IRA Calculator

See how your investments can grow over time with our Mutual Fund Calculator

Table of Contents

- Introduction

- What Is an IRA Calculator?

- Why Every Retirement Saver Needs an IRA Calculator

- Key Inputs in an IRA Calculator Explained

- How to Use an IRA Calculator Step by Step

- Understanding Your IRA Calculator Results

- Traditional IRA vs. Roth IRA — How the IRA Calculator Helps You Choose

- How Inflation and Fees Impact Your IRA Growth

- Smart Retirement Strategies Using an IRA Calculator

- IRA Contribution Limits and How They Affect Your Planning

- Common Mistakes to Avoid When Using an IRA Calculator

- Frequently Asked Questions (FAQs)

- Conclusion

Introduction

Retirement planning is not something you can afford to leave to guesswork.

The decisions you make today — how much you contribute, when you start, which IRA account you choose, and how you manage fees and taxes — will determine the quality of your financial life for decades after you stop working.

That is exactly why an IRA Calculator is one of the most important financial tools available to any working adult.

An IRA Calculator takes your personal financial details and projects your exact retirement balance — year by year, from your current age all the way to your chosen retirement date.

It accounts for your current savings, annual contributions, expected investment return, tax rate, management fees, and inflation — all in one clear, precise calculation.

Without an IRA Calculator, you are planning blind. And planning blind with your retirement is a mistake you cannot afford to make.

This complete guide explains everything — every input, every result, every strategy — so you can use an IRA Calculator to build the most accurate and confident retirement plan possible.

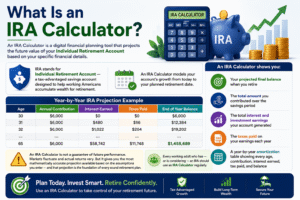

What Is an IRA Calculator?

An IRA Calculator is a digital financial planning tool that projects the future value of your Individual Retirement Account based on your specific financial details.

IRA stands for Individual Retirement Account — a tax-advantaged savings account designed to help working Americans accumulate wealth for retirement.

An IRA Calculator models your account’s growth from today to your planned retirement date. It shows you:

- Your projected final balance when you retire

- The total amount you contributed over the savings period

- The total interest and investment earnings your account generated

- The taxes paid on your earnings each year

- A year-by-year amortization table showing every age, contribution, interest earned, tax paid, and balance

An IRA Calculator is not a guarantee of future performance. Markets fluctuate and actual returns vary. But it gives you the most mathematically accurate projection available based on the assumptions you enter — and that projection is the foundation of every sound retirement plan.

Every working adult who has — or is considering — an IRA should use an IRA Calculator regularly.

Why Every Retirement Saver Needs an IRA Calculator

Most people significantly underestimate how much money they will need in retirement — and equally underestimate how much their current savings rate will actually produce.

Both of these miscalculations are dangerous. An IRA Calculator corrects both.

Here is exactly why an IRA Calculator is non-negotiable for serious retirement savers:

It shows you your real retirement number. Not a vague estimate. Not a rule of thumb. An IRA Calculator produces a specific projected balance based on your actual age, contributions, and return assumptions — so you know exactly what you are building toward.

It reveals the devastating impact of starting late. Run your numbers starting at age 25 in the IRA Calculator, then run them again starting at age 35. The difference in final balance will shock you. Compound growth rewards early starters with exponentially larger outcomes.

It quantifies the cost of fees and inflation. A 0.5% annual fee and 2% inflation together reduce your effective return significantly. An IRA Calculator models these costs annually so you see their compounding impact over a 30 or 40-year savings period — not just their seemingly small annual percentage.

It helps you set a realistic contribution target. Rather than guessing how much to save, use the IRA Calculator to work backward — enter your retirement goal and your current balance, and the calculator shows you exactly what annual contribution is required to reach it.

It removes anxiety by replacing uncertainty with clarity. One of the biggest sources of financial stress is not knowing whether you are on track. An IRA Calculator answers that question with precision — either confirming you are on course or showing you exactly what adjustments to make.

Key Inputs in an IRA Calculator Explained

Entering accurate inputs is the foundation of accurate results. Here is a complete breakdown of every field in the IRA Calculator:

Current Age

Your age today — the starting point of the projection.

The younger you are, the more powerful compound growth becomes. A 25-year-old who starts contributing $6,000 per year will retire with dramatically more wealth than a 35-year-old making identical contributions — purely because of the extra decade of compounding.

Enter your actual current age, not a rounded number.

Retirement Age

The age at which you plan to stop working and begin living on your retirement savings.

