Estimate returns, plan your wealth, and grow money instantly with smart financial calculations – Investment Calculator

Table of Contents

- Introduction

- What Is an Inflation Calculator?

- Why Inflation Matters More Than Most People Realize

- How an Inflation Calculator Works

- Future Cost Projection (Forward Inflation)

- Historical Buying Power Analysis (Backward Inflation)

- Personal Inflation Rate — Your Own Financial Reality

- How to Use an Inflation Calculator Effectively

- The Real Impact of Inflation on Savings and Investments

- How to Protect Your Wealth Against Inflation

- Inflation vs. Interest Rates — Understanding the Connection

- Common Inflation Myths Debunked

- Who Should Use an Inflation Calculator?

- Frequently Asked Questions (FAQs)

- Conclusion

Introduction

Every year, without making a single bad financial decision, millions of people silently lose purchasing power. The culprit is inflation — the slow, relentless rise in the cost of goods and services that erodes the real value of your money over time. An Inflation Calculator is the most direct and honest tool available to measure this invisible force and understand exactly how it is affecting your finances. Whether you want to project the future cost of your current expenses, analyze what a past sum of money is worth today, or measure your own personal inflation rate — an Inflation Calculator gives you clear, actionable answers. In this comprehensive guide, we cover everything you need to know about inflation, how it works, how to calculate it, and — most importantly — what you can do to protect your wealth from its relentless impact.

What Is an Inflation Calculator?

An Inflation Calculator is a financial tool that quantifies the impact of inflation on the value of money over a specified period. It uses a standard compound formula to show how the purchasing power of a given amount changes when exposed to a consistent annual inflation rate across multiple years. Unlike vague economic headlines, an Inflation Calculator translates abstract inflation percentages into concrete dollar figures that directly relate to your life.

A well-designed Inflation Calculator typically offers three distinct modes of analysis. The first is forward projection — you enter a current amount, an expected inflation rate, and a number of years, and the tool tells you how much that same goods or service will cost in the future. The second is backward analysis — you enter a historical amount and the tool reveals how much it would be equivalent to in today’s purchasing power. The third and most personal mode is the personal inflation basket — where you enter your actual spending across categories like housing, food, and utilities, and the tool calculates your own unique, personalized inflation rate.

Together, these three modes give you a 360-degree view of how inflation has affected your past, is affecting your present, and will affect your future.

Why Inflation Matters More Than Most People Realize

Inflation is often dismissed as a distant economic concept — something governments and central banks deal with, not something that directly impacts everyday financial decisions. This misunderstanding is one of the most expensive financial mistakes a person can make.

Consider this: at a modest 5% annual inflation rate, the purchasing power of $1,000 drops to approximately $614 in just 10 years. You have not spent a single dollar. You have not made a single bad investment. Yet nearly 40% of your money’s value has quietly disappeared. This is why financial experts call inflation “the silent tax.” It is invisible, it is constant, and it spares no one.

An Inflation Calculator makes this invisible force visible. It forces you to confront the real numbers rather than a comforting but dangerously false sense that “your money is safe in the bank.” Here is why understanding inflation is non-negotiable:

- Savings accounts lose real value: A savings account earning 2% annual interest in a 5% inflation environment is actually losing 3% of real value every single year.

- Salaries need to beat inflation: If your salary grows by 3% annually but inflation runs at 5%, you are effectively taking a 2% pay cut in real terms.

- Retirement planning depends on it: Retirement savings that look comfortable today may be dangerously inadequate 20 years from now without inflation adjustments.

- Major purchases require inflation-adjusted budgeting: The cost of a home, a car, or a child’s education in 15 years will be dramatically higher than today’s prices.

An Inflation Calculator gives you the numbers to make smarter decisions across all of these areas.

How an Inflation Calculator Works

The mathematics behind an Inflation Calculator is straightforward but powerful. It uses the compound inflation formula — the same compounding principle that drives investment growth, but applied in reverse to show the erosion of purchasing power.

Future Value = Present Value × (1 + Inflation Rate)^Years

Where:

- Future Value = How much something will cost in the future

- Present Value = Today’s cost or amount

- Inflation Rate = Annual inflation rate (as a decimal)

- Years = Number of years into the future

For example: If a monthly grocery bill today is $300 and inflation averages 5% annually, in 10 years that same basket of groceries will cost:

$300 × (1 + 0.05)^10 = $300 × 1.6289 = $488.67

That is an increase of nearly $189 per month — or over $2,200 per year — just to buy the same groceries. An Inflation Calculator runs this calculation instantly for any amount, rate, and time period you choose.

