See How Much Your Money Could Grow with Our Future Value Calculator

Table of Contents

- Introduction

- What Is a Mortgage Calculator UK?

- How the UK Mortgage Market Works

- Key Inputs Every Mortgage Calculator UK Requires

- Understanding Fixed Rate vs. Standard Variable Rate (SVR)

- How Loan-to-Value Ratio Affects Your Mortgage

- Product Fees and Their Hidden Impact on Total Cost

- Extra Payments – The Fastest Route to Mortgage Freedom

- Tax Rate and Inflation – The Wider Financial Picture

- How to Read Your Amortization Table

- Understanding the Balance Chart

- First-Time Buyers in the UK – What You Need to Know

- How to Use Our Mortgage Calculator UK Step-by-Step

- Tips to Get the Best Mortgage Deal in the UK

- Common Mortgage Mistakes UK Buyers Make

- Frequently Asked Questions (FAQs)

- Conclusion

Introduction

Buying property in the United Kingdom is one of the largest financial decisions most people will ever make — and navigating the UK mortgage market without the right tools can cost you thousands of pounds in unnecessary interest, product fees, and poor rate choices. From understanding the difference between a fixed-rate deal and the Standard Variable Rate to calculating how extra payments affect your long-term balance, the complexity of UK mortgage planning demands more than a rough estimate.

A Mortgage Calculator UK is the essential tool that makes all of this clear. It processes your property value, loan amount, deposit, loan term, fixed-rate period, product fee, interest rates, monthly payment, extra contributions, tax rate, and inflation into a comprehensive financial summary — complete with a year-by-year amortization table and a visual balance chart that shows exactly how your mortgage decreases over time.

In this complete guide, you will learn how a Mortgage Calculator UK works, what every input means in the context of the British mortgage market, how to interpret your results, and what practical strategies help you save money and pay off your mortgage faster. Whether you are a first-time buyer, a remortgager, or a buy-to-let investor, this guide and our free Mortgage Calculator UK give you the financial clarity to make smarter decisions.

What Is a Mortgage Calculator UK?

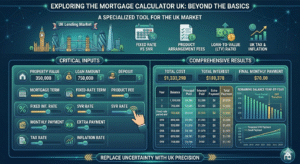

A Mortgage Calculator UK is a specialised online financial tool designed to calculate the complete cost structure of a British mortgage. Unlike generic loan calculators, a proper Mortgage Calculator UK accounts for the unique features of the UK lending market — including the distinction between fixed-rate periods and Standard Variable Rates, product arrangement fees, the Loan-to-Value ratio, and UK-specific tax and inflation considerations.

Our free Mortgage Calculator UK processes twelve critical inputs — property value, loan amount, deposit, full mortgage term, fixed-rate term, product fee, fixed interest rate, SVR rate, monthly payment, extra payment, tax rate, and inflation rate — and produces a complete result summary alongside a year-by-year amortization table and a bar chart showing your remaining balance for each year of the term.

The purpose of a Mortgage Calculator UK is to replace uncertainty with precision. The UK mortgage market is complex, with hundreds of lenders, thousands of products, and interest rate structures that change partway through the mortgage term. A Mortgage Calculator UK gives you the power to model exactly what your mortgage will cost — not just in year one at the attractive fixed rate, but across the entire term as rates potentially shift to the higher Standard Variab

How the UK Mortgage Market Works

Understanding the structure of the UK mortgage market is essential for using a Mortgage Calculator UK effectively. Here are the key features that make UK mortgages distinct from those in other countries:

Two-Phase Interest Structure: Most UK mortgages begin with an introductory period — typically 2, 3, or 5 years — at a fixed or tracker rate. After this period ends, the mortgage automatically moves to the lender’s Standard Variable Rate (SVR) unless you remortgage to a new deal. This two-phase structure is one of the most important features the Mortgage Calculator UK models.

Loan-to-Value (LTV): UK lenders price their products based on Loan-to-Value ratio. A larger deposit means a lower LTV, which typically qualifies for better rates. Most lenders offer their best rates at 60% LTV, with progressively higher rates at 75%, 85%, and 90% LTV.

Repayment vs. Interest-Only: UK borrowers can choose repayment mortgages (where each payment reduces the principal balance) or interest-only mortgages (where monthly payments cover only interest and the full principal remains at the end of the term). Our Mortgage Calculator UK models the repayment structure — the most common and recommended type for residential buyers.

