Refinance Calculator

Calculate boat loan payments, interest costs, and financing estimates with our Boat Loan Calculator

Table of Contents

- Introduction

- What Is a Refinance Home Loan Calculator?

- Why Refinancing Your Mortgage Could Be a Smart Move

- How a Refinance Home Loan Calculator Works

- Understanding Your Current Loan Details

- Analyzing Your New Loan Options

- Key Metrics the Calculator Reveals

- The Amortization Schedule Explained

- When Is the Right Time to Refinance?

- Common Refinancing Mistakes to Avoid

- How to Use Our Refinance Home Loan Calculator Step-by-Step

- Tips to Get the Best Refinance Rate

- Frequently Asked Questions (FAQs)

- Conclusion

Introduction

Your home loan is likely the largest financial commitment of your life — and paying more interest than necessary on that loan can cost you tens of thousands of dollars over time. For millions of homeowners, refinancing offers a powerful opportunity to reduce monthly payments, lower interest rates, shorten loan terms, or access built-up home equity for other financial needs.

But here is the challenge: refinancing is not always the right move, and the decision must be based on hard numbers rather than optimism. This is exactly why a Refinance Home Loan Calculator is an indispensable tool for every homeowner considering a new mortgage arrangement.

In this comprehensive guide, we break down everything you need to know about using a Refinance Home Loan Calculator intelligently. You will learn how refinancing works, what inputs the calculator needs, how to interpret the results, when refinancing makes financial sense, and what traps to avoid. Whether you are a first-time refinancer or someone who has done it before, this guide will help you make the most informed decision possible.

By the end, you will know exactly how to use our free, powerful Refinance Home Loan Calculator to compare your current loan against a new loan option — complete with a side-by-side analysis, amortization schedules, and visual breakdowns.

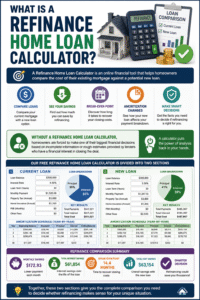

What Is a Refinance Home Loan Calculator?

A Refinance Home Loan Calculator is an online financial tool that helps homeowners compare the cost of their existing mortgage against a potential new loan. It takes the key details of both loans — including the principal balance, interest rate, loan term, monthly payment, fees, taxes, and insurance — and calculates a complete financial picture for each scenario.

The purpose of a Refinance Home Loan Calculator is straightforward: it shows you whether refinancing will save you money, how much it will save, how long it takes to recover the closing costs (the “break-even point”), and how your amortization schedule changes under the new loan structure.

Without a Refinance Home Loan Calculator, homeowners are forced to make one of their biggest financial decisions based on incomplete information or rough estimates provided by lenders who have a financial interest in closing the deal. A calculator puts the power of analysis back in your hands.

Our free Refinance Home Loan Calculator is divided into two sections — your Current Loan and your New Loan — each producing a detailed results summary, a pie chart showing the principal-to-interest ratio, and a full year-by-year amortization table. Together, these two sections give you the complete comparison you need to decide whether refinancing makes sense for your unique situation.

Why Refinancing Your Mortgage Could Be a Smart Move

Refinancing is not just about getting a lower interest rate — though that is often the primary motivation. There are several compelling reasons why homeowners choose to refinance, and a Refinance Home Loan Calculator helps you evaluate the financial impact of each:

Reduce Your Monthly Payment: If interest rates have fallen since you took out your original mortgage, refinancing to a lower rate can significantly reduce your monthly payment — freeing up hundreds of dollars in cash each month for savings, investment, or other expenses.

Lower Your Total Interest Cost: Even a small reduction in your interest rate can save tens of thousands of dollars over the life of the loan. A Refinance Home Loan Calculator shows you exactly how much interest you will pay under each scenario, making the long-term savings immediately visible.

Shorten Your Loan Term: Refinancing from a 30-year mortgage to a 15-year mortgage increases monthly payments slightly but dramatically reduces total interest paid and builds equity much faster.

