Annuity Calculator

Plan your future income easily and find your exact retirement pension with our Pension Calculator

Table of Contents

- Introduction

- What Is a FERS Annuity Calculator?

- Why Every Federal Employee Needs a FERS Annuity Calculator

- Understanding FERS: The Federal Employees Retirement System Explained

- How FERS Annuity Calculations Work

- Key Inputs in a FERS Annuity Calculator Explained

- How to Use the FERS Annuity Calculator Step by Step

- Understanding Your Results: Balance, Interest, and Growth

- The Three-Part FERS Retirement Benefit Structure

- How Inflation and Fees Erode Your Annuity Over Time

- Real-Life Scenarios Using the FERS Annuity Calculator

- FERS vs. CSRS: Key Differences Federal Employees Must Know

- Maximizing Your FERS Annuity: Proven Strategies

- Common Mistakes Federal Employees Make in Retirement Planning

- Frequently Asked Questions (FAQs)

- Conclusion

Introduction

Federal government employment comes with one of the most comprehensive and generous retirement benefit packages available to any workforce in the United States — but only if you understand it, plan for it, and make the right decisions throughout your career. At the heart of that planning lies a single, indispensable tool: the FERS Annuity Calculator.

A FERS Annuity Calculator helps federal employees project the growth of their retirement savings, model the impact of annual contributions, understand how interest compounds over time, and determine whether their current trajectory will meet their retirement goals. Whether you are 30 years into a federal career or just starting your first government job, having a clear, numerical picture of your retirement outcome is the foundation of every smart financial decision you will make between now and the day you leave service.

In this comprehensive guide, we will cover everything you need to know — from the structure of the Federal Employees Retirement System and how annuity calculations work, to how inflation and fees affect long-term outcomes, and how to use the FERS Annuity Calculator to build and optimize your personal retirement plan. By the end, you will have both the knowledge and the framework to take full, confident control of your federal retirement future.

What Is a FERS Annuity Calculator?

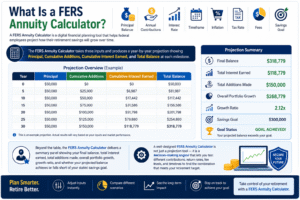

A FERS Annuity Calculator is a digital financial planning tool that allows federal employees to project how their retirement savings will grow over time, based on their principal balance, annual payment contributions, interest rate, investment timeframe, inflation, tax rate, fees, and savings goal.

The FERS Annuity Calculator takes these inputs and produces a year-by-year projection showing:

- Principal — your starting balance at each year

- Cumulative additions — the total of all annual contributions made

- Cumulative interest earned — the compound growth generated by investments

- Total balance — your projected account value at each milestone

Beyond the table, the FERS Annuity Calculator delivers a summary panel showing your final balance, total interest earned, total additions made, overall portfolio growth, growth ratio, and — critically — whether your projected balance achieves or falls short of your stated savings goal.

A well-designed FERS Annuity Calculator is not just a projection tool — it is a decision-making engine that lets you test different contribution amounts, return rates, fee levels, and timelines to find the combination that meets your retirement target.

Why Every Federal Employee Needs a FERS Annuity Calculator

Many federal employees assume their FERS benefit will automatically be sufficient for retirement — and this assumption, more than any other single factor, leads to underprepared retirements. The truth is that while FERS provides a strong foundation, the final retirement outcome depends heavily on personal savings decisions, contribution rates, investment choices, and the length of service — all variables that a FERS Annuity Calculator is specifically designed to model.

Here is why this tool is essential for every federal worker:

Clarity replaces assumption. Instead of estimating whether your retirement savings are “probably fine,” the FERS Annuity Calculator gives you exact projections year by year. You know precisely where you stand.

The cost of delay becomes visible. Federal employees who delay increasing their Thrift Savings Plan (TSP) contributions often do not realize how much each year of delay costs in compound growth. The FERS Annuity Calculator quantifies this cost immediately and motivates action.