Product Fees: UK mortgage products often come with arrangement fees, booking fees, or product fees that can range from £0 to £2,000 or more. A lower rate with a high product fee can cost more overall than a slightly higher rate with no fee — a comparison the Mortgage Calculator UK helps you make accurately.

Stamp Duty Land Tax (SDLT): Property purchases in England and Northern Ireland are subject to Stamp Duty — a tax based on the purchase price. Scotland has Land and Buildings Transaction Tax (LBTT) and Wales has Land Transaction Tax (LTT). These taxes significantly affect the total cash required to complete a purchase and should always be budgeted for alongside your deposit and fees.

Key Inputs Every Mortgage Calculator UK Requires

Accurate results from a Mortgage Calculator UK depend entirely on the accuracy of the inputs you provide. Here is a detailed explanation of each of the twelve fields:

Property Value (£): The agreed sale price or current market value of the property. This is the baseline figure from which your LTV, equity, and lending limits are calculated.

Loan Amount (£): The total amount you are borrowing from the lender — typically the property value minus your deposit. Most UK lenders cap residential loans at 4.5 times your annual income, though some lenders offer up to 5.5x for high earners.

Deposit (£): The cash you are contributing toward the purchase. In the UK, the minimum deposit for a residential mortgage is typically 5% of the property value, though you will access significantly better rates with a 10%, 15%, or 20% deposit. Enter your planned deposit into the Mortgage Calculator UK to see how it affects your loan amount and monthly payment.

Term (Years): The full repayment term of your mortgage. UK residential mortgages commonly run for 20 to 35 years. Longer terms lower monthly payments but increase total interest significantly — the Mortgage Calculator UK’s amortization table makes this trade-off immediately clear.

Fixed Term (Years): The number of years your initial fixed rate applies. After this period, the rate reverts to the SVR unless you remortgage. Common fixed periods in the UK are 2, 3, and 5 years. Entering your specific fixed term into the Mortgage Calculator UK ensures the interest calculation accurately reflects the two-rate structure.

Product Fee (£): The arrangement or product fee charged by the lender to set up the mortgage. This can typically be added to the loan (increasing your borrowing) or paid upfront. Always factor the product fee into your total cost calculation — the Mortgage Calculator UK includes it in the result summary.

Fixed Rate (%): The annual interest rate during your initial fixed period. This is the attractive rate advertised by lenders and represents the lower-cost phase of your mortgage.

SVR Rate (%): The Standard Variable Rate your lender will apply after your fixed period expires. UK SVRs are typically 2% to 4% higher than the initial fixed rate. The gap between your fixed rate and SVR is where most UK mortgage pain comes from, and the Mortgage Calculator UK models this transition clearly.

Monthly Payment (£): Your planned monthly mortgage payment. This can be the minimum required payment or a higher figure if you intend to overpay from the start.

Extra Payment (£): Any monthly overpayment above your contracted amount. UK mortgage lenders typically allow overpayments of up to 10% of the outstanding balance per year without an early repayment charge — a powerful tool for reducing your term and total interest.

Tax Rate (%): For buy-to-let investors and landlords, your income tax rate affects the net return on rental income. For owner-occupiers, this field can reflect the broader tax context of the investment.

Inflation (%): The current or expected inflation rate — relevant for understanding the real cost of your mortgage over time and the purchasing power of your future payments.

Understanding Fixed Rate vs. Standard Variable Rate (SVR)

One of the most critical distinctions in UK mortgage planning is the difference between the initial fixed rate and the Standard Variable Rate — and the Mortgage Calculator UK models both precisely.

Fixed Rate: During the fixed period (typically 2 to 5 years), your interest rate is locked in regardless of changes in the Bank of England base rate or lender decisions. This provides complete payment certainty and is the most popular mortgage type in the UK for this reason.

Standard Variable Rate (SVR): Once your fixed period ends, your mortgage automatically moves to your lender’s SVR — a rate set at the lender’s discretion that typically sits 3% to 5% above the Bank of England base rate. SVRs are not fixed and can change at any time. In practice, SVRs are almost always significantly higher than available market rates, which is why remortgaging at the end of your fixed term is nearly always financially advisable.

