Mutual Fund Calculator

Estimate your CD earnings and future savings growth with our CD Calculator

Table of Contents

- Introduction

- What Is a Mutual Fund Calculator?

- Why You Need a Mutual Fund Calculator Before Investing

- Key Inputs in a Mutual Fund Calculator Explained

- How to Use a Mutual Fund Calculator Step by Step

- Understanding Your Mutual Fund Calculator Results

- How Fees and Charges Affect Your Returns

- Smart Investment Strategies Using a Mutual Fund Calculator

- Types of Mutual Funds You Can Analyze With a Mutual Fund Calculator

- Common Mistakes to Avoid When Using a Mutual Fund Calculator

- Mutual Fund Calculator vs. Other Investment Calculators

- Frequently Asked Questions (FAQs)

- Conclusion

Introduction

Investing in mutual funds is one of the most popular and accessible ways to grow wealth over time.

Whether you are a beginner investor or a seasoned financial planner, understanding exactly how your money will grow — and how much of it you will actually keep after fees — is critical before committing a single dollar.

That is exactly where a Mutual Fund Calculator becomes your most powerful planning tool.

A Mutual Fund Calculator takes your investment details and projects your future returns with precision. It accounts for your initial investment, regular contributions, expected rate of return, holding period, sales charges, deferred fees, and operating expenses — all in one place.

Without using a Mutual Fund Calculator, most investors are simply guessing. And guessing with your money is expensive.

This complete guide covers everything you need to know — from understanding every input field to reading every result, and from avoiding fee traps to comparing investment strategies confidently.

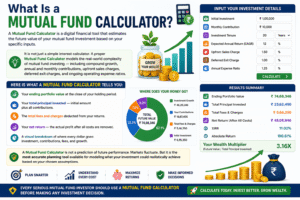

What Is a Mutual Fund Calculator?

A Mutual Fund Calculator is a digital financial tool that estimates the future value of your mutual fund investment based on your specific inputs.

It is not just a simple interest calculator. A proper Mutual Fund Calculator models the real-world complexity of mutual fund investing — including compound growth, annual and monthly contributions, upfront sales charges, deferred exit charges, and ongoing operating expense ratios.

Here is what a Mutual Fund Calculator tells you:

- Your ending portfolio value at the close of your holding period

- Your total principal invested — initial amount plus all contributions

- The total fees and charges deducted from your returns

- Your net return — the actual profit after all costs are removed

- A visual breakdown of where every dollar goes: investment, contributions, fees, and growth

A Mutual Fund Calculator is not a prediction of future performance. Markets fluctuate. But it is the most accurate planning tool available for modeling what your investment could realistically achieve based on your chosen assumptions.

Every serious mutual fund investor should use a Mutual Fund Calculator before making any investment decision.

Why You Need a Mutual Fund Calculator Before Investing

Many investors focus only on a fund’s advertised rate of return — and ignore the fees that silently erode their wealth.

A fund advertising 8% annual returns sounds attractive. But after a 2% sales charge, 0.5% annual operating expense ratio, and potential deferred charges, your real net return can be significantly lower.

A Mutual Fund Calculator reveals this truth with exact numbers.

Here is why using a Mutual Fund Calculator before investing is non-negotiable:

It shows your real net return after all costs. Not the gross advertised return — the actual dollars you take home after every fee has been deducted. This is the only number that matters.

It quantifies the true cost of fees over time. A 1% expense ratio sounds small. But on a $100,000 portfolio held for 20 years, it can cost you over $30,000 in lost compounding growth. A Mutual Fund Calculator makes this visible and undeniable.

It helps you compare funds side by side. Enter the same investment amount, holding period, and return rate — but change the fee structures. The Mutual Fund Calculator instantly shows which fund delivers better real-world results after costs.

It motivates disciplined, consistent contributions. When you see how monthly contributions compound into substantial wealth over time, the Mutual Fund Calculator provides powerful motivation to stay invested and contribute regularly.

It removes emotional guesswork from financial decisions. Data beats instinct every time. And the Mutual Fund Calculator gives you the data you need.

Key Inputs in a Mutual Fund Calculator Explained

Understanding every input field is essential for getting accurate, useful results.

Here is a complete breakdown of every field in the Mutual Fund Calculator and exactly what each one means:

Initial Investment ($)

This is the lump-sum amount you invest on day one.

Your initial investment is the most powerful driver of long-term compound growth — because it earns returns for the entire holding period, not just part of it.

Even a modest initial investment of $5,000 or $10,000, held for 15 to 20 years at a reasonable return rate, grows into a substantial sum. Enter your actual planned investment — not a wishful number.