Switch from Adjustable to Fixed Rate: If you currently have an adjustable-rate mortgage (ARM) and are concerned about future rate increases, refinancing into a fixed-rate loan locks in your interest rate and provides payment certainty for the life of the loan.

Access Home Equity: A cash-out refinance allows you to borrow against your home’s equity — useful for funding home renovations, consolidating high-interest debt, or covering major expenses. A Refinance Home Loan Calculator helps you model how a larger loan amount affects your monthly payments and total cost.

Eliminate Private Mortgage Insurance (PMI): If your home has appreciated significantly since you purchased it, refinancing can help you eliminate PMI by resetting your loan-to-value ratio below the 80% threshold.

How a Refinance Home Loan Calculator Works

A Refinance Home Loan Calculator works by processing two parallel sets of loan data — your current mortgage details and your proposed new loan details — and producing a complete financial analysis for each.

The calculation process for each loan follows this flow:

First, the calculator takes your principal balance (or new loan amount) and applies the interest rate over the loan term to determine the total interest you will pay. It then factors in your monthly payment amount and calculates how your balance decreases over time through the amortization process.

For the current loan section, the calculator captures your remaining balance, current interest rate, remaining years on the loan, current monthly payment, and any origination or miscellaneous fees still associated with the loan.

For the new loan section, it captures the new loan amount (which may be different from the current balance if you are doing a cash-out refinance or rolling closing costs into the loan), the new interest rate, the new loan term, the projected monthly payment, property taxes, insurance, lender fees, and total closing costs.

Once both sets of data are entered and calculated, you can compare the results side by side — monthly payment difference, total interest difference, and how the amortization schedule changes. This is the core value of a Refinance Home Loan Calculator: it turns complexity into clarity.

Understanding Your Current Loan Details

Accurate input is the foundation of accurate results. When entering your current loan details into the Refinance Home Loan Calculator, here is what each field means and where to find the information:

Loan Balance: This is your current outstanding mortgage balance — not the original loan amount. You can find this on your most recent mortgage statement or by logging into your lender’s online portal.

Interest Rate: Your current annual interest rate, expressed as a percentage. This is also on your mortgage statement or loan documents. If you have an ARM, use your current effective rate, not the initial teaser rate.

Loan Years: The remaining years left on your current mortgage. If you took out a 30-year mortgage 7 years ago, you have 23 years remaining.

Monthly Payment: Your current principal and interest payment. Do not include escrow amounts for taxes and insurance unless the calculator specifically asks for them separately.

Origination Fees: Any fees originally paid to obtain the current loan that may still be factored into your analysis. These are typically listed in your original loan documentation.

Miscellaneous Fees: Any other costs associated with your current loan — prepayment penalties, service fees, or other charges that would apply if you refinance.

Entering these figures accurately into the Refinance Home Loan Calculator ensures that the comparison with your new loan option is based on your real financial reality, not estimates or approximations.

Analyzing Your New Loan Options

The new loan section of our Refinance Home Loan Calculator is where you model your refinancing scenario. Here is a breakdown of each field and why it matters:

New Loan Amount: The total amount you are borrowing under the new loan. This may be equal to your current balance (rate-and-term refinance), higher (cash-out refinance), or slightly higher if you roll closing costs into the loan.

New Interest Rate: The rate your lender is offering for the refinanced loan. Even a 0.5% reduction in interest rate can produce significant savings over the remaining loan term — and the Refinance Home Loan Calculator quantifies exactly how much.

New Loan Term: The number of years for your new mortgage. Choosing a shorter term increases monthly payments but reduces total interest dramatically. Choosing a longer term reduces monthly payments but increases total interest cost.

Projected Monthly Payment: What your new monthly payment will be. You can enter a quote from your lender or let the amortization table help you verify it.

Property Tax: Your annual property tax divided by 12, if you want the calculator to reflect your full housing cost including escrow.

