Total Principal Invested: $0.00

Accumulated Interest Yield: $0.00

Turn your homeownership goals into reality with our Mortgage Payoff Calculator

Table of Contents

- Introduction

- What Is a Compound Interest Calculator?

- Why a Compound Interest Calculator Is Essential for Every Investor

- The Science Behind Compound Interest: How It Really Works

- Key Terms You Need to Know Before Using a Compound Interest Calculator

- How to Use the Compound Interest Calculator Step by Step

- Understanding Your Results: What the Numbers Mean

- Compounding Frequency: Why It Matters More Than You Think

- The Power of Monthly Contributions in Wealth Building

- Real-Life Examples Using the Compound Interest Calculator

- Compound Interest vs. Simple Interest: A Clear Comparison

- How Time Transforms Small Investments into Large Fortunes

- Common Mistakes to Avoid When Using a Compound Interest Calculator

- Smart Investment Strategies to Maximize Compound Growth

- Frequently Asked Questions (FAQs)

- Conclusion

Introduction

What if the secret to building life-changing wealth was not about earning more money, but about making your existing money work harder? That is the core promise of compound interest — and it is a promise that has made ordinary people extraordinarily wealthy over time. Yet most people never fully harness this power simply because they do not understand the numbers behind it.

A Compound Interest Calculator changes everything. It takes the abstract concept of exponential growth and converts it into precise, personalized projections you can actually act on. Whether you are planning for retirement, building an emergency fund, investing for your child’s future, or simply curious about what your savings could become, a Compound Interest Calculator gives you instant clarity.

In this comprehensive guide, we will walk you through everything you need to understand about compound interest — how it works, why it accelerates over time, how compounding frequency affects your returns, and how to use a Compound Interest Calculator to design a wealth-building strategy tailored to your life. By the end, you will have both the knowledge and the tool to make your financial future far more prosperous than you may have imagined.

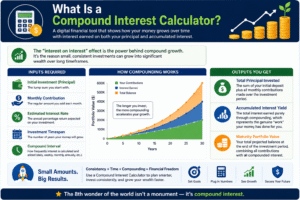

What Is a Compound Interest Calculator?

A Compound Interest Calculator is a digital financial tool that calculates how an investment or savings balance grows over time when interest is earned not just on the original principal, but also on the accumulated interest from previous periods.

This “interest on interest” effect is what sets compound growth apart from simple growth — and it is the mechanism that causes small, consistent investments to balloon into significant wealth over long timeframes.

A well-built Compound Interest Calculator typically requires the following inputs:

- Initial Investment (Principal) — the lump sum you start with

- Monthly Contribution — the regular amount you add each month

- Estimated Interest Rate — the annual percentage return expected on your investment

- Investment Timespan — the number of years your money will grow

- Compound Interval — how frequently interest is calculated and added (daily, weekly, monthly, annually, etc.)

From these inputs, the Compound Interest Calculator delivers three critical outputs:

Total Principal Invested — the sum of your initial deposit plus all monthly contributions made over the investment period.

Accumulated Interest Yield — the total interest earned purely through compounding, which represents the genuine “work” your money has done for you.

Maturity Portfolio Value — your total projected balance at the end of the investment period, combining all contributions with all compounded interest.

Why a Compound Interest Calculator Is Essential for Every Investor

Most people dramatically underestimate the power of compound growth — and that underestimation costs them years of financial progress. A Compound Interest Calculator solves this problem by making the invisible visible.

Here is why every investor, saver, and financially aware person should use one regularly:

It replaces guesswork with certainty. Instead of vague hopes that your savings will “grow nicely,” the Compound Interest Calculator gives you exact figures — down to the cent.

It shows you the true cost of waiting. Delaying your investment by even five years can cost you more in lost compound growth than an entire decade of contributions later. The Compound Interest Calculator makes this stark reality visible and motivates action.

It helps you set smarter financial goals. Once you know exactly how much your current savings trajectory will produce, you can work backwards — adjusting your contribution, rate of return, or timeframe — to hit a specific target.