Why the SVR matters so much in your Mortgage Calculator UK analysis: If you have a 20-year mortgage with a 2-year fixed rate, you will spend 18 years on the SVR unless you actively remortgage. Over those 18 years, the higher SVR rate means paying thousands of pounds more in interest than necessary. The Mortgage Calculator UK’s amortization table shows your annual balance across both the fixed period and the SVR period, making the cost of inaction dramatically visible.

The smart strategy: Use the Mortgage Calculator UK to identify the point at which your fixed rate expires, note the projected balance at that point, and plan to remortgage to a new competitive deal before your lender transfers you to the SVR.

How Loan-to-Value Ratio Affects Your Mortgage

Your Loan-to-Value (LTV) ratio is one of the most important factors in UK mortgage pricing, and understanding it helps you use the Mortgage Calculator UK more strategically.

LTV = Loan Amount ÷ Property Value × 100

A property valued at £300,000 with a £250,000 loan has an LTV of 83.3%. The same property with a £200,000 loan has an LTV of 66.7%. Lower LTV means less risk for the lender and significantly better rates for the borrower.

UK mortgage pricing by LTV tier typically follows this pattern:

- 60% LTV and below: Best available rates, reserved for buyers with large deposits or significant equity

- 70% to 75% LTV: Good rates available from most high-street lenders

- 80% to 85% LTV: Moderate rates; fewer product options

- 90% LTV: Limited product choice; higher rates

- 95% LTV: Highest rates; typically requires government scheme or specialist lender

When using the Mortgage Calculator UK, experiment with different deposit amounts to see how moving from 85% LTV to 80% LTV (by saving an additional £15,000 on a £300,000 property) changes your available rate and therefore your total interest cost. The savings are often significant enough to justify delaying your purchase to save more.

Product Fees and Their Hidden Impact on Total Cost

Product fees are one of the most misunderstood costs in UK mortgage planning, and the Mortgage Calculator UK ensures they are never overlooked.

UK mortgage products often offer a choice between a lower rate with a higher fee or a slightly higher rate with no fee. Many borrowers instinctively choose the lowest advertised rate without considering whether the fee makes that choice more or less expensive overall.

A simple example: A 2-year fixed rate at 3.5% with a £999 product fee versus 3.7% with no fee. On a £250,000 loan over 2 years, the lower rate saves approximately £1,000 in interest — but the £999 fee means total savings of only £1. On a smaller loan, the no-fee option might actually be cheaper overall.

This is exactly why entering your product fee into the Mortgage Calculator UK matters. The result summary includes the product fee alongside all other cost components, allowing you to make a true total-cost comparison rather than a rate-only comparison.

If you add the product fee to your loan balance rather than paying it upfront, you also pay interest on the fee for the entire mortgage term — potentially turning a £999 fee into £1,500 or more in real cost over a 20-year term. The Mortgage Calculator UK helps you model both the upfront and financed versions of the fee to determine which approach costs less overall.

Extra Payments – The Fastest Route to Mortgage Freedom

One of the most powerful features of the Mortgage Calculator UK is its dedicated Extra Payment field, which allows you to model the financial impact of making voluntary overpayments on your mortgage.

UK mortgage regulations typically allow overpayments of up to 10% of the outstanding balance per year without triggering an Early Repayment Charge (ERC). Within this limit, every pound you overpay goes directly to reducing your principal balance — generating significant interest savings and shortening your mortgage term.

The compounding effect of overpayments is substantial. An extra £100 per month on a £250,000 mortgage at 3.5% over 20 years reduces the term by approximately 2.5 years and saves over £8,000 in interest. An extra £200 per month shortens the term by nearly 5 years.

The Mortgage Calculator UK’s amortization table shows the annual balance trajectory when you include extra payments — making the accelerated paydown clearly visible compared to the minimum payment schedule.

Practical overpayment strategies for UK homeowners:

- Regular monthly overpayments: Set a fixed extra amount each month — even £50 to £100 significantly impacts the long-term balance.

- Annual lump sum: Apply any year-end bonus, inheritance, or unexpected income directly to your mortgage principal up to the 10% annual limit.

- Increase payments at remortgage: Each time you remortgage, consider maintaining your current payment level (rather than reducing to the new minimum) to accelerate paydown.

Tax Rate and Inflation – The Wider Financial Picture

Our Mortgage Calculator UK includes two fields — Tax Rate and Inflation — that go beyond simple payment calculation to provide a more complete picture of your mortgage’s true financial context.

