your loan, helps you model payoff strategies, and motivates faster repayment by making the savings real and visible.

The key lessons from this guide are:

- Always calculate your full monthly cost — including taxes, insurance, and fees

- Use extra payments strategically — even small amounts compound into major savings over time

- Understand your amortization schedule — early payments are mostly interest; act accordingly

- Model multiple scenarios — rate changes, term changes, frequency changes — before committing to any loan

- Use the repayment calculator regularly — not just once at signing, but throughout the entire life of your loan

Start now. Enter your loan details into the repayment calculator above. See your real numbers. Build your plan. Every day you wait is a day interest is accumulating — take control of your financial future today.