Most Americans plan to retire between ages 62 and 67. The difference between retiring at 60 and 67 is not just 7 fewer years of contributions — it is 7 fewer years of compound growth on your entire accumulated balance.

Use the IRA Calculator to compare different retirement ages and see the exact financial impact of each option.

Current Balance ($)

The amount currently sitting in your IRA account.

Even a small existing balance is enormously valuable — it earns compound returns for every remaining year until retirement. A $5,000 balance today, growing at 7% for 35 years, becomes approximately $53,000 without adding another dollar.

Enter your actual current IRA balance — check your account statement for the most recent figure.

Annual Contribution ($)

The amount you plan to contribute to your IRA each year going forward.

Annual contributions are the most controllable driver of your retirement outcome. Even modest increases — from $4,000 to $6,000 per year — produce massive differences in final balance over a 30-year savings horizon.

The IRS sets annual contribution limits for IRAs. In 2024, the limit is $7,000 per year ($8,000 if you are age 50 or older). Enter the actual amount you plan to contribute — never assume you will always hit the maximum.

Return Rate (%)

Your expected average annual investment return on the IRA assets.

For a diversified stock-heavy IRA portfolio, 6% to 8% per year is a commonly used long-term assumption. For more conservative portfolios with significant bond allocation, 4% to 6% may be more appropriate.

The IRA Calculator applies this return rate annually, compounding it forward across every year of your savings period.

Tax Rate (%)

Your expected annual marginal tax rate on investment earnings within the account.

For a Traditional IRA, earnings grow tax-deferred — meaning no tax is paid while the money is in the account, but withdrawals in retirement are taxed as ordinary income.

For a Roth IRA, contributions are made with after-tax dollars — but all growth and qualified withdrawals are completely tax-free.

Enter your current or expected tax rate to model the annual tax impact. Use 0% if modeling a Roth IRA where growth is tax-free.

Fees (%)

The annual management fees, fund expense ratios, and account administration costs — expressed as a percentage of your account balance.

This is the most underestimated cost in IRA planning. A 0.5% annual fee on a $200,000 balance costs $1,000 per year — and that $1,000 never compounds for the remaining years. Over 30 years, total fee costs can represent tens of thousands of lost retirement dollars.

Enter the actual combined expense ratio and account fee percentage from your IRA provider.

Inflation (%)

The annual inflation rate — used to model the real purchasing power erosion of your projected retirement balance.

Inflation is the silent retirement thief. A $1,000,000 IRA balance in 30 years will not buy what $1,000,000 buys today. At 2% annual inflation, its purchasing power will be worth approximately $550,000 in today’s dollars.

The IRA Calculator deducts the inflation rate from your real return to show you growth that accounts for the actual purchasing power of your future money.

How to Use an IRA Calculator Step by Step

Follow these steps for the most accurate and actionable results:

Step 1 — Gather your current IRA account information. Log in to your IRA account and note your current balance, annual contribution amount, current investment options and their expense ratios, and account management fees. Have these exact figures ready before opening the IRA Calculator.

Step 2 — Enter your current age and target retirement age. Be honest about your retirement goal. If you want to retire at 62, enter 62 — not 67. The IRA Calculator shows you the real cost of your chosen retirement timeline, including what you must save to make it realistic.

Step 3 — Enter your current IRA balance. Use your actual, verified account balance from your most recent statement. This is the starting point for all compound growth projections in the IRA Calculator.

Step 4 — Enter your planned annual contribution. Enter the amount you will realistically contribute each year — not the maximum limit unless you are certain you can sustain it. Consistent, realistic contributions over time outperform ambitious targets that get abandoned after two years.

Step 5 — Set your return rate conservatively. Use 6% to 7% for a balanced retirement portfolio. Use 7% to 8% for an equity-heavy portfolio with a long time horizon. Never inflate your return assumption — an IRA Calculator based on unrealistic returns produces false comfort, not genuine financial security.

Step 6 — Enter your tax rate, fees, and inflation. Enter your current or expected marginal tax rate for the account type you are using. Enter the actual management fees from your IRA provider. Use 2% to 3% for the inflation rate. These three fields together reveal the true real-world growth of your account — not just the nominal growth before costs.

Step 7 — Click Calculate and review every result. The IRA Calculator displays your final balance, total contributions, total interest, total taxes paid, and average annual interest. It also generates a year-by-year amortization table. Study every row of the table — it shows you exactly how your balance builds at every age from now until retirement.

Step 8 — Run multiple scenarios. Increase your annual contribution by $1,000 and recalculate. Reduce your fees by 0.25% and recalculate. Delay retirement by 3 years and recalculate. Running multiple scenarios through the IRA Calculator reveals exactly which changes have the greatest impact on your final retirement balance — and which levers you should pull first.