Future Cost Projection (Forward Inflation)

The future cost projection mode of an Inflation Calculator is the most commonly used feature, and for good reason — it directly answers the question every financial planner must address: “How much will things cost in the future?”

You enter three inputs: your current amount or cost, your expected annual inflation rate, and the number of years into the future. The Inflation Calculator then shows you the projected future cost, the total increase in dollar terms, the percentage increase, and — in more detailed versions — a year-by-year breakdown of how costs escalate.

This feature is invaluable for planning major life expenses such as:

- Education costs: University tuition is rising at 4–6% annually in many countries. A degree that costs $30,000 today may cost $48,000+ in 10 years.

- Healthcare expenses: Medical inflation consistently outpaces general inflation. Use an Inflation Calculator with a higher rate (6–8%) when planning for future healthcare costs.

- Housing and rent: Property values and rents in urban areas often rise faster than headline CPI. Model these separately with appropriate rates.

- Retirement income needs: The income that feels comfortable today will need to be significantly higher in real terms 20–30 years from now.

The key insight from forward inflation projection is simple: plan for higher costs tomorrow, always. Any financial plan that does not account for future inflation is built on a dangerously false foundation.

Historical Buying Power Analysis (Backward Inflation)

The backward inflation mode of an Inflation Calculator answers a different but equally important question: “What was a historical sum of money actually worth in today’s terms?”

This analysis is essential for understanding historical financial data in proper context. When someone says “$50,000 was a great salary in 1990,” the Inflation Calculator reveals that $50,000 in 1990 had the same purchasing power as approximately $115,000 in 2024 — a fact that completely changes the interpretation of the original figure.

You enter three inputs: the historical amount, the average inflation rate over the period, and the number of years in the past. The tool calculates both the equivalent value in today’s money and the total purchasing power that has been lost to inflation over the period.

Practical uses for backward inflation analysis include:

- Comparing historical salaries and costs: Understanding whether your income today is genuinely higher in real terms than a historical figure

- Evaluating old investments: Determining whether an investment that doubled in nominal terms over 20 years actually outpaced inflation

- Estate planning: Understanding the real value of historical inheritances or property purchases relative to today’s prices

- Policy analysis: Evaluating whether government benefits, pensions, or minimum wages have kept pace with real-world inflation over time

Personal Inflation Rate — Your Own Financial Reality

The most underused and most revealing feature of an advanced Inflation Calculator is the personal inflation basket. Government inflation statistics — whether the Consumer Price Index (CPI) or the Retail Price Index (RPI) — measure price changes across a standardized basket of goods for an average consumer. But you are not an average consumer. Your spending pattern is unique, and your personal inflation rate may be dramatically different from the headline number.

In the personal inflation mode of an Inflation Calculator, you enter your actual spending across major categories — housing, food, utilities, healthcare, transportation, and more — for both the previous year and the current year. The tool calculates a weighted inflation rate that reflects your specific cost-of-living increase, not the government’s average.

Why does this matter? Consider two people:

- Person A spends heavily on housing and groceries in a high-cost urban area. Their personal inflation rate may be 7–8% even when headline CPI reads 4%.

- Person B owns their home outright and grows some of their own food. Their personal inflation rate may be only 2–3%.

Government statistics cannot capture this difference — but a personal Inflation Calculator can. Knowing your actual personal inflation rate allows you to:

- Set a realistic salary increase target that genuinely preserves your purchasing power

- Adjust your savings rate to account for your specific cost-of-living pressures

- Identify which spending categories are inflating fastest and take targeted action

- Build a retirement income plan based on your real lifestyle costs, not average statistics

How to Use an Inflation Calculator Effectively

Getting maximum insight from an Inflation Calculator requires more than entering numbers and reading results. Here is a strategic approach:

Use realistic, category-specific rates. Do not apply a single blanket inflation rate to all future expenses. Healthcare, education, housing, and food all inflate at different rates. Use an Inflation Calculator separately for each major expense category with the appropriate rate.

Run multiple time horizons. Calculate the inflation impact at 5, 10, 20, and 30 years. The difference between a 10-year and 30-year projection is often shocking — and it reveals just how critical early action is.

Combine forward and backward analysis. Use the backward mode to validate your understanding of historical inflation, then use the forward mode to project future costs. Together, they give you a complete picture of inflation’s trajectory.