Tax Rate: For buy-to-let investors, UK income tax significantly affects net rental yield and overall return on investment. Rental income is taxed as regular income after deducting allowable expenses. Since the 2017 tax changes, mortgage interest relief for landlords has been replaced with a 20% basic rate tax credit — a change that significantly reduced the attractiveness of highly leveraged buy-to-let investment. Entering your personal tax rate into the Mortgage Calculator UK provides a more accurate net cost calculation for investment properties.

Inflation: Over a 20 or 25-year mortgage term, inflation dramatically affects the real value of your mortgage debt. While your mortgage balance is fixed in nominal terms, inflation erodes its real value over time — meaning a £250,000 mortgage today is effectively smaller in real purchasing power terms by the time you pay it off. Entering a realistic inflation assumption into the Mortgage Calculator UK adds an important perspective to your long-term financial planning.

For owner-occupiers, the tax and inflation fields help contextualize the opportunity cost of capital tied up in a deposit versus deployed in other investments — an increasingly important consideration as ISA rates and investment returns fluctuate.

How to Read Your Amortization Table

The amortization table is one of the most important outputs of the Mortgage Calculator UK, providing a year-by-year breakdown of your mortgage’s progress from origination to payoff.

The table contains four columns:

Year: Each row represents one year of the mortgage term, from year 1 to your selected term end.

Total Payment: The combined total of your monthly payment and any extra payment multiplied by 12 — your annual mortgage contribution.

Interest: The annual interest charged on your outstanding balance. During the fixed period, this is calculated at your fixed rate. After the fixed term expires, the SVR rate is applied — often revealing a noticeable jump in annual interest cost that motivates remortgaging.

Balance: Your remaining mortgage balance at the end of each year. This column is the clearest indicator of your equity-building progress. Early years show a slow balance reduction as interest consumes most of the payment. As the balance decreases and a greater proportion of each payment goes to principal, the balance drop accelerates in later years.

Key things to look for in your amortization table:

- Year your fixed rate expires: Note the interest figure in the transition year — it typically increases noticeably as the SVR kicks in.

- Break-even year for extra payments: Identify the year at which overpayments have reduced your balance below where it would be under the minimum payment schedule.

- Midpoint equity check: At the midpoint of your term, your balance should be roughly 50% to 60% of the original loan if you are making minimum payments — or lower if you are overpaying.

Understanding the Balance Chart

Alongside the amortization table, our Mortgage Calculator UK generates a colour-coded bar chart that visualises your remaining mortgage balance for each year of the term. This visual representation adds an intuitive layer to the numerical data in the table.

Each bar represents your outstanding balance at the end of that year. The multi-colour design helps distinguish individual years and makes it easy to identify at a glance how quickly your balance decreases.

What to look for in the balance chart:

Slow initial decline: The bars in the early years decrease slowly because most of the payment is covering interest. This is the interest-heavy phase of your mortgage — a normal feature of any amortizing loan structure.

Accelerating decline in later years: As your balance falls and a greater share of each payment reduces principal, the bars drop more steeply. This visual acceleration is satisfying evidence of your growing equity.

The SVR transition: If your fixed period ends midway through the term, a sharper or flatter decline in the bars post-transition year can visually indicate the impact of the rate change. A steeper decline confirms that the higher SVR payment (if larger than the fixed payment) is reducing your balance faster. A flatter or slower decline confirms the SVR’s higher interest cost is consuming a larger proportion of each payment.

First-Time Buyers in the UK – What You Need to Know

First-time buyers face a unique set of challenges and opportunities in the UK mortgage market, and the Mortgage Calculator UK helps them navigate both sides of that equation.

Stamp Duty Relief: First-time buyers in England pay no Stamp Duty on properties up to £425,000 (as of the current rules), and a reduced rate on the portion between £425,000 and £625,000. This relief significantly reduces the upfront cash required compared to subsequent purchases — a meaningful advantage to factor into your total cost calculation.

Help to Buy and Other Schemes: The UK government has offered various first-time buyer schemes including Help to Buy Equity Loans, Shared Ownership, and the Mortgage Guarantee Scheme. While Help to Buy ISA and equity loan have now closed to new applicants, Shared Ownership and the mortgage guarantee remain active options. The Mortgage Calculator UK can model any of these scenarios by adjusting the loan amount and deposit to reflect the scheme’s structure.