Understanding Your IRA Calculator Results

Every number in the IRA Calculator output tells an important part of your retirement story.

Final Balance is the projected total value of your IRA account on your chosen retirement date. This is your retirement number — the amount you will have available to fund your post-work life. Compare this against your estimated annual retirement expenses multiplied by your expected years in retirement to see if your plan is sufficient.

Total Contributed is the sum of every annual contribution you will make from today until retirement. This is the total of your own money deposited — your actual cost of building the account. Subtract this from your final balance and you see the total growth generated by your investments.

Total Interest is the cumulative investment earnings your IRA generated over the full savings period — the power of compound growth made visible in a single number. This figure dramatically illustrates why starting early and staying invested matters so much — the interest number grows exponentially with time.

Total Tax Paid shows the cumulative tax deducted from investment earnings throughout the savings period. For Traditional IRA modeling with a non-zero tax rate, this figure shows you the annual cost of deferred-tax growth. For Roth IRA modeling (tax rate = 0%), this number will be zero — visually confirming the Roth’s tax-free advantage.

Years to Grow is simply the difference between your retirement age and your current age — the number of years compound growth has to work. Every additional year of growth dramatically increases your final balance, which is why the IRA Calculator so powerfully illustrates the cost of retiring early or the reward of delaying retirement by even a few years.

Average Interest Per Year is your total interest divided by the number of years — giving you an intuitive sense of how much your account earns on average annually. This number grows significantly over time as your balance increases, demonstrating the acceleration of compound growth in later years.

Year-by-Year Amortization Table shows your age, contribution, interest earned, tax paid, and ending balance for every single year from now to retirement. This table is the most detailed and useful output the IRA Calculator produces. Scroll through it and find the age at which your annual interest earned exceeds your annual contribution — that crossover point is when your money is truly working harder than you are.

Traditional IRA vs. Roth IRA — How the IRA Calculator Helps You Choose

One of the most important retirement decisions you will make is choosing between a Traditional IRA and a Roth IRA.

The IRA Calculator helps you model both options and compare them directly.

Traditional IRA:

- Contributions may be tax-deductible in the year made

- Investment growth is tax-deferred — no tax while money stays in the account

- Withdrawals in retirement are taxed as ordinary income

- Best for people who expect to be in a lower tax bracket in retirement than they are today

To model a Traditional IRA in the IRA Calculator: enter your current tax rate in the Tax Rate field. The calculator will deduct taxes from your annual investment earnings, reflecting the ongoing tax treatment of a taxable account or the future tax liability of Traditional IRA withdrawals.

Roth IRA:

- Contributions are made with after-tax dollars — no deduction today

- Investment growth is completely tax-free

- Qualified withdrawals in retirement are entirely tax-free

- Best for people who expect to be in a higher tax bracket in retirement or who want tax-free income flexibility in retirement

To model a Roth IRA in the IRA Calculator: enter 0% in the Tax Rate field. The resulting final balance reflects tax-free compound growth — showing you the genuine long-term advantage of Roth accounts for younger investors with long growth horizons.

Run the IRA Calculator with your actual tax rate, then run it again with 0% to see the precise dollar difference between Traditional and Roth IRA outcomes over your specific savings period. This comparison is one of the most valuable analyses the IRA Calculator can produce for your retirement planning.

How Inflation and Fees Impact Your IRA Growth

Inflation and fees are the two silent forces that erode your retirement wealth year after year — and most people dramatically underestimate their combined impact.

The IRA Calculator models both forces precisely, showing you their compounding negative effect across your entire savings period.

Inflation reduces the purchasing power of your retirement balance. If your IRA Calculator projects a $900,000 final balance in 35 years, that $900,000 will not buy what $900,000 buys today.

At 2% annual inflation over 35 years, your real purchasing power will be approximately $450,000 in today’s dollars — less than half the nominal balance. The IRA Calculator incorporates inflation into your effective return rate to show you real, inflation-adjusted growth rather than misleading nominal growth.

Fees are equally damaging — and uniquely so because they compound negatively.

Consider this example:

- Portfolio: $200,000 growing at 7% for 25 years

- With 0.10% annual fees (index fund): Final balance ≈ $1,060,000

- With 1.00% annual fees (actively managed fund): Final balance ≈ $860,000

That is a $200,000 difference — entirely from fees. And the IRA Calculator reveals this with precise numbers when you change only the fees field.