Update your calculations annually. Inflation rates change. Central bank policies shift. Recalculate your projections every year with current inflation data to keep your financial plan accurate and relevant.

Use the personal basket feature regularly. Track your own spending categories year over year and calculate your personal inflation rate annually. This is the most honest measure of your actual financial pressure.

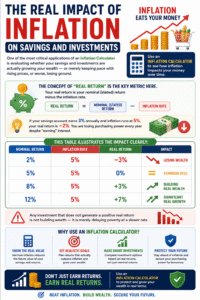

The Real Impact of Inflation on Savings and Investments

One of the most critical applications of an Inflation Calculator is evaluating whether your savings and investments are actually growing your wealth — or merely keeping pace with rising prices, or worse, losing ground.

The concept of “real return” is the key metric here. Your real return is your nominal (stated) return minus the inflation rate. If your savings account earns 3% annually and inflation runs at 5%, your real return is −2%. You are losing purchasing power every year despite “earning” interest.

This table illustrates the impact clearly:

| Nominal Return | Inflation Rate | Real Return | Impact |

|---|---|---|---|

| 2% | 5% | −3% | Losing wealth |

| 5% | 5% | 0% | Standing still |

| 8% | 5% | +3% | Building real wealth |

| 12% | 5% | +7% | Significant real growth |

Any investment that does not generate a positive real return is not building wealth — it is merely delaying poverty at a slower rate. This is why an Inflation Calculator should be used alongside any investment calculator to ensure that projected returns genuinely outpace inflation.

How to Protect Your Wealth Against Inflation

Understanding inflation through an Inflation Calculator is only the first step. The second — and more important — step is taking concrete action to protect your purchasing power. Here are the most effective inflation-protection strategies:

Invest in equities. Stocks represent ownership in real businesses that can raise prices as inflation rises, protecting their earnings and your investment. Historically, broad equity markets have delivered returns of 7–10% annually — well above long-term inflation averages.

Hold real assets. Real estate, commodities, and infrastructure tend to appreciate with inflation because they are physical assets with intrinsic value. As prices rise, so does the value of tangible property.

Consider inflation-linked bonds. Treasury Inflation-Protected Securities (TIPS) in the US — and similar instruments in other countries — are bonds whose principal value is automatically adjusted for inflation, guaranteeing a positive real return.

Maximize income growth. Negotiate salary increases that at minimum match your personal inflation rate calculated through an Inflation Calculator. A raise that does not beat your personal inflation rate is a hidden pay cut.

Diversify globally. Different countries experience different inflation rates. International diversification of investments provides a natural hedge against domestic inflation surges.

Reduce fixed-rate debt. Inflation actually benefits borrowers with fixed-rate loans — the real value of your debt decreases as prices rise. Keeping a manageable fixed-rate mortgage during an inflationary period can actually work in your favor.

Inflation vs. Interest Rates — Understanding the Connection

A complete understanding of how to use an Inflation Calculator requires understanding the relationship between inflation and interest rates. These two forces are deeply intertwined, and their interaction has profound effects on savings, borrowing, and investment returns.

When inflation rises, central banks typically raise interest rates to slow economic activity and reduce upward price pressure. Higher interest rates make borrowing more expensive, which reduces spending and slows inflation over time.

For investors, this relationship creates important dynamics:

- Rising inflation erodes bond values: Existing bonds with fixed rates become less attractive when new bonds offer higher yields, causing their market price to fall.

- Cash and savings accounts benefit temporarily: Higher interest rates mean higher savings account yields — but only if those yields exceed the inflation rate does real value actually grow.

- Equity markets experience volatility: Higher rates increase borrowing costs for companies, compressing profit margins and often causing short-term stock market declines.

Use an Inflation Calculator alongside current interest rate data to evaluate whether the real yield on any cash or fixed-income holding is positive or negative. If your savings rate is lower than inflation, you are losing real money regardless of the nominal interest earned.

Common Inflation Myths Debunked

Many people hold misconceptions about inflation that lead to poor financial decisions. Here are the most common myths — and the truth an Inflation Calculator reveals:

Myth: “Inflation only affects the poor.”

Truth: Inflation affects everyone whose assets are held primarily in cash or low-yield savings. The wealthy are often better protected because they hold real assets and equities that appreciate with inflation. Cash-heavy savers at all income levels are equally vulnerable.

Myth: “2–3% inflation is harmless.”