Higher LTV Products: First-time buyers with small deposits typically access 90% or 95% LTV products. Use the Mortgage Calculator UK to compare your monthly payment at 95% LTV versus what it would be at 90% LTV if you waited an extra 6 to 12 months to save a larger deposit. The difference in rate and monthly cost is often substantial.

Income Multiples and Affordability: UK lenders assess affordability using income multiples and stress-tested payments. As a first-time buyer, use the loan amount field in the Mortgage Calculator UK to model different borrowing levels against your income to find a sustainable mortgage size.

How to Use Our Mortgage Calculator UK Step-by-Step

Our free Mortgage Calculator UK is straightforward and produces comprehensive results instantly. Here is the complete process:

Step One – Enter Property Value: Input the agreed purchase price or current market value of the property in pounds.

Step Two – Enter Loan Amount and Deposit: Input the amount you are borrowing and your deposit separately. The Mortgage Calculator UK displays both in the result summary alongside your effective LTV.

Step Three – Set Your Mortgage Term: Enter the full repayment term in years. Common UK terms are 20, 25, and 30 years.

Step Four – Enter Fixed Term and Product Fee: Input the number of years at the fixed rate and the arrangement fee for your chosen product. These inputs ensure the two-phase interest calculation is accurate and the fee is reflected in your total cost.

Step Five – Enter Both Interest Rates: Input your fixed rate percentage and your lender’s current SVR. These two rates drive the year-by-year interest calculation in the amortization table, so accuracy here is critical.

Step Six – Enter Monthly and Extra Payments: Input your regular monthly payment amount and any additional monthly overpayment you plan to make.

Step Seven – Enter Tax Rate and Inflation: Input your income tax rate and an inflation estimate. For basic rate taxpayers, 20% is the standard input. For higher rate taxpayers, use 40%.

Step Eight – Click Calculate: Instantly view your complete result summary showing all 12 input values with currency symbols, the full amortization table, and the balance bar chart.

Step Nine – Experiment with Scenarios: Adjust your deposit amount, loan term, or extra payment to model different scenarios. The Mortgage Calculator UK lets you find the structure that best balances monthly affordability with long-term cost efficiency.

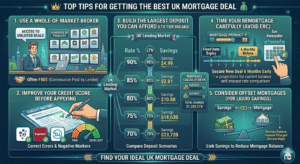

Tips to Get the Best Mortgage Deal in the UK

The UK mortgage market is highly competitive, and the right approach can save you thousands of pounds. Here are the most effective strategies:

Use a Whole-of-Market Broker: Independent mortgage brokers with access to the whole market can find products not available directly to consumers and compare hundreds of products simultaneously. Their advice is often free to you, paid by lender commission.

Improve Your Credit Score Before Applying: UK credit scores affect both your eligibility and the rates available to you. Check your report on Experian, Equifax, or TransUnion before applying, and address any errors or negative markers.

Build the Largest Deposit You Can Afford: Each LTV tier unlocks materially better rates. Use the Mortgage Calculator UK to quantify exactly how much a larger deposit saves you over the mortgage term — the answer often makes waiting a few extra months to save more an easy decision.

Time Your Remortgage Carefully: In the UK, you can typically secure a new mortgage deal up to 6 months before your fixed rate expires without paying an ERC. Set a calendar reminder 6 months before your fixed period ends and use the Mortgage Calculator UK to evaluate current market products against your projected balance at that point.Consider Offset Mortgages: An offset mortgage links your savings account to your mortgage balance, effectively reducing the interest charged while keeping your savings accessible. For borrowers with significant liquid savings, this can be a highly effective structure.

Common Mortgage Mistakes UK Buyers Make

Even experienced property buyers make costly errors. Here are the most common — and how the Mortgage Calculator UK helps you avoid them:

Reverting to SVR Without Remortgaging: This is the single most expensive mortgage mistake in the UK. Sitting on a lender’s SVR for years after a fixed period ends costs thousands of pounds in unnecessary interest. Always plan your remortgage using the Mortgage Calculator UK before your fixed term expires.

Focusing Only on the Monthly Payment: A lower monthly payment from a longer term or a no-fee product may look attractive but can cost significantly more overall. Always compare total cost using the Mortgage Calculator UK, not just the monthly figure.