Goal alignment becomes achievable. By entering a specific savings goal and running the FERS Annuity Calculator, you can see whether your current contribution rate and timeline will achieve your target — and if not, exactly what needs to change.

Fee awareness improves outcomes. Even a 0.5% management fee, compounded over 15-20 years, can reduce your final balance by tens of thousands of dollars. The FERS Annuity Calculator includes fees as a variable so you can see their true long-term cost.

Inflation-adjusted planning prevents nasty surprises. The FERS Annuity Calculator nets out inflation from your return rate, giving you real-value projections rather than nominal figures that overstate purchasing power.

Understanding FERS: The Federal Employees Retirement System Explained

FERS is the retirement system that covers most federal employees hired after January 1, 1987. It replaced the older Civil Service Retirement System (CSRS) and is structured as a three-part benefit package — a design intended to provide comprehensive retirement security when all three components work together.

The three pillars of FERS are:

The FERS Basic Benefit (Defined Benefit Annuity): This is the traditional pension component. It pays a monthly annuity for life based on a formula using your years of creditable service and your highest average salary over three consecutive years (the “High-3”). The formula is: 1% × High-3 Salary × Years of Service (or 1.1% if you retire at 62 or later with 20+ years of service).

Social Security: Unlike CSRS employees, FERS employees contribute to and earn Social Security benefits throughout their careers. This provides an additional inflation-indexed income stream in retirement.

The Thrift Savings Plan (TSP): The TSP is the federal government’s equivalent of a 401(k). Employees contribute from their salary, and the government matches contributions up to 5% of pay. The TSP component is where individual contribution decisions have the most impact — and it is the component most directly modeled by the FERS Annuity Calculator.

Understanding how all three components interact is critical to building a complete FERS retirement plan — and the FERS Annuity Calculator gives you visibility into the TSP growth trajectory that complements your fixed FERS pension and Social Security projections.

How FERS Annuity Calculations Work

The core calculation behind a FERS Annuity Calculator uses a net rate of return — the interest rate minus inflation and fees — applied to a growing balance that includes both the principal and annual payment contributions.

The mathematical model works as follows:

Net Rate = (Interest Rate % − Inflation % − Fees %) ÷ 100

For each year in the projection:

- Interest is calculated on the current balance using the net rate

- Cumulative interest is tracked as a running total

- The annual payment (contribution) is added to the balance

- The new balance is the previous balance plus the annual payment plus that year’s interest

This process repeats for each year of the projection period, producing the year-by-year table that forms the core output of the FERS Annuity Calculator.

Why net rate matters: Using a gross return rate without subtracting inflation produces projections that overstate your real purchasing power. Subtracting inflation (typically 2-3%) from your nominal return gives you a real-return projection that reflects what your savings will actually buy in future dollars. The FERS Annuity Calculator handles this automatically, giving you honest projections from the start.

Key Inputs in a FERS Annuity Calculator Explained

Each input in the FERS Annuity Calculator plays a specific role in the projection. Understanding what to enter — and why — ensures your results are accurate and actionable.

Principal ($): Your starting balance — either your current TSP account balance or the lump sum you are analyzing. The larger your principal, the more compound growth you benefit from over the entire projection period.

Annual Payment ($): The total amount you contribute to your retirement account each year. For TSP calculations, this includes both your employee contributions and the government match (up to 5% of salary).

Interest Rate (%): Your expected average annual return. For TSP investors in diversified funds, 6-8% is a commonly used long-term estimate. Enter the nominal (pre-inflation) rate here — the FERS Annuity Calculator will subtract inflation and fees to compute the net rate.

Years: The number of years the projection runs — typically from your current age to your planned retirement age.

Inflation (%): The expected annual inflation rate. This is subtracted from your interest rate to produce real-return projections. A rate of 2-3% reflects historical U.S. inflation averages.

Tax Rate (%): The percentage of returns or income subject to tax. For traditional TSP accounts, withdrawals in retirement are taxed as ordinary income. Entering a realistic effective tax rate in the FERS Annuity Calculator gives you more accurate net income projections.