Truth: At 3% annual inflation, the purchasing power of $100,000 drops to approximately $74,000 in just 10 years. An Inflation Calculator makes clear that even “low” inflation causes severe long-term erosion. Over 30 years, 3% inflation cuts purchasing power by nearly 60%.

Myth: “My salary has kept up with inflation.”

Truth: Most people do not track this rigorously. Use an Inflation Calculator to compare your salary in a prior year to its equivalent today and compare it to your actual current salary. The result is often sobering.

Myth: “Inflation is predictable and stable.”

Truth: Inflation is influenced by dozens of interacting factors — energy prices, supply chains, monetary policy, geopolitical events, and consumer behavior. Projections are always estimates. Use your Inflation Calculator with conservative, moderate, and aggressive inflation scenarios to plan for a range of outcomes.

Who Should Use an Inflation Calculator?

The honest answer is: everyone. But here are the groups for whom an Inflation Calculator is particularly indispensable:

- Retirees and near-retirees: Planning a fixed income in retirement without accounting for inflation is a serious financial risk. An Inflation Calculator is the most important tool in retirement income planning.

- Parents planning for children’s education: University costs are rising faster than general inflation. Start projecting now.

- Employees negotiating salary increases: Know your personal inflation rate before you walk into any salary negotiation.

- Small business owners: Understanding how rising input costs compound over time is critical for pricing strategy and long-term business planning.

- First-time investors: Before choosing any investment vehicle, use an Inflation Calculator to verify whether its projected return genuinely outpaces inflation.

- Anyone with significant cash savings: If you are holding large amounts in a savings account, you need to see the real cost of that decision in inflation-adjusted terms.

Frequently Asked Questions (FAQs)

What is an Inflation Calculator used for?

An Inflation Calculator is used to measure how inflation affects the value of money over time. It can project the future cost of current expenses, reveal the equivalent purchasing power of historical amounts in today’s money, and calculate your personal inflation rate based on actual spending data.

How accurate is an Inflation Calculator?

An Inflation Calculator is as accurate as the inflation rate you input. Official calculators using historical CPI data are highly accurate for past projections. Future projections are estimates — always run calculations with conservative, moderate, and high inflation scenarios to understand your full range of risk.

What is a good inflation rate to use for future projections?

For general planning purposes, many financial advisors recommend using 3–4% for developed economies as a baseline. For specific categories like healthcare or education, use higher rates (5–7%). For developing economies, rates of 6–10% are often more realistic.

How does inflation affect retirement savings?

Inflation is one of the most critical risks in retirement planning. A retiree on a fixed income loses real purchasing power every year inflation rises. An Inflation Calculator helps you determine how much your retirement savings will actually be worth in 20–30 years and how much income you truly need to maintain your current lifestyle.

Can I calculate my own personal inflation rate?

Yes. An Inflation Calculator with a personal basket feature allows you to enter your actual spending across categories for two consecutive years. The tool calculates your weighted personal inflation rate — which is almost always different from the official government CPI figure.

How often should I use an Inflation Calculator?

At minimum, revisit your Inflation Calculator projections once per year. Update your inputs with current inflation data, revised spending figures, and any changes to your financial goals. Annual recalculation keeps your financial plan accurate and your expectations realistic.

Is inflation always bad for everyone?

Not entirely. Borrowers with fixed-rate debt benefit from inflation because the real value of their debt decreases over time. Owners of real assets like property also benefit as asset values rise with inflation. However, cash savers and fixed-income earners are consistently harmed by inflation — which is why using an Inflation Calculator regularly is so important for protecting your financial position.

Conclusion

Inflation does not announce itself. It does not send warnings or ask permission. It simply works — quietly, consistently, and relentlessly — reducing the real value of money year after year. The only defense against an invisible force is the ability to see it clearly, measure it accurately, and plan around it intelligently.

An Inflation Calculator is that defense. It transforms abstract percentages into concrete dollar figures. It shows you the true future cost of today’s expenses. It reveals the real purchasing power of historical amounts. And it gives you your own personal inflation rate — the most honest measure of your actual financial reality.

Use an Inflation Calculator to project your costs forward. Use it to understand your past. Use it to measure your own inflation experience. And most importantly, use the insights it provides to build an investment and savings strategy that generates genuine real returns — returns that outpace inflation and build actual, enduring wealth.

The money you save today is only as valuable as the purchasing power it retains tomorrow. Measure it. Protect it. Grow it. Start with an Inflation Calculator — and stay one step ahead of the silent tax that no one can escape.