Insurance: Your monthly homeowner’s insurance premium. Like property taxes, this is part of your total monthly housing cost even though it is not technically part of the loan payment.

Lender Fees: Underwriting fees, application fees, and other lender-side charges that increase the true cost of the new loan.

Closing Costs: The total transaction costs associated with completing the refinance — title search, appraisal, attorney fees, recording fees, and other third-party charges. Closing costs typically range from 2% to 5% of the new loan amount and are one of the most important factors in determining whether refinancing is financially worthwhile.

Key Metrics the Calculator Reveals

Once you run both sections of the Refinance Home Loan Calculator, you get a series of results that tell the complete story of your refinancing decision:

Monthly Payment Comparison: The most immediately visible metric — how much your monthly payment changes between your current loan and the new loan. A lower monthly payment improves monthly cashflow but may extend the loan term.

Total Interest Paid: The cumulative interest cost over the full remaining life of each loan. This figure often reveals surprising differences that are invisible when you only compare monthly payments.

Other Costs: All fees, taxes, insurance, and closing costs bundled into a total cost figure for each loan scenario. This ensures you are comparing true total cost, not just the interest rate.

Break-Even Point: The number of months it takes for your monthly savings from the new loan to offset the upfront closing costs of refinancing. If you plan to stay in the home longer than the break-even point, refinancing almost certainly makes financial sense.

Principal-to-Interest Ratio: Visualized as a pie chart, this shows what proportion of your total loan cost is principal (the actual money you borrowed) versus interest (the cost of borrowing). A good Refinance Home Loan Calculator makes this ratio immediately visible and comparable between both loans.

Amortization Progress: How quickly your balance decreases under each loan structure — a key indicator of equity building speed.

The Amortization Schedule Explained

One of the most powerful features of our Refinance Home Loan Calculator is the year-by-year amortization table generated for both the current loan and the new loan. Understanding this table is essential for making the right decision.

An amortization schedule shows exactly how each payment is split between principal repayment and interest for every year of the loan. In the early years of a mortgage, the vast majority of each payment goes toward interest — not principal. This is why refinancing an older loan into a new long-term loan can sometimes increase total interest cost even when the rate is lower.

Our amortization table displays four columns: Year, Interest Paid, Principal Paid, and Remaining Balance. By tracking these figures annually over the life of the loan, you can see:

How quickly equity builds: A shorter loan term or lower interest rate accelerates equity accumulation, which has significant implications for your net worth over time.

Where you are in the interest-heavy phase: If you are already past the halfway point on a 30-year mortgage, refinancing into a new 30-year loan restarts the interest-heavy phase and may cost you more in total interest even at a lower rate.

The impact of extra payments: The amortization schedule helps you model what happens if you make additional principal payments — a strategy that dramatically reduces total interest cost and loan duration.

Always review the amortization tables from both sections of the Refinance Home Loan Calculator before making your final decision. The monthly savings may look attractive, but the full amortization picture reveals the true long-term cost of each option.

When Is the Right Time to Refinance?

Timing is everything in refinancing. A Refinance Home Loan Calculator helps you evaluate the numbers, but here are the general conditions that make refinancing most financially advantageous:

Interest Rates Have Dropped Significantly: The traditional rule of thumb is that refinancing makes sense when you can reduce your rate by at least 1%. However, even a 0.5% reduction can justify refinancing if your loan balance is large enough. Use the Refinance Home Loan Calculator to find your personal break-even point.

Your Credit Score Has Improved: If your credit score has risen significantly since you took out your original mortgage, you may now qualify for substantially better rates than you received initially.

You Plan to Stay in the Home Long-Term: Refinancing involves upfront closing costs that take time to recover through monthly savings. If you plan to sell the home soon, refinancing may cost more than it saves.