Annual Contribution ($)

The additional amount you invest every year throughout the holding period.

Annual contributions dramatically accelerate wealth building. Each annual contribution has its own compound growth runway — it grows from the year it is made until the end of your holding period.

If your fund does not allow annual lump-sum additions, use the monthly contribution field instead.

Monthly Contribution ($)

The amount you add to your mutual fund investment every single month.

Monthly contributions are the backbone of systematic investment planning. Even $200 or $500 per month, consistently invested over 10 to 20 years, builds extraordinary wealth through compound growth.

The Mutual Fund Calculator compounds both annual and monthly contributions forward to the end of your holding period automatically.

Rate of Return (%)

Your expected average annual rate of return on the mutual fund investment.

This is a projected figure — not a guarantee. For equity mutual funds, historical long-term average returns have ranged from 7% to 12% annually depending on the fund category and market conditions. For bond funds, typical returns range from 3% to 6%.

Use a conservative estimate — 6% to 8% for equity funds — to avoid overestimating your projected wealth.

The Mutual Fund Calculator automatically deducts the operating expense ratio from this rate to show your net growth rate.

Holding Length (Years)

How many years you plan to keep your money invested in the mutual fund.

Holding period is one of the most powerful variables in the entire Mutual Fund Calculator — because compound growth is exponential, not linear.

The difference between holding an investment for 10 years versus 20 years is not double the growth — it is often four to six times the growth, due to compounding.

Longer holding periods reward patient investors disproportionately.

Sales Charge (%)

The upfront load or sales charge deducted when you first purchase the mutual fund.

Front-end loads typically range from 1% to 5.75% and are taken out of your initial investment immediately. A 3% sales charge on a $20,000 investment means only $19,400 actually enters the fund on day one.

Some mutual funds are “no-load” funds with 0% sales charge. The Mutual Fund Calculator allows you to enter 0% to model no-load funds and compare them against loaded alternatives.

Deferred Charge (%)

Also called a back-end load or contingent deferred sales charge (CDSC).

This fee is charged when you sell or redeem your mutual fund shares — typically calculated as a percentage of the ending value at the time of sale.

Deferred charges often decrease the longer you hold the fund. Many funds waive the deferred charge entirely if you hold for 5 to 7 years.

The Mutual Fund Calculator applies this charge to your ending value at maturity to show its exact dollar impact.

Operating Expense Ratio (%)

The annual fee charged by the mutual fund company to manage the fund.

This is the most consistently underestimated cost in mutual fund investing. The expense ratio is deducted automatically from fund returns each year — you never see a separate bill for it, which makes it easy to ignore.

Typical expense ratios range from 0.03% for passive index funds to 1.5% or more for actively managed funds.

The Mutual Fund Calculator deducts the operating expense ratio from your rate of return annually, showing you the true compounding impact of this recurring cost over your full holding period.

How to Use a Mutual Fund Calculator Step by Step

Follow these steps for the most accurate and useful results:

Step 1 — Identify the specific fund you are evaluating. Before entering any numbers, research the mutual fund’s current expense ratio, sales charge structure, and historical performance. Use the fund’s official prospectus or a financial data site for accurate figures.

Step 2 — Enter your initial investment. Type the exact dollar amount you plan to invest upfront. Use your actual planned commitment — accuracy here drives accuracy everywhere else in the Mutual Fund Calculator.

Step 3 — Enter your annual and monthly contributions. Decide whether you will add money annually, monthly, or both. Enter your realistic planned contribution amounts. Do not enter aspirational numbers you cannot sustain — disciplined, consistent contributions beat optimistic projections every time.

Step 4 — Enter your expected rate of return. Use a conservative, research-based estimate. For a diversified equity fund, 6% to 8% is a reasonable assumption for long-term planning. For bond funds, use 3% to 5%.

Step 5 — Set your holding period. Enter the number of years you plan to stay invested. Be realistic — the Mutual Fund Calculator rewards longer holding periods mathematically, so only enter what you can genuinely commit to.

Step 6 — Enter all fee information accurately. Enter the sales charge, deferred charge, and operating expense ratio from the fund’s official documentation. Never estimate fees — always use the actual figures from the fund prospectus.

Step 7 — Click Calculate and review all results. The Mutual Fund Calculator will display your ending value, total principal, total contributions, total fees, and net return. Study every number — not just the ending value.

Step 8 — Run comparison scenarios. Change one variable at a time — lower the expense ratio, remove the sales charge, increase the holding period, or add monthly contributions. Running multiple scenarios is where the Mutual Fund Calculator delivers its greatest value, revealing exactly how each variable affects your real net outcome.