Underestimating Total Purchase Costs: Stamp Duty, legal fees, survey costs, removal costs, and any immediate renovation work all add to the cash required to complete a purchase. Budget for these alongside your deposit.

Overstretching on Borrowing: Taking the maximum loan a lender will offer without stress-testing affordability against a rate increase is a common error. Use the SVR Rate field in the Mortgage Calculator UK to model your payment if rates rise significantly and confirm the payment remains affordable.

Not Overpaying During Fixed Period: Many borrowers believe they cannot overpay during the fixed rate period. In fact, most UK fixed-rate mortgages allow up to 10% overpayment per year without penalty. Use the Extra Payment field in the Mortgage Calculator UK to model how even modest overpayments shorten your term and save interest.

Frequently Asked Questions (FAQs)

What is a Mortgage Calculator UK? A Mortgage Calculator UK is a specialised financial tool that calculates UK mortgage costs including monthly payments, total interest, the two-phase fixed/SVR rate structure, product fees, overpayment impact, and a full amortization schedule with a balance chart.

Is the Mortgage Calculator UK free to use? Yes. Our Mortgage Calculator UK is completely free with no registration required. Enter your figures and receive instant, comprehensive results.

What is the Standard Variable Rate (SVR)? The SVR is the default interest rate your UK lender applies after your initial fixed or tracker deal expires. SVRs are typically 3% to 5% higher than competitive market rates and can change at the lender’s discretion. Always model the SVR impact in the Mortgage Calculator UK before selecting a mortgage product.

How much deposit do I need for a UK mortgage? The minimum deposit is typically 5% of the property value, though 10% to 15% opens up significantly more products and better rates. A 25% deposit or more typically unlocks the most competitive UK mortgage rates.

Can I overpay my UK mortgage? Most UK fixed-rate mortgages allow overpayments of up to 10% of the outstanding balance per year without an Early Repayment Charge. Use the Extra Payment field in the Mortgage Calculator UK to model the long-term impact of regular overpayments.

When should I remortgage in the UK? You should typically begin looking 3 to 6 months before your fixed rate expires to avoid reverting to the SVR. Use the Mortgage Calculator UK to project your balance at the remortgage date and compare current market products against the cost of staying on the SVR.

What is Loan-to-Value and why does it matter? LTV is your loan amount as a percentage of the property value. Lower LTV means more equity, less lender risk, and access to better mortgage rates. Adjust your deposit amount in the Mortgage Calculator UK to see how different LTV levels affect your mortgage cost.

Does the Mortgage Calculator UK account for Stamp Duty? The calculator focuses on mortgage costs rather than transaction taxes. Stamp Duty should be budgeted for separately using the government’s SDLT calculator and factored into your total cash required to purchase.

What is the difference between repayment and interest-only mortgages? A repayment mortgage reduces your balance with each payment, so you own the property outright at the end of the term. An interest-only mortgage keeps the balance constant and requires a separate repayment vehicle to clear the debt at term end. Our Mortgage Calculator UK models the repayment structure.

How accurate is the Mortgage Calculator UK? Our Mortgage Calculator UK provides highly accurate estimates based on the inputs you provide. For precise quotes, always consult a qualified mortgage adviser who can access lender systems and account for your individual circumstances.

Conclusion

The UK mortgage market is complex, competitive, and consequential — getting it right can save you tens of thousands of pounds over the life of your loan, while getting it wrong can mean years of unnecessarily high payments. A Mortgage Calculator UK is the tool that gives you the clarity to get it right.

Our free Mortgage Calculator UK processes all twelve key inputs of your mortgage scenario — property value, loan, deposit, term, fixed period, product fee, fixed rate, SVR, monthly payment, overpayments, tax, and inflation — into a complete financial picture: a detailed result summary, a year-by-year amortization table showing the transition from fixed rate to SVR, and a visual bar chart of your declining balance over time.

Whether you are buying your first home, remortgaging to a better deal, investing in buy-to-let, or simply reviewing your current mortgage’s true cost, the Mortgage Calculator UK gives you the data-driven foundation for every decision you make. It removes the guesswork, quantifies the impact of every variable, and empowers you to take control of the most significant financial commitment of your life.

Use our Mortgage Calculator UK today. Enter your numbers, explore your scenarios, and start making your most important financial decisions with complete confidence.