You Want to Change Loan Structure: Switching from a 30-year to a 15-year mortgage, or from an ARM to a fixed rate, can be the right move regardless of whether rates have dropped — and the Refinance Home Loan Calculator helps you model the payment impact.

You Need to Access Equity: If home values have risen and you need capital for renovations or debt consolidation, a cash-out refinance may be appropriate. Run the new loan amount through the Refinance Home Loan Calculator to understand the full cost.

Common Refinancing Mistakes to Avoid

Even with the best intentions, homeowners make costly mistakes when refinancing. Here are the most common errors — all of which a Refinance Home Loan Calculator helps you avoid:

Focusing Only on the Monthly Payment: A lower monthly payment looks attractive, but if it comes with a longer loan term, you could pay significantly more in total interest over time. Always compare total interest cost, not just the monthly figure.

Ignoring Closing Costs: Closing costs of 2% to 5% of the loan amount are a real and substantial expense. Homeowners who ignore these costs overestimate their savings dramatically.

Restarting the Loan Clock Unnecessarily: Refinancing a 25-year-old loan into a new 30-year loan resets your amortization schedule and can add years of interest payments. Use the Refinance Home Loan Calculator to model a shorter term that maintains your equity trajectory.

Not Shopping Multiple Lenders: Accepting the first refinance offer without comparing rates and fees from multiple lenders can cost thousands of dollars. Get at least three quotes before deciding.

Refinancing Too Frequently: Each refinance resets closing costs and can interrupt your equity-building progress. Refinance strategically, not habitually, and always verify the break-even timeline.

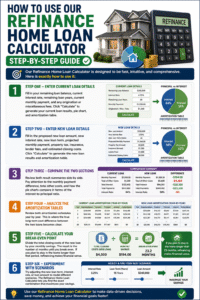

How to Use Our Refinance Home Loan Calculator Step-by-Step

Our Refinance Home Loan Calculator is designed to be fast, intuitive, and comprehensive. Here is exactly how to use it:

Step One – Enter Current Loan Details: Fill in your remaining loan balance, current interest rate, remaining loan years, current monthly payment, and any origination or miscellaneous fees. Click “Calculate” to generate your current loan results, pie chart, and amortization table.

Step Two – Enter New Loan Details: Fill in the proposed new loan amount, new interest rate, new loan term, projected monthly payment, property tax, insurance, lender fees, and estimated closing costs. Click “Calculate” to generate the new loan results and amortization table.

Step Three – Compare the Two Sections: Review both result summaries side by side. Pay attention to the monthly payment difference, total other costs, and how the pie charts compare in terms of the interest-to-principal ratio.

Step Four – Analyze the Amortization Tables: Review both amortization schedules year by year. This is where the true long-term cost difference between the two loans becomes clear.

Step Five – Calculate Your Break-Even Point: Divide the total closing costs of the new loan by your monthly savings. The result is the number of months until you break even. If you plan to stay in the home longer than that period, refinancing makes financial sense.

Step Six – Experiment with Scenarios: Try adjusting the new loan term, interest rate, or loan amount to model different scenarios. The Refinance Home Loan Calculator lets you find the exact combination that maximizes your savings.

Tips to Get the Best Refinance Rate

Getting the best possible rate on your refinanced mortgage significantly improves the numbers in your Refinance Home Loan Calculator. Here is how to position yourself for the lowest rate available:

Improve Your Credit Score Before Applying: Pay down credit card balances, avoid new credit inquiries, and resolve any errors on your credit report. Even a 20-point improvement in your score can qualify you for a meaningfully better rate.

Increase Your Home Equity: Lenders offer the best rates to borrowers with at least 20% equity. If you are close to this threshold, consider making extra principal payments before refinancing.

Compare Offers from Multiple Lenders: Rates and fees vary significantly from lender to lender. Compare offers from banks, credit unions, mortgage brokers, and online lenders before choosing.