Start Age and End Age: These define your investment timeline. The difference between start and end age should match your “Years” input for consistency.

Fees (%): Any annual management or advisory fees charged against your account. TSP funds are among the lowest-cost investment options available anywhere — with expense ratios as low as 0.04-0.06%. If you roll over funds to higher-fee accounts, this input becomes critically important.

Goal Amount ($): Your target retirement savings balance. The FERS Annuity Calculator compares your projected final balance to this goal and shows you whether it has been achieved or remains pending.

How to Use the FERS Annuity Calculator Step by Step

Using the FERS Annuity Calculator correctly ensures you get projections that are genuinely useful for your retirement planning decisions. Here is the process:

Step 1 — Enter your principal. Input your current TSP or annuity account balance. If you are modeling a future scenario from a current age, this is your account value today.

Step 2 — Set your annual payment. Enter the total annual contribution amount, including both your contribution and employer match. For example, if you earn $70,000 and contribute 10% with a 5% government match, your annual payment is $10,500.

Step 3 — Input your expected interest rate. Use a realistic long-term average return for your TSP fund mix. A blended portfolio of C, S, and I funds has historically delivered 7-9% annually over long periods.

Step 4 — Set the number of years. Enter the years between your current age and your planned retirement age.

Step 5 — Enter inflation and tax rate. Use 2-3% for inflation and your expected effective tax rate in retirement for the most realistic projection.

Step 6 — Add start and end ages. These should correspond to your current age and retirement age respectively.

Step 7 — Enter fees. For TSP funds, this is typically 0.05-0.06%. For external investments, enter the actual expense ratio or advisory fee.

Step 8 — Set your goal amount. Enter the total TSP balance you want to achieve at retirement. The FERS Annuity Calculator will compare your projected balance against this target.

Step 9 — Click Calculate. Your FERS Annuity Calculator will instantly produce the summary panel and year-by-year amortization table, along with a stacked bar chart visualizing principal, additions, and interest at each year milestone.

Step 10 — Test scenarios. Adjust contributions, return rates, or retirement age to discover which changes have the greatest impact on your final outcome.

Understanding Your Results: Balance, Interest, and Growth

The FERS Annuity Calculator produces six summary metrics that together tell the complete story of your retirement savings trajectory:

Balance: Your projected total account value at the end of the projection period. This is your headline number — but it must be evaluated in the context of inflation adjustment and your income needs.

Interest: The cumulative compound interest earned across the entire projection period. This figure represents the money your money made — growth generated purely by investment returns, independent of your direct contributions. In long projections, this typically exceeds total contributions significantly.

Additions: The total of all annual payments made across the projection period. This is the money you personally contributed through discipline and consistency.

Growth: The increase in value above your original principal — additions plus interest. This shows the total wealth creation generated beyond your starting balance.

Ratio: Your final balance expressed as a percentage of your original principal. A ratio of 400% means your balance has quadrupled. The FERS Annuity Calculator uses this to show the multiplier effect of long-term compounding.

Status: A clear “Achieved” or “Pending” indicator showing whether your projected balance meets your stated goal. If the status shows “Pending,” use this as a prompt to adjust your inputs — increasing contributions, extending the timeframe, or exploring higher-return options — until the FERS Annuity Calculator shows “Achieved.”

The Three-Part FERS Retirement Benefit Structure

To use the FERS Annuity Calculator most effectively, it helps to understand exactly how your TSP balance fits into the overall FERS retirement picture.

Part 1 — FERS Basic Annuity (Monthly Pension): This is your defined benefit — guaranteed monthly income for life, calculated from your service record and High-3 average salary. It forms the stable, inflation-adjusted foundation of your FERS retirement income. You cannot directly influence this calculation with the FERS Annuity Calculator — it is determined by your years of service and salary history.