It makes the abstract concrete. Compound interest is a mathematical concept. The Compound Interest Calculator transforms it into your own personal projection, making it feel real and actionable rather than theoretical.

It empowers better investment decisions. When you can compare two investment products side by side using a Compound Interest Calculator — one at 6% and one at 8%, for example — the difference in long-term outcomes becomes immediately clear, enabling smarter, more informed choices.

The Science Behind Compound Interest: How It Really Works

Compound interest is often described as “interest on interest” — and that description, while simple, captures the essence of one of the most powerful forces in personal finance.

Here is the core formula that powers every Compound Interest Calculator:

A = P × (1 + r/n)^(nt)

Where:

- A = the future value of the investment

- P = the initial principal

- r = the annual interest rate (as a decimal)

- n = the number of times interest compounds per year

- t = the time in years

What makes this formula so powerful is the exponent. When time (t) or compounding frequency (n) increases, the result does not grow in a straight line — it curves upward exponentially.

Consider a simple example: You invest $10,000 at an 8% annual return, compounded monthly, for 10 years with no additional contributions.

- After Year 1: $10,830

- After Year 5: $14,898

- After Year 10: $22,196

- After Year 20: $49,268

- After Year 30: $109,357

Notice how the growth accelerates dramatically in the later years. In the first 10 years, your money doubled. In the next 10, it more than doubled again — without a single extra dollar contributed. This acceleration is the defining characteristic of compound growth, and it is why a Compound Interest Calculator is so important for long-term planning.

Key Terms You Need to Know Before Using a Compound Interest Calculator

Before you enter a single number, make sure you understand these essential concepts:

Principal: Your starting investment amount. The larger your principal, the more powerful the compounding effect from day one.

Annual Interest Rate (APR / APY): The percentage return your investment earns per year. APR is the nominal rate without compounding effects factored in. APY (Annual Percentage Yield) already accounts for compounding, so use it in your Compound Interest Calculator for greater accuracy.

Compounding Frequency: How often your interest is calculated and added to your balance. Options range from daily to annually — and more frequent compounding always produces a higher return at the same stated rate.

Investment Timespan: The number of years your money remains invested. Time is the single most powerful variable in compound growth — extending your investment horizon even by a few years produces dramatically better outcomes.

Monthly Contribution: The regular amount you add to your investment each period. Consistent contributions turbocharge compounding because each new dollar immediately begins earning compound returns.

Future Value: The total projected value of your investment at the end of the period — the final output of any Compound Interest Calculator.

Accumulated Interest Yield: The portion of your future value that came purely from compounding — the money your money made, independent of your contributions.

How to Use the Compound Interest Calculator Step by Step

Getting accurate, useful results from a Compound Interest Calculator is straightforward — but the quality of your inputs determines the quality of your projections. Follow these steps:

Step 1 — Enter your initial investment. Input the amount you are starting with today. This could be existing savings, a bonus, an inheritance, or any lump sum you plan to invest immediately.

Step 2 — Set your monthly contribution. Enter the amount you plan to contribute each month going forward. Even a modest regular contribution can produce remarkable results over time.

Step 3 — Input your estimated interest rate. Use a realistic, conservative estimate. For stock market investments, historical average returns of 7-10% are commonly cited, but nothing is guaranteed. For savings accounts or bonds, use the current advertised rate.

Step 4 — Set your investment timespan. Enter the number of years you plan to leave the money invested. For retirement planning, this is typically your current age subtracted from your target retirement age.

Step 5 — Choose your compounding interval. Select how frequently your interest compounds. Monthly is most common for savings accounts and many investment products. Daily compounding is used by some high-yield accounts and will produce slightly higher results than monthly.

Step 6 — Click “Calculate Return.” The Compound Interest Calculator will instantly display your total principal invested, your accumulated interest yield, and your projected maturity portfolio value.

