| Age | Total Invested | Ending Balance |

|---|

| Age | Total Injected | Projected Value |

|---|

| Age | If Untouched | After Cashout |

|---|

| Age | Total Injected | Actual Balance |

|---|

Watch your money grow faster with our easy-to-use Compound Interest Calculator

Table of Contents

- Introduction

- What Is a 401k Calculator?

- Why Every Working American Needs a 401k Calculator

- Understanding How a 401(k) Plan Works

- Key Inputs in a 401k Calculator Explained

- How to Use the 401k Calculator Step by Step

- The Power of Employer Matching: Free Money You Cannot Afford to Miss

- Understanding Your Results: Growth, Projection, and Withdrawal

- The Role of Compound Interest in 401(k) Growth

- How Contribution Rate Changes Your Retirement Balance

- Real-Life Scenarios Using the 401k Calculator

- 401(k) Withdrawal Planning: Making Your Money Last

- Common Mistakes to Avoid in 401(k) Planning

- Strategies to Maximize Your 401(k) Balance

- Frequently Asked Questions (FAQs)

- Conclusion

Introduction

Retirement may feel like a distant concern when you are young and focused on your career, your family, and the demands of daily life — but the financial decisions you make today will determine the quality of life you enjoy decades from now. The single most powerful tool available to most American workers for building retirement wealth is the 401(k) plan — and the single most powerful tool for understanding and optimizing that plan is a 401k Calculator.

A 401k Calculator transforms abstract retirement planning into concrete, personalized projections. It shows you exactly what your account will be worth at retirement, how much employer matching adds to your total, and what impact even small changes in your contribution rate can make over time. Whether you are 25 and just starting your career, or 50 and realizing you need to accelerate your savings, a 401k Calculator gives you the clarity to act with confidence.

In this comprehensive guide, we will cover everything you need to know — from the basic mechanics of a 401(k) plan to advanced strategies for maximizing your balance, understanding employer matches, planning withdrawals, and avoiding the costly mistakes that derail so many retirement savers. By the end, you will know exactly how to use a 401k Calculator to take full control of your financial future.

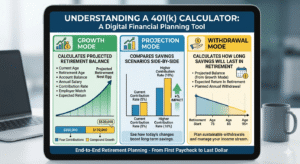

What Is a 401k Calculator?

A 401k Calculator is a digital financial planning tool that projects how much money you will accumulate in your 401(k) retirement account by the time you retire, based on your current balance, contribution rate, employer match, expected return, and investment timeframe.

A well-designed 401k Calculator typically operates across two or more modes:

Growth Mode — This calculates your projected retirement balance based on inputs like your current age, retirement age, existing account balance, annual salary, contribution rate, employer matching terms, and expected annual return. It shows you exactly what your 401(k) will be worth at retirement and breaks down how much came from your contributions versus compound investment growth.

Projection Mode — This compares scenarios side by side — for example, your current contribution rate versus a higher rate — to show you the long-term impact of changing your savings behavior today.

Withdrawal Mode — This calculates how long your retirement savings will last based on your projected balance, expected return in retirement, and planned annual withdrawal amount.

Together, these three modes make the 401k Calculator an end-to-end retirement planning tool — from your very first paycheck contribution to the final dollar drawn in retirement.401k calculator401k calculator401k calculator

Why Every Working American Needs a 401k Calculator

Most Americans are dangerously underprepared for retirement. Studies consistently show that the majority of workers have saved less than $100,000 for retirement — a fraction of what is typically needed to fund 20 to 30 years of post-work life. A large part of this problem is not a lack of earning potential — it is a lack of clarity about where you stand and what you need to do.

A 401k Calculator solves this clarity problem immediately. Here is why it is indispensable:

It shows you the real numbers. Instead of vague reassurances that “you should be saving more,” the 401k Calculator shows you your exact projected balance at retirement — and whether it is enough.

It makes the cost of inaction visible. Seeing that delaying your 401(k) enrollment by five years could cost you $200,000 or more in final balance is a powerful motivator that no general financial advice can replicate.