Part 2 — Social Security: FERS employees earn Social Security credits throughout their careers. Benefits are paid from age 62 (at a reduced rate) or at full retirement age (66-67, depending on birth year) at full benefit. The Social Security Administration provides online benefit estimates based on your actual earnings record.

Part 3 — Thrift Savings Plan (TSP): This is the component the FERS Annuity Calculator directly models. Your TSP balance depends entirely on your contribution rate, investment choices, employer matching, and investment returns over your career. Unlike the basic annuity, the TSP is entirely within your control — which makes planning and projecting it with the FERS Annuity Calculator so important.

The financial security of your FERS retirement depends on how well all three pillars work together. A strong basic annuity plus Social Security may cover essential expenses, but a well-funded TSP — modeled and optimized with the FERS Annuity Calculator — is what funds the discretionary lifestyle, travel, healthcare cushion, and legacy goals that define a truly comfortable retirement.

How Inflation and Fees Erode Your Annuity Over Time

Two forces work silently against your retirement savings throughout your entire career: inflation and fees. Understanding both — and seeing their impact through the FERS Annuity Calculator — is essential for setting accurate retirement targets.

The impact of inflation:

At 2% annual inflation over 20 years, the purchasing power of your money decreases by approximately 33%. This means a $500,000 retirement balance today would only have the purchasing power of about $335,000 in 20 years at 2% inflation. At 3% inflation, purchasing power falls by nearly 45% over 20 years — a dramatic erosion that nominal projections completely miss.

The FERS Annuity Calculator addresses this by subtracting your inflation rate from your nominal return to compute a real net rate. This means your projected balance represents genuine purchasing power in today’s terms — a far more honest and useful figure for retirement planning.

The impact of fees:

TSP funds are extraordinarily low-cost — among the lowest expense ratios of any investment vehicle available to individual investors. But not all federal employees keep their savings in the TSP. Many roll funds to external IRAs or brokerage accounts upon leaving federal service, where fees can be substantially higher.

A seemingly small 1% annual fee compounds into an enormous loss over time. On a $20,000 principal with $10,000 annual additions at 7% return over 15 years:

- At 0.05% fees: Projected balance ≈ $282,000

- At 1.05% fees: Projected balance ≈ $251,000

- Difference: over $31,000 lost to fees alone

Use the FERS Annuity Calculator to model the exact fee impact on your specific balance before rolling funds to any external account — the numbers are frequently compelling enough to keep retirees invested in the low-cost TSP.

Real-Life Scenarios Using the FERS Annuity Calculator

Scenario 1 — The Early Career Federal Employee: Sarah, age 30, is a federal employee with a $20,000 TSP balance. She contributes $10,000 per year (including employer match), expects a 7% return, plans to retire at 45 (15-year horizon), and has a savings goal of $300,000. With 2% inflation and 0.5% fees, her FERS Annuity Calculator projects a final balance of approximately $268,000 — status: Pending. By increasing her annual contribution to $12,000, she clears the $300,000 goal and achieves her target.

Scenario 2 — The Mid-Career Catch-Up: Marcus, age 45, has $80,000 in his TSP. He contributes $15,000 per year, expects 6.5% return, and plans to retire at 62 (17 years). His inflation rate is 2.5%, fees are 0.05%, and his goal is $500,000. His FERS Annuity Calculator result shows a projected balance of approximately $521,000 — status: Achieved. He knows his current strategy is sufficient and can maintain course confidently.

Scenario 3 — The Fee Comparison: Jennifer is considering rolling her $150,000 TSP balance to a private IRA with a 1% annual fee versus keeping it in the TSP at 0.05%. Using the FERS Annuity Calculator for both scenarios over 20 years at 7% return, she discovers the high-fee IRA produces a balance approximately $85,000 lower than keeping the funds in the TSP. She keeps her money in the TSP.

FERS vs. CSRS: Key Differences Federal Employees Must Know

Federal employees hired before January 1, 1987 may be covered by the Civil Service Retirement System (CSRS) rather than FERS. Understanding the key differences matters for retirement planning — and for knowing how to best use the FERS Annuity Calculator.