Understanding Your Mutual Fund Calculator Results

Each result produced by the Mutual Fund Calculator tells an important part of your investment story.

Ending Value is the total projected worth of your mutual fund at the end of your holding period, before deducting deferred charges. This is the gross accumulated value of your investment — your starting capital plus all contributions plus all compounding growth minus ongoing operating expenses.

Total Principal is the sum of your initial investment plus every annual and monthly contribution made throughout the holding period. This is the total amount of your own money that entered the fund — your actual cost basis.

Total Contributions is the total of all annual and monthly contributions made after the initial investment. This separates your ongoing saving discipline from your starting capital.

Net Return is your actual profit — the amount by which your ending value exceeds your total principal, after all charges and fees have been subtracted. This is the truest measure of how well your mutual fund investment performed for you personally.

Sales Charge shows the exact dollar amount deducted upfront from your initial investment as the front-end load. This money never enters the fund and never earns any returns — making it one of the most expensive fees on a compounding basis.

Operating Expenses shows the total cumulative cost of the fund’s annual expense ratio across your full holding period. This figure is frequently shocking — because while 0.5% per year sounds trivial, it compounds into a significant dollar amount over 10 to 20 years.

Total Charges and Fees combines all costs — sales charges, deferred charges, and operating expenses — into one comprehensive number. Compare this figure across different fund options to understand which fund is truly the most cost-efficient choice for your investment goals.

How Fees and Charges Affect Your Returns

Fees are the silent destroyers of mutual fund wealth — and a Mutual Fund Calculator makes their impact impossible to ignore.

Here is a real-world example that illustrates the true cost of fees:

Imagine you invest $20,000 for 20 years at an 8% gross annual return.

- Fund A: 0% sales charge, 0.10% expense ratio (index fund)

- Fund B: 3% sales charge, 1.20% expense ratio (actively managed fund)

Without using a Mutual Fund Calculator, both funds might look similar — after all, you are getting the same market exposure at the same gross return.

But running both through a Mutual Fund Calculator reveals the truth:

- Fund A produces a net ending value of approximately $93,000

- Fund B produces a net ending value of approximately $67,000

That is a $26,000 difference — entirely from fees. The Mutual Fund Calculator makes this calculation in seconds.

The three types of fees to watch most closely are:

Front-end sales loads — deducted immediately, meaning your principal starts smaller and every dollar of missing principal costs you compound growth for the entire holding period.

Operating expense ratios — deducted silently every year from your fund’s return. On a 20-year investment, even a 1% annual difference in expense ratios can cost you 20% or more of your total accumulated wealth.

Deferred charges (back-end loads) — applied to your ending value when you sell, which can be especially painful if your portfolio has grown substantially.

Always use the Mutual Fund Calculator to compare the net after-fee results of every fund you evaluate — never make a fund selection based on gross advertised returns alone.

Smart Investment Strategies Using a Mutual Fund Calculator

Once you understand how to read the Mutual Fund Calculator results, use these proven strategies to optimize your outcomes:

Prioritize low-cost funds. The single most controllable variable in your mutual fund returns is cost. Run multiple scenarios in the Mutual Fund Calculator using different expense ratios — 0.10%, 0.50%, and 1.20% — with the same return rate and holding period. The results will demonstrate clearly why minimizing fees is the highest-impact decision most investors can make.

Model the power of consistent monthly contributions. Enter your current monthly contribution amount into the Mutual Fund Calculator, then increase it by $100 and run the calculation again. The difference in ending value over a 15 or 20-year holding period will motivate you to find ways to increase your contributions systematically.

Choose no-load funds whenever possible. Run your planned investment through the Mutual Fund Calculator twice — once with your actual sales charge and once with 0% sales charge. The difference shows you exactly how much you are paying for the privilege of buying that specific fund through a broker. In many cases, an equivalent no-load fund is available at zero upfront cost.

Maximize your holding period. Use the Mutual Fund Calculator to compare 10-year, 15-year, and 20-year holding periods for the same investment. The exponential difference in ending value across these periods provides compelling mathematical evidence for staying invested longer rather than timing the market.

Reinvest all dividends. While the Mutual Fund Calculator models return-based growth, all dividends and capital gains distributions should be reinvested in additional shares rather than taken as cash. This keeps your full invested capital working continuously toward compound growth throughout your entire holding period.