Step 7 — Test different scenarios. Change your monthly contribution, adjust the interest rate, or extend the timespan to see how each variable affects your outcome. This scenario testing is where the real power of the Compound Interest Calculator lies — it allows you to find the combination of inputs that meets your specific financial goal.

Understanding Your Results: What the Numbers Mean

When your Compound Interest Calculator returns its results, here is how to interpret each figure meaningfully:

Total Principal Invested tells you how much money you personally put in across the entire investment period. This is the baseline — what you actually contributed through discipline and sacrifice.

Accumulated Interest Yield is the number that tells the real story. This is the money your money made — generated entirely through compounding without any additional effort from you. In long-term investments, this figure often exceeds total contributions by a significant multiple.

Maturity Portfolio Value is your bottom line — the total projected wealth at the end of your investment period.

Here is an eye-opening example: $10,000 initial investment, $200 monthly contribution, 8% annual return, compounded monthly for 30 years:

- Total principal invested: $82,000

- Accumulated interest yield: $227,000+

- Maturity portfolio value: $309,000+

The accumulated interest nearly triples your total contributions — purely because of the compounding effect over time. This is the fundamental insight the Compound Interest Calculator delivers, and it is the most compelling argument for starting early and staying consistent.

Compounding Frequency: Why It Matters More Than You Think

One of the most underappreciated inputs in a Compound Interest Calculator is compounding frequency — how often your interest is calculated and added to your balance.

At the same stated annual interest rate, more frequent compounding always produces more growth. Here is how different frequencies compare on a $10,000 investment at 8% over 10 years:

- Annually: Final value ≈ $21,589

- Quarterly: Final value ≈ $22,080

- Monthly: Final value ≈ $22,196

- Daily: Final value ≈ $22,254

While the difference between monthly and daily compounding is modest, the difference between annual and daily compounding is over $665 on a $10,000 investment over 10 years — and that gap widens significantly at higher principal amounts and longer timespans.

When comparing savings accounts, investment platforms, or financial products, always use your Compound Interest Calculator to compare the actual projected outcomes at each compounding frequency rather than relying solely on the stated rate. The frequency can meaningfully change your final result, especially over decades.

The Power of Monthly Contributions in Wealth Building

Many people believe they need a large lump sum to benefit meaningfully from compound interest. The Compound Interest Calculator reveals the truth: consistent monthly contributions are often more powerful than a single large deposit.

Here is why: every monthly contribution immediately starts compounding on its own schedule. The money you add in month one grows for nearly the full remaining period. The money you add in month 12 still has years to compound. The aggregate effect of hundreds of small, consistent contributions compounds into a financial force that dwarfs the original investment.

Consider two investors, both over 25 years:

Investor A deposits $50,000 as a single lump sum and adds nothing monthly. Investor B deposits $5,000 and adds $300 per month consistently.

At 8% annual return, compounded monthly:

- Investor A: ≈ $342,424

- Investor B: ≈ $311,822

The results are remarkably close despite Investor B contributing far less upfront — because the regular monthly additions create their own compounding engine running in parallel to the principal.

Run your own comparison in the Compound Interest Calculator to find the perfect balance between a lump sum deposit and ongoing contributions given your specific financial situation.

Real-Life Examples Using the Compound Interest Calculator

Example 1 — The Early Starter: Emma, age 22, invests $5,000 and adds $150 per month at 7% annual return, compounded monthly, until age 62 (40 years). Her Compound Interest Calculator projection shows a maturity value exceeding $400,000 — on total contributions of just under $77,000. Compounding did the rest.

Example 2 — The Consistent Saver: David, age 35, has $20,000 saved and contributes $500 per month at 6% for 25 years. His Compound Interest Calculator result shows a final portfolio value of approximately $367,000 — with over $197,000 coming purely from compound interest.

Example 3 — The High-Frequency Optimizer: Lisa uses the Compound Interest Calculator to compare monthly versus daily compounding on her $50,000 investment at 5% over 20 years. Daily compounding adds approximately $1,400 more than monthly — a meaningful difference simply from choosing the right account type.