CSRS provides a larger defined benefit annuity — the formula is more generous than FERS, paying up to 80% of High-3 salary for 41+ years of service. However, CSRS employees do not earn Social Security benefits from their federal employment and do not receive government matching in the TSP.

FERS provides a smaller basic annuity but combines it with Social Security and generous TSP matching — creating a three-legged stool that is broadly considered more portable and flexible for modern career patterns.

For FERS employees, the TSP component is disproportionately important relative to CSRS, precisely because the basic annuity formula is less generous. This is why accurately projecting TSP growth with the FERS Annuity Calculator is especially critical for FERS employees who want a comfortable retirement.

Maximizing Your FERS Annuity: Proven Strategies

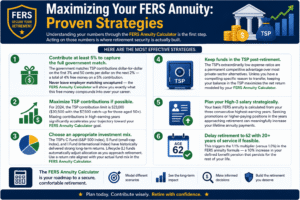

Understanding your numbers through the FERS Annuity Calculator is the first step. Acting on those numbers is where retirement security is actually built. Here are the most effective strategies:

Contribute at least 5% to capture the full government match. The government matches TSP contributions dollar-for-dollar on the first 3% and 50 cents per dollar on the next 2% — a total of 4% free money on a 5% contribution. Never leave employer matching uncaptured — the FERS Annuity Calculator will show you exactly what this free money compounds into over your career.

Maximize TSP contributions if possible. For 2024, the TSP contribution limit is $23,000 ($30,500 with the $7,500 catch-up for those aged 50+). Maxing contributions in high-earning years significantly accelerates your trajectory toward your FERS Annuity Calculator goal.

Choose an appropriate investment mix. The TSP’s C Fund (S&P 500 index), S Fund (small-cap index), and I Fund (international index) have historically delivered strong long-term returns. Lifecycle (L) funds automatically adjust allocation as you approach retirement. Use a return rate aligned with your actual fund mix in the FERS Annuity Calculator.

Keep funds in the TSP post-retirement. The TSP’s extraordinarily low expense ratios are a permanent competitive advantage over most private-sector alternatives. Unless you have a compelling specific reason to transfer, keeping your balance in the TSP maximizes the net return modeled by your FERS Annuity Calculator.

Plan your High-3 salary strategically. Your basic FERS annuity is calculated from your three consecutive highest-earning years. Seeking promotions or higher-paying positions in the years approaching retirement can meaningfully increase your lifetime annuity payments.

Delay retirement to 62 with 20+ years of service if feasible. This triggers the 1.1% multiplier (versus 1.0%) in the FERS annuity formula — a 10% increase in your defined benefit pension that persists for the rest of your life.

Common Mistakes Federal Employees Make in Retirement Planning

Even with a powerful FERS Annuity Calculator available, these errors frequently undermine federal retirement security:

Contributing only the minimum to capture the government match. While capturing the 5% match is essential, many federal employees stop there. Contributing above the match threshold is one of the highest-return financial decisions available — the FERS Annuity Calculator shows you the enormous long-term impact of every additional percentage point.

Not adjusting contributions after pay increases. Federal step increases and promotions raise your salary regularly, but many employees never update their contribution percentage. Even maintaining the same percentage means automatic dollar contribution increases with each raise.

Leaving federal service before reaching minimum retirement age. FERS employees who separate before their minimum retirement age (MRA, typically 57) may defer their annuity but sacrifice valuable years of TSP compounding and delayed annuity growth.

Using an overly optimistic return rate. The FERS Annuity Calculator is only as accurate as the return rate you enter. Using 10%+ return assumptions may produce exciting projections but creates dangerous overconfidence. Use 6-8% for diversified TSP portfolios.

Ignoring the FERS Supplement. FERS employees who retire before 62 may be eligible for a FERS Supplement that approximates what Social Security would pay for their federal service years. This temporary income bridge is often overlooked in retirement income planning.