It quantifies employer matching. Many workers do not fully understand how valuable employer matching is. The 401k Calculator shows you in exact dollars how much free money you are leaving on the table if you contribute below the match threshold.

It helps you set a realistic retirement target. By working backwards from a desired retirement income, the 401k Calculator tells you precisely what contribution rate, return rate, and timeline will get you there.

It removes anxiety with knowledge. Financial uncertainty is one of the leading sources of stress for working adults. Replacing uncertainty with accurate projections — even if the numbers need work — is always better than not knowing.

Understanding How a 401(k) Plan Works

Before getting the most out of your 401k Calculator, it helps to understand the mechanics of the plan itself.

A 401(k) is an employer-sponsored retirement savings plan that allows employees to contribute a portion of their pre-tax salary to investment accounts. These contributions reduce your taxable income in the year they are made — meaning you pay less tax now, while your money grows tax-deferred until withdrawal in retirement.

Key features of a traditional 401(k):

Pre-tax contributions. Every dollar you contribute reduces your taxable income. If you are in the 22% tax bracket and contribute $5,000, you effectively save $1,100 in taxes in that year.

Tax-deferred growth. All investment returns inside the account — dividends, capital gains, and interest — accumulate without being taxed annually, allowing the full compounding effect to work unimpeded.

Employer matching. Most employers offer to match a portion of employee contributions up to a certain percentage of salary. This is effectively free money added to your retirement account.

Contribution limits. The IRS sets annual contribution limits. For 2024, the employee contribution limit is $23,000, with an additional $7,500 catch-up contribution allowed for those aged 50 and older.

Required Minimum Distributions (RMDs). Beginning at age 73, you must start taking minimum withdrawals from your traditional 401(k), whether you need the money or not.

A 401k Calculator accounts for all of these elements to produce projections that reflect how the plan actually works — not just a simplified interest calculation.

Key Inputs in a 401k Calculator Explained

The accuracy of your 401k Calculator results depends entirely on the quality of your inputs. Here is what each field means and how to fill it in correctly:

Current Age: Your age today. This determines how many years your money has to compound before retirement.

Retirement Age: The age at which you plan to stop working and begin drawing from your 401(k). Most Americans target ages between 60 and 67, depending on Social Security timing and personal preference.

Current Balance: The amount already in your 401(k) account today. If you are just starting, this is zero. If you have been contributing for years, enter your current account value.

Annual Salary: Your gross annual salary before taxes and deductions. This is used to calculate your dollar contribution based on your contribution percentage.

Contribution Rate: The percentage of your salary you contribute to your 401(k) each year. The 401k Calculator converts this to an annual dollar amount for projection purposes.

Employer Match Percentage: How much your employer matches — for example, 100% means they match dollar for dollar.

Match Limit: The maximum percentage of your salary up to which the employer will match. A common structure is “100% match up to 4% of salary” — meaning you must contribute at least 4% to receive the full match.

Annual Return Rate: The expected average annual return on your 401(k) investments. A historically grounded estimate of 7-8% is appropriate for a diversified equity-heavy portfolio over long periods, though actual returns will vary.

How to Use the 401k Calculator Step by Step

Getting meaningful results from a 401k Calculator is straightforward when you approach it methodically. Here is the process:

Step 1 — Open the Growth tab. This is your primary projection tool. It will show you your projected balance at retirement based on your current situation.

Step 2 — Enter your current age and target retirement age. These two numbers define your investment horizon — the single most important variable in any retirement calculation.

Step 3 — Input your current balance. Even if it is zero, enter it accurately. The 401k Calculator needs this as the starting point for all projections.

Step 4 — Enter your annual salary and contribution rate. Start with your current actual contribution rate. You will adjust this later to test scenarios.

Step 5 — Fill in employer matching details. Enter both the match percentage and the match limit to ensure the 401k Calculator adds the correct employer contribution to your annual total.

Step 6 — Set your expected return rate. Use 7-8% for a diversified long-term equity portfolio. Use a lower rate (4-5%) for more conservative allocations.