Types of Mutual Funds You Can Analyze With a Mutual Fund Calculator

The Mutual Fund Calculator is flexible enough to model virtually any type of mutual fund investment. Here is how to apply it across the most common fund categories:

Equity Mutual Funds invest primarily in stocks and offer the highest long-term growth potential. Use a rate of return of 7% to 12% for long-term equity fund modeling in the Mutual Fund Calculator. These funds typically carry higher operating expense ratios for actively managed options — and lower ratios for passive index versions.

Bond Mutual Funds invest in government or corporate debt instruments and provide more stable but lower returns. Use 3% to 6% as your rate of return for bond fund modeling. These funds typically have lower expense ratios and often no sales charges, making them cost-efficient income-oriented options to model in the Mutual Fund Calculator.

Balanced Mutual Funds combine stocks and bonds in a single portfolio — typically 60% equity and 40% fixed income. Use 5% to 8% as a reasonable return assumption. The Mutual Fund Calculator handles these funds identically to pure equity or bond funds — the return assumption is simply more moderate to reflect the blended composition.

Index Funds track a market index like the S&P 500 and are characterized by extremely low expense ratios — often between 0.03% and 0.20%. Enter these ultra-low expense ratios into the Mutual Fund Calculator and compare the results against actively managed alternatives to see the enormous long-term cost advantage of passive index investing.

Sector Funds concentrate investments in a specific industry — technology, healthcare, energy, real estate. These funds carry higher risk but potentially higher returns. Use the Mutual Fund Calculator conservatively when modeling sector funds — use a return assumption that accounts for the higher volatility of concentrated sector exposure.

Common Mistakes to Avoid When Using a Mutual Fund Calculator

Avoid these frequent errors to ensure your Mutual Fund Calculator results are accurate and actionable:

Mistake 1 — Using the gross return instead of netting out the expense ratio. Some investors enter the fund’s advertised gross return without adjusting for the operating expense ratio. The Mutual Fund Calculator automatically deducts the expense ratio from your rate of return — but only if you enter the expense ratio accurately. Never leave this field at zero unless the fund truly has no expenses.

Mistake 2 — Ignoring the sales charge on the initial investment. A 3% front-end load on a $20,000 investment means only $19,400 is actually invested. Every dollar lost to the sales charge is a dollar that never compounds. Always enter the exact sales charge from the fund’s prospectus — do not round down or ignore it.

Mistake 3 — Entering unrealistically high return assumptions. It is tempting to enter 12% or 15% to see exciting projected numbers. But the Mutual Fund Calculator is most valuable when you use realistic, conservative return assumptions. A projection based on 8% that is achievable is worth far more than a projection based on 15% that never materializes.

Mistake 4 — Not modeling monthly contributions. Many investors run the Mutual Fund Calculator with only the initial investment and ignore the power of regular monthly contributions. Even $100 or $200 per month, compounded over 15 to 20 years, adds tens of thousands of dollars to your ending value. Always model your realistic ongoing contributions.

Mistake 5 — Running only one scenario. The Mutual Fund Calculator is most powerful when used comparatively. Running one scenario and accepting the result misses the tool’s greatest capability — the ability to compare multiple funds, multiple fee structures, multiple contribution levels, and multiple holding periods side by side to identify the optimal investment strategy for your specific situation.

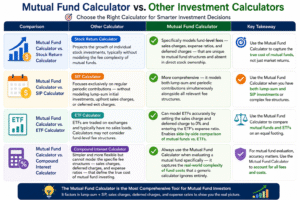

Mutual Fund Calculator vs. Other Investment Calculators

Understanding when to use a Mutual Fund Calculator versus other financial calculators helps you choose the right tool for every planning decision:

Mutual Fund Calculator vs. Stock Return Calculator. A stock return calculator projects the growth of individual stock investments, typically without modeling the fee complexity of mutual funds. The Mutual Fund Calculator specifically models fund-level fees — sales charges, expense ratios, and deferred charges — that are unique to mutual fund structures and absent in direct stock ownership.

Mutual Fund Calculator vs. SIP Calculator. A Systematic Investment Plan (SIP) calculator focuses exclusively on regular periodic contributions — without modeling lump-sum initial investments, upfront sales charges, or deferred exit charges. The Mutual Fund Calculator is more comprehensive — it models both lump-sum and periodic contributions simultaneously alongside all relevant fee structures.

Mutual Fund Calculator vs. ETF Calculator. Exchange-traded funds (ETFs) share many characteristics with mutual funds but are traded on exchanges and typically have no sales loads. The Mutual Fund Calculator can model ETFs accurately by setting the sales charge and deferred charge to 0% and entering the ETF’s expense ratio. This makes side-by-side comparison of mutual funds versus ETFs straightforward.