The strategic lesson from the IRA Calculator is clear:

- Choose low-cost index funds inside your IRA to minimize the fee drag

- Understand that every 0.25% reduction in annual fees translates to tens of thousands of dollars more in your retirement balance

- Never overlook the fees field when entering your data — it is as important as your return rate

Smart Retirement Strategies Using an IRA Calculator

Once you understand how to read your IRA Calculator results, apply these proven strategies to optimize your retirement outcome:

Start as early as possible — even with small amounts. Run your IRA Calculator starting at age 25 with a $2,000 annual contribution versus starting at age 35 with a $4,000 annual contribution. In most scenarios, the earlier starter wins — because compound growth on a longer timeline outweighs a higher contribution starting later. Time is the most powerful variable in the IRA Calculator.

Increase contributions by the amount of every raise. Every time your income increases, direct at least half of the raise toward your IRA contribution. Run the IRA Calculator after each increase to see how even a $500 or $1,000 annual contribution increase translates to tens of thousands more at retirement.

Minimize fees relentlessly. Compare your current IRA fee structure against low-cost index fund alternatives. Run both through the IRA Calculator with identical return rates and holding periods. The fee comparison alone will show you thousands or tens of thousands of dollars in difference — often more than enough motivation to switch to a lower-cost provider or fund selection.

Model the impact of delay — then act accordingly. Every year you wait to maximize your IRA contribution is a year of compound growth you can never recover. Use the IRA Calculator to calculate exactly what one year of delay costs you in final balance — the result is almost always more than enough to motivate immediate action.

Take advantage of catch-up contributions after age 50. The IRS allows individuals aged 50 and older to contribute an additional $1,000 per year above the standard limit — $8,000 total in 2024. Enter this higher contribution amount into the IRA Calculator to model how catch-up contributions during your final working years can meaningfully improve your retirement balance.

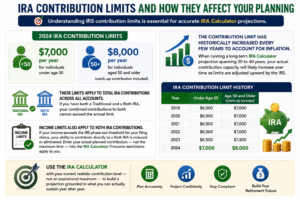

IRA Contribution Limits and How They Affect Your Planning

Understanding IRS contribution limits is essential for accurate IRA Calculator projections.

For 2024, the IRA contribution limits are:

- $7,000 per year for individuals under age 50

- $8,000 per year for individuals aged 50 and older (catch-up contribution included)

These limits apply to total IRA contributions across all accounts. If you have both a Traditional and a Roth IRA, your combined contributions to both cannot exceed the annual limit.

Income limits also apply to Roth IRA contributions. If your income exceeds the IRS phase-out threshold for your filing status, your ability to contribute directly to a Roth IRA is reduced or eliminated. Enter your actual planned contribution — not the maximum limit — into the IRA Calculator if income restrictions apply to you.

The contribution limit has historically increased every few years to account for inflation. When running a long-term IRA Calculator projection spanning 30 to 40 years, your actual contribution capacity will likely increase over time as limits are adjusted upward by the IRS.

Use the IRA Calculator with your current realistic contribution level — not an aspirational maximum — to build a projection grounded in what you can actually sustain year after year.

Common Mistakes to Avoid When Using an IRA Calculator

Avoid these frequent errors to ensure your IRA Calculator results are reliable and actionable:

Mistake 1 — Using an overly optimistic return rate. Entering 12% or 15% as your return rate makes the final balance look exciting but creates false security. Use 6% to 8% for a diversified stock portfolio — conservative enough to account for down years while reflecting realistic long-term averages. An honest projection beats a flattering one every time.

Mistake 2 — Ignoring fees entirely. Leaving the fees field at 0% is one of the most common and costly errors. Almost every IRA has some level of fees — account management charges, fund expense ratios, or advisor fees. Even 0.25% matters significantly over 30 years. Always enter your actual fee percentage.

Mistake 3 — Setting inflation to zero. A 0% inflation assumption means you believe money in 30 years will buy exactly what it buys today. That has never been true in modern economic history. Use 2% to 3% — the historical long-term average — to model the real purchasing power of your retirement savings.

Mistake 4 — Not reviewing the amortization table. Most users read the summary and stop. The year-by-year amortization table is the most valuable output the IRA Calculator produces. It shows you the age at which your interest earnings overtake your contributions, the years where inflation creates the most drag, and the compounding acceleration in the final decade before retirement.

Mistake 5 — Running the IRA Calculator only once. Your financial situation changes every year. Income grows, expenses shift, markets change, and IRS contribution limits update. Run the IRA Calculator at least once per year — ideally at the start of each tax year — to keep your retirement projection current and your savings strategy properly calibrated.