Not using the FERS Annuity Calculator regularly. A projection made five years ago is no longer accurate. Update your FERS Annuity Calculator inputs annually to reflect your current balance, salary, contribution rate, and remaining timeline.

Frequently Asked Questions (FAQs)

What is the FERS basic annuity formula?

The standard FERS basic annuity is calculated as: 1% × High-3 Average Salary × Years of Creditable Service. If you retire at age 62 or later with at least 20 years of service, the multiplier increases to 1.1%, providing a 10% permanent increase to your monthly annuity. The FERS Annuity Calculator models your TSP balance separately from this defined benefit component.

How much should I contribute to the TSP?

At minimum, contribute 5% to capture the full government match. Beyond that, the maximum contribution for 2024 is $23,000 ($30,500 with catch-up if you are 50+). Use the FERS Annuity Calculator to model the impact of different contribution rates on your projected balance — the results almost always make a compelling case for contributing as much as cash flow allows.

What return rate should I use in the FERS Annuity Calculator?

For TSP accounts invested in a diversified mix of the C, S, and I funds, a long-term average return of 7-8% is a reasonable and historically grounded estimate. For conservative allocations (more G Fund or F Fund), use 4-5%. Always run a scenario at 2% lower than your base assumption to stress-test your plan against underperformance.

What happens to my TSP if I leave federal service before retirement?

Your TSP balance remains yours and continues to grow. You can leave it in the TSP (recommended for most retirees due to low fees), roll it to an IRA or new employer’s plan, or — at significant tax and penalty cost — cash it out. Use the FERS Annuity Calculator to project how your balance will grow if left in the TSP versus transferred to a higher-fee alternative before making this decision.

When can I start withdrawing from the TSP without penalty?

Standard TSP withdrawals without penalty are available at age 59½. FERS employees who separate from service at age 55 or older can access TSP funds without the 10% early withdrawal penalty, regardless of their age at the time of separation. Required Minimum Distributions must begin at age 73.

How does the FERS Annuity Calculator account for inflation?

The FERS Annuity Calculator subtracts your entered inflation rate from the nominal interest rate to compute a real net return rate. This means all projected balances reflect real purchasing power in terms of today’s dollars, not inflated nominal values. This is a critical feature — without inflation adjustment, projections dramatically overstate your actual retirement security.

Is the TSP better than a private IRA for FERS employees?

For most FERS employees, the TSP offers significant advantages over private IRAs: expense ratios as low as 0.04-0.06% (versus 0.5-1.5% for typical private funds), access to the unique G Fund (government bonds with no price risk), and the same investment options available to the world’s largest institutional investors. Use the FERS Annuity Calculator to model the fee differential over your specific remaining career length — the advantage of the TSP typically amounts to tens of thousands of dollars in preserved wealth.

Conclusion

Federal employment offers one of the most generous retirement packages available in the modern workforce — but that generosity only translates into financial security if you plan for it deliberately, track it accurately, and act on what the numbers tell you. The FERS Annuity Calculator is the tool that makes this possible.

By modeling your TSP growth year by year, accounting for the real-world impacts of inflation, fees, taxes, and compound returns, and comparing your projected outcome to your stated retirement goal, the FERS Annuity Calculator gives you the clarity and confidence to make every contribution decision, investment choice, and career move with full awareness of its long-term consequence.

The fundamental lessons are clear: Start contributing early and maximize employer matching. Increase your contribution rate with every salary increase. Keep fees as low as possible — the TSP’s near-zero expense ratios are a competitive advantage worth preserving. Use conservative but realistic return assumptions. And revisit the FERS Annuity Calculator every year to ensure your plan remains aligned with your goals.

Your federal career has built you a strong foundation with the FERS basic annuity and Social Security — but the TSP is the component that gives you control, flexibility, and the potential for genuine financial abundance in retirement. Use the FERS Annuity Calculator to make the most of that opportunity, every year, from your first day of service to your last.