Mutual Fund Calculator vs. Compound Interest Calculator. A generic compound interest calculator is simpler and more flexible but cannot model the specific fee structures — sales charges, deferred charges, and expense ratios — that define the true cost of mutual fund investing. Always use the Mutual Fund Calculator when evaluating a mutual fund specifically — it captures the real-world complexity of fund costs that a generic calculator ignores entirely.

Frequently Asked Questions (FAQs)

Q1: What does a Mutual Fund Calculator calculate?

A Mutual Fund Calculator calculates the projected ending value of your mutual fund investment, your total principal invested, your total contributions, the total fees and charges deducted, and your net return — all based on your specific inputs including initial investment, contributions, rate of return, holding period, and all applicable fee structures.

Q2: How accurate is a Mutual Fund Calculator?

A Mutual Fund Calculator is highly accurate for planning purposes when you enter realistic inputs. It applies mathematical compound growth formulas precisely. However, it cannot predict actual future market performance — the “rate of return” you enter is an assumption, not a guarantee. Use conservative return assumptions to build a realistic rather than optimistic financial plan.

Q3: What is a good rate of return to enter in a Mutual Fund Calculator?

For long-term equity mutual funds, 6% to 8% per year is a widely used conservative assumption based on historical market averages. For bond funds, 3% to 5% is more appropriate. For balanced funds, 5% to 7% is a reasonable midpoint. Always use a rate that reflects the realistic long-term performance expectation of the specific fund type you are evaluating.

Q4: Why do fees matter so much in mutual fund investing?

Because fees reduce the capital that compounds over time. Every dollar paid in fees is a dollar that can never earn compound returns for the remaining years of your holding period. A 1% higher expense ratio may sound small, but over 20 years on a growing portfolio, it can cost you 20% or more of your total accumulated wealth. The Mutual Fund Calculator makes this compounding fee cost visible with exact dollar figures.

Q5: What is the difference between a sales charge and an expense ratio in the Mutual Fund Calculator?

A sales charge (front-end load) is a one-time fee deducted when you first buy the fund — it reduces your initial invested principal immediately. An expense ratio is an annual ongoing fee deducted from fund returns every single year throughout your holding period. Both erode your total returns, but the expense ratio’s impact grows over time due to compounding while the sales charge’s impact is fixed at purchase. The Mutual Fund Calculator models both accurately.

Q6: Can I use a Mutual Fund Calculator to compare two different funds?

Yes — and this is one of the most valuable uses of the Mutual Fund Calculator. Enter the same initial investment, contributions, holding period, and rate of return for both funds, but enter their different fee structures separately. Compare the resulting net returns side by side. The fund with the lower total fees almost always delivers the higher net return — even if both funds earn the same gross return before fees.

Q7: Should I choose a no-load mutual fund based on the Mutual Fund Calculator results?

In most cases, the Mutual Fund Calculator will show that no-load funds outperform loaded funds with identical return rates and holding periods — because the full initial investment enters the fund without deduction and compounds from day one. However, if a loaded fund delivers consistently higher gross returns that exceed the cost of the load and higher expense ratio, it may still be a competitive option. Always run both through the Mutual Fund Calculator to compare actual net results rather than making assumptions.

Q8: How often should I use a Mutual Fund Calculator?

Use a Mutual Fund Calculator every time you make a mutual fund decision — when selecting a new fund, when reviewing your portfolio annually, when considering increasing contributions, or when comparing your current funds against lower-cost alternatives. It is not a one-time tool. Regular use of the Mutual Fund Calculator keeps your investment strategy aligned with your actual financial goals and ensures you are never silently losing wealth to avoidable fees.

Conclusion

Mutual funds remain one of the most accessible, diversified, and professionally managed investment vehicles available to ordinary investors.

But the difference between a good mutual fund investment and a great one — or between a cost-efficient fund and an expensive one — can represent hundreds of thousands of dollars over a long investment lifetime.

The Mutual Fund Calculator gives you the power to see those differences before you commit your money.

It shows you exactly how fees compound against you over time. It reveals the true power of consistent monthly contributions. It demonstrates the extraordinary wealth-building advantage of longer holding periods. And it empowers you to compare fund options with mathematical precision rather than marketing claims.

Use the Mutual Fund Calculator every time you evaluate a new fund. Use it when you review your existing portfolio annually. Use it when you consider increasing your contributions. And use it when comparing actively managed funds against low-cost passive index alternatives.

Every smart mutual fund decision starts with running the numbers. And running the numbers starts with a Mutual Fund Calculator.

Your financial future is too important to leave to guesswork. Start calculating today.