Compound Interest vs. Simple Interest: A Clear Comparison

Understanding the difference between compound and simple interest is fundamental to appreciating why a Compound Interest Calculator is so valuable.

Simple interest is calculated only on the original principal. If you invest $10,000 at 8% simple interest for 10 years, you earn $800 per year — exactly $8,000 in interest — regardless of how long it has been invested. There is no acceleration.

Compound interest calculates interest on both the principal and the previously accumulated interest. The same $10,000 at 8% compounded annually for 10 years grows to $21,589 — yielding $11,589 in interest rather than $8,000.

The difference of $3,589 is entirely attributable to compounding — interest earned on interest, year after year.

Over 30 years, the gap becomes staggering:

- Simple interest: $10,000 + $24,000 = $34,000

- Compound interest (annual): $100,627

A Compound Interest Calculator makes this comparison instantly visible and drives home why the type of return on your investment matters as much as the rate itself.

How Time Transforms Small Investments into Large Fortunes

If there is one lesson the Compound Interest Calculator teaches above all others, it is this: time is the most valuable asset in any investment plan — more valuable than the amount you invest, more valuable than the rate you earn.

The Rule of 72 is a useful shortcut for understanding this: divide 72 by your annual interest rate to find how many years it takes to double your money.

- At 6%: Money doubles every 12 years

- At 8%: Money doubles every 9 years

- At 10%: Money doubles every 7.2 years

This means an investment at 8% will double approximately three times over 27 years — multiplying your original capital by a factor of eight. Use the Compound Interest Calculator to see exactly how many times your money will double over your chosen investment horizon.

Starting 10 years earlier can easily result in two to three times more wealth at retirement — even with identical contribution amounts and returns. This is why financial advisors universally recommend beginning to invest as early as possible, and why the Compound Interest Calculator is such a powerful motivator for young investors who see what starting in their twenties means versus their thirties.

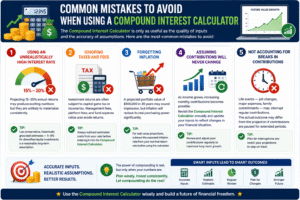

Common Mistakes to Avoid When Using a Compound Interest Calculator

The Compound Interest Calculator is only as useful as the quality of inputs and the accuracy of assumptions. Here are the most common mistakes to avoid:

Using an unrealistically high interest rate. Projecting 15-20% annual returns may produce exciting numbers, but they are unlikely to materialize consistently. Use conservative, historically grounded estimates — 5-8% for diversified equity investments is a reasonable long-term assumption.

Ignoring taxes and fees. Investment returns are often subject to capital gains tax or income tax. Management fees, platform fees, and fund expense ratios also erode returns. Always subtract estimated costs from your rate before entering it into the Compound Interest Calculator.

Forgetting inflation. A projected portfolio value of $500,000 in 30 years may sound impressive, but inflation will reduce its real purchasing power significantly. For real-value projections, subtract the expected inflation rate from your nominal return rate before using the calculator.

Assuming contributions will never change. As income grows, increasing monthly contributions becomes possible. Revisit the Compound Interest Calculator annually and update your inputs to reflect changes in your financial situation.

Not accounting for breaks in contributions. Life events — job changes, major expenses, family commitments — may interrupt regular contributions. The actual outcome may differ from the projection if contributions are paused for extended periods.

Smart Investment Strategies to Maximize Compound Growth

Understanding the math is the first step. Acting on it is where wealth is actually built. Here are the most effective strategies to maximize the results you see in your Compound Interest Calculator:

Start immediately, no matter how small. The earlier you begin, the more time compounding has to work. Even $50 per month starting at age 20 builds into a vastly larger sum than $500 per month starting at 40.

Automate your contributions. Set up automatic monthly transfers to your investment account. Automation removes friction, removes temptation, and ensures your compounding timeline is never interrupted.

Reinvest all interest and dividends. Never withdraw interest or dividends during the growth phase. Reinvesting keeps the full compounding engine running at maximum power.