Frequently Asked Questions (FAQs)

Q1: What does an IRA Calculator calculate?

An IRA Calculator projects your IRA account’s growth from your current age to your planned retirement age. It shows your final balance, total contributions made, total investment interest earned, total taxes paid, and a year-by-year amortization table of every contribution, interest payment, tax deduction, and ending balance across your entire savings horizon.

Q2: What is the difference between a Traditional IRA and a Roth IRA in the IRA Calculator?

In the IRA Calculator, model a Traditional IRA by entering your actual tax rate — reflecting the annual tax on investment earnings or the future tax on withdrawals. Model a Roth IRA by entering 0% as the tax rate — reflecting completely tax-free investment growth and qualified withdrawals. Run both scenarios and compare the final balances to see which account type delivers the better outcome for your specific tax situation and timeline.

Q3: What return rate should I use in the IRA Calculator?

For a diversified, stock-heavy IRA portfolio with a long time horizon, 6% to 8% per year is a widely accepted conservative assumption. For a more balanced portfolio with significant bond exposure, use 4% to 6%. Never use rates above 8% to 9% for long-term projections — they create unrealistic expectations that can lead to dangerously underfunded retirement plans.

Q4: How do fees affect my IRA Calculator results?

Fees reduce your effective return rate and compound negatively over time. Every dollar paid in annual fees is a dollar removed from your compounding balance permanently. A difference of just 0.75% in annual fees on a $300,000 portfolio held for 20 more years can represent over $60,000 in lost retirement wealth. Always enter your actual fee percentage into the IRA Calculator and then compare the result against a 0.10% fee scenario to quantify the specific cost of your current fee structure.

Q5: How much should I contribute annually according to the IRA Calculator?

The IRA Calculator can answer this question in reverse — enter your target retirement balance, your current age, your current balance, and your expected return rate, and adjust your annual contribution figure until the projected final balance matches your goal. This reverse-planning approach turns the IRA Calculator into a powerful contribution targeting tool. For most Americans, maximizing contributions up to the IRS annual limit is the most straightforward path to adequate retirement savings.

Q6: At what age should I start using an IRA Calculator?

As early as possible — ideally the moment you begin your first full-time job. The most powerful thing the IRA Calculator can show a young person is the difference between starting at 22 versus 32. The 10-year difference in compound growth is so large that it permanently and irreversibly changes lifetime retirement outcomes. There is no minimum age for benefit — every year of additional calculation and planning improves your financial outcome.

Q7: How does inflation affect my IRA Calculator results?

Inflation reduces the real purchasing power of your projected final balance. The IRA Calculator deducts your entered inflation rate from your effective return — so if you enter 7% return and 2% inflation, your real growth rate is approximately 5%. This means your final balance projection already accounts for inflation’s erosion of purchasing power, giving you a more honest picture of your retirement wealth in today’s dollars rather than inflated future nominal dollars.

Q8: Can I use the IRA Calculator to compare starting at different ages?

Yes — and this is one of the most eye-opening comparisons the IRA Calculator can produce. Run the calculation with your current age, then run it again with an age 5 years younger and 5 years older, keeping all other inputs identical. The difference in final balance across these three scenarios powerfully illustrates the exponential reward of early starting and the steep compounding cost of delay — one of the most motivating outputs any retirement tool can generate.

Q9: Should I use the IRA Calculator every year?

Absolutely — at a minimum once per year, and ideally every time your financial situation changes. Annual reviews catch problems early. When your income increases, update your contribution. When you switch IRA providers and reduce your fees, update that field. When IRS contribution limits increase, update your annual contribution ceiling. The IRA Calculator is most valuable as a recurring annual planning tool, not a one-time calculation you make and file away.

Conclusion

The IRA is one of the most powerful retirement savings tools ever created — and the IRA Calculator is the key that unlocks its full potential.

Without running your numbers, you are guessing at one of the most important financial outcomes of your life. With an IRA Calculator, you have precision — and precision is the foundation of confidence.

You can see exactly how much you will have at retirement. You can see the real cost of fees and inflation. You can model the Roth versus Traditional decision with actual numbers rather than general advice. And you can identify the specific actions — more contributions, lower fees, a longer holding period — that will have the greatest impact on your final balance.

The IRA Calculator removes uncertainty and replaces it with clarity.

Whether you are 25 years old just opening your first IRA, or 55 years old accelerating your catch-up contributions, the IRA Calculator gives you the roadmap you need — personalized to your actual situation, not a generic guideline.

Start today. Enter your numbers. Know your retirement outcome. And adjust your plan accordingly.

Your retirement deserves the clarity that only an IRA Calculator can provide.