Lock Your Rate at the Right Time: Mortgage rates fluctuate daily based on economic conditions. Use the Refinance Home Loan Calculator to model different rate scenarios so you know exactly what rate you need to make refinancing worthwhile, and lock in when rates hit that target.

Negotiate Lender Fees: Unlike the interest rate, many lender fees are negotiable. Do not hesitate to ask lenders to waive or reduce origination fees, application fees, or other charges.

Consider Paying Points: Paying discount points upfront to buy down your interest rate can make sense if you plan to stay in the home for many years. Run the break-even analysis in your Refinance Home Loan Calculator to determine whether paying points is worthwhile.

Frequently Asked Questions (FAQs)

What is a Refinance Home Loan Calculator? A Refinance Home Loan Calculator is a free online tool that helps homeowners compare their current mortgage against a potential new loan. It calculates monthly payments, total interest costs, amortization schedules, and the break-even point for refinancing costs.

Is the Refinance Home Loan Calculator free to use? Yes. Our Refinance Home Loan Calculator is completely free with no registration or account required. Simply enter your loan details and get instant, detailed results.

How much can I save by refinancing? Savings depend on your current interest rate, new rate, remaining loan balance, and loan term. Use the Refinance Home Loan Calculator to calculate your personalized savings — results vary significantly from case to case.

What is the break-even point and why does it matter? The break-even point is the number of months it takes for your monthly savings from the new loan to offset the upfront closing costs. If you plan to stay in your home longer than this period, refinancing is likely worth it. The Refinance Home Loan Calculator helps you identify this timeline clearly.

What closing costs should I expect when refinancing? Closing costs typically range from 2% to 5% of the new loan amount and include appraisal fees, title insurance, lender fees, attorney fees, and recording costs. Enter these in the Refinance Home Loan Calculator to see how they affect your break-even point.

Can I refinance if I have bad credit? Refinancing with poor credit is challenging and typically results in higher interest rates. Work on improving your credit score before using the Refinance Home Loan Calculator to evaluate realistic options.

Should I choose a 15-year or 30-year refinance? It depends on your financial goals. A 15-year loan builds equity faster and costs less in total interest but has higher monthly payments. A 30-year loan has lower monthly payments but higher total interest cost. Model both options in the Refinance Home Loan Calculator to compare.

What is a cash-out refinance? A cash-out refinance replaces your current mortgage with a larger loan, allowing you to receive the difference in cash. You can use these funds for home improvements, debt consolidation, or other needs. Enter the new larger loan amount in the Refinance Home Loan Calculator to understand the full cost impact.

How often can I refinance? There is no strict legal limit, but refinancing too frequently resets closing costs and can disrupt your equity progress. Most financial advisors recommend waiting at least 12 to 24 months between refinances.

Does refinancing affect my credit score? Yes, refinancing involves a hard credit inquiry which can temporarily lower your score by a few points. However, successfully refinancing to a lower rate and payment can improve your long-term financial health significantly.

Conclusion

Your mortgage should work for you — not against you. With interest rates constantly shifting and home values changing, refinancing at the right moment and under the right terms can save you a substantial amount of money and dramatically improve your financial position.

Our free Refinance Home Loan Calculator gives you the complete, data-driven picture you need to make this critical decision with confidence. By entering your current and new loan details side by side, you get instant clarity on monthly payment differences, total interest savings, closing cost recovery timelines, and how your amortization schedule changes — all without leaving your home or paying a financial advisor.

Whether your goal is to reduce your monthly payment, shorten your loan term, switch to a fixed rate, or access your home equity, the Refinance Home Loan Calculator is your starting point. It replaces guesswork with precision and transforms one of the most complex financial decisions of homeownership into something clear, manageable, and actionable.

Do not let another month pass paying more on your mortgage than you have to. Run your numbers through the Refinance Home Loan Calculator today, compare your current loan against the best new loan option available, and take the first confident step toward a smarter mortgage and a stronger financial future.

Your home is your most valuable asset. Make sure your loan reflects that value.