Choose higher-frequency compounding accounts. When comparing accounts with similar stated rates, always choose the one that compounds more frequently. Use the Compound Interest Calculator to quantify the advantage.

Increase contributions with every income increase. Direct a fixed percentage of every pay rise directly into your investment account before lifestyle inflation absorbs it.

Minimize fees relentlessly. A 1% reduction in annual fees is equivalent to earning 1% more in returns. Over 30 years, this difference is enormous. The Compound Interest Calculator can help you quantify exactly what each percentage point in fees costs you over your investment timeline.

Stay invested through market volatility. Compound growth requires staying in the market during downturns. Selling during volatility locks in losses and destroys compounding continuity.

Frequently Asked Questions (FAQs)

What is the difference between APR and APY in a Compound Interest Calculator?

APR (Annual Percentage Rate) is the nominal interest rate without compounding effects. APY (Annual Percentage Yield) already factors in compounding and represents the effective annual return. When using a Compound Interest Calculator, using the APY gives you a more accurate projection if the account compounds more frequently than annually.

How often should I use a Compound Interest Calculator?

Review your projections at least once a year — or whenever your income changes, your interest rate changes, or you receive a lump sum you plan to invest. Regular recalculation keeps your strategy current and your motivation high.

Is a higher compounding frequency always better?

Yes — at the same stated annual interest rate, more frequent compounding always produces a higher return. Daily compounding will always outperform monthly, which outperforms quarterly, which outperforms annually. Use your Compound Interest Calculator to compare the actual projected difference before choosing between two accounts.

Can I use the Compound Interest Calculator for retirement planning?

Absolutely. Enter your current age, target retirement age (as your investment timespan), current savings as principal, and expected monthly contribution. Use a conservative annual return estimate of 5-7% for a diversified retirement portfolio. The Compound Interest Calculator will show you your projected retirement balance and whether your current strategy is sufficient.

What happens if I miss monthly contributions for a period?

Missing contributions does not destroy your plan — but it does reduce your final outcome. The principal already invested continues to compound, but the “missed” contributions are simply absent from the calculation. When you resume, re-run the Compound Interest Calculator with an updated principal (current balance) and remaining timespan to get a fresh projection.

How does inflation affect my compound interest projections?

The Compound Interest Calculator shows nominal growth — the raw dollar value of your future portfolio. Inflation reduces the real purchasing power of that amount over time. To account for inflation, subtract the expected inflation rate from your nominal interest rate before entering it into the Compound Interest Calculator. For example, at 8% nominal return with 2.5% inflation, use 5.5% as your effective real return rate.

Should I prioritize paying off debt or investing for compound growth?

This depends on the interest rate of your debt versus your expected investment return. If your debt carries an interest rate higher than your expected investment return — for example, a credit card at 20% versus an investment at 8% — paying off the debt first delivers a guaranteed return that cannot be beaten. Use the Compound Interest Calculator to compare the projected investment outcome against the guaranteed savings from debt repayment to make the right choice for your situation.

Conclusion

Compound interest is not a complicated concept — but its outcomes are extraordinary. A small amount of money, invested consistently over a long period at a reasonable rate of return, can grow into a fortune that transforms your financial life. The mathematics are precise, the results are predictable, and the only variable you truly control is whether you start.

The Compound Interest Calculator puts the full power of this mathematical reality into your hands. It shows you the exact outcome of your current savings strategy, reveals the true cost of waiting, and empowers you to experiment with different scenarios until you find a plan that genuinely excites and motivates you.

The most important takeaways are simple: Start as early as possible. Contribute consistently. Choose accounts that compound frequently. Minimize fees and taxes. Reinvest everything during the growth phase. And revisit the Compound Interest Calculator regularly to keep your plan aligned with your goals.

Your future wealth is not determined by luck or circumstance — it is determined by the choices you make today. Use the Compound Interest Calculator, understand your numbers, make your plan, and let the most powerful force in personal finance work in your favor every single day.