Step 7 — Click Calculate. The 401k Calculator will display your projected retirement balance, a breakdown of principal versus growth, and a year-by-year table showing your age, total invested, and ending balance at each milestone.

Step 8 — Switch to the Projection tab. Test alternative contribution rates and compare projected outcomes side by side to find the contribution strategy that works best for your budget and retirement goals.

Step 9 — Use the Withdrawal tab. Once you know your projected balance, model how long it will last based on different withdrawal rates and post-retirement return assumptions.

The Power of Employer Matching: Free Money You Cannot Afford to Miss

If there is one single insight that the 401k Calculator delivers most powerfully, it is the extraordinary value of employer matching. Employer matching is the closest thing to guaranteed, risk-free, instant return on investment that exists in personal finance — and yet millions of workers fail to capture it fully.

Here is a concrete example: You earn $80,000 per year. Your employer offers a 100% match on contributions up to 4% of salary. That means if you contribute 4% ($3,200), your employer adds another $3,200 — a 100% instant return on that portion of your contribution before a single dollar of investment growth is added.

If you contribute only 3% instead of 4%, you leave $800 in employer matching uncaptured every single year. Over 30 years, with 8% growth, that uncaptured $800 per year compounds to over $97,000 in lost retirement savings.

The 401k Calculator makes this calculation instantly visible. You can see the exact difference between contributing at, below, and above the match threshold — and the results are invariably compelling enough to motivate maximum matching capture.

The absolute first priority for any 401(k) participant is to contribute at least enough to capture the full employer match. The 401k Calculator shows you exactly where that threshold is and what it means for your final balance.

Understanding Your Results: Growth, Projection, and Withdrawal

Once the 401k Calculator produces your results, here is how to interpret each element:

Total Principal Invested is the combined total of all your contributions and all employer matching contributions over your working career. This represents the real money that entered your account.

Compound Interest Yield is the investment growth generated purely by your portfolio returns — the money your money made. In long-term 401(k) projections, this figure typically equals or exceeds total principal invested by a significant margin, which is the central argument for starting early and contributing consistently.

Projected Retirement Balance is your estimated total account value at your target retirement age. This is the headline number — but it is important to contextualize it against your projected retirement spending needs.

The year-by-year table shows your estimated ending balance at every age milestone. This granular view reveals the accelerating nature of compound growth — early years show modest growth, while the final decade before retirement often produces the largest absolute dollar increases, even with the same contribution rate.

The visual progress bars show the proportion of your final balance attributable to principal versus growth — a powerful reminder that investment returns, not just contributions, are the real engine of retirement wealth.

The Role of Compound Interest in 401(k) Growth

Compound interest is the engine that transforms a lifetime of 401(k) contributions into genuine retirement wealth. Without compounding, the typical American’s 401(k) contributions would produce a modest sum. With compounding over 30 to 40 years, those same contributions can produce a portfolio worth ten times the amount actually deposited.

Here is an illustration using the 401k Calculator:

Starting at age 30 with a $50,000 balance, contributing 7% of an $80,000 salary ($5,600/year) with a 100% employer match up to 4% ($3,200/year employer contribution) at 8% annual return until age 65:

- Total employee contributions over 35 years: approximately $196,000

- Total employer matching over 35 years: approximately $112,000

- Total principal invested: approximately $308,000

- Compound interest yield: approximately $1,100,000+

- Projected retirement balance: approximately $1,400,000+

Over 70% of the final balance comes from compound investment growth — not from contributions. This is the defining insight of long-term 401(k) planning, and it is the single most compelling argument for starting contributions as early as possible and maintaining them consistently throughout your career.

How Contribution Rate Changes Your Retirement Balance

One of the most revealing features of the 401k Calculator is its ability to show you exactly how changing your contribution rate — even by 1 or 2 percentage points — transforms your retirement outcome.

Using the same profile above ($80,000 salary, age 30, $50,000 balance, 8% return, retiring at 65):

| Contribution Rate | Annual Contribution | Projected Balance |

|---|---|---|

| 4% | $3,200 | ~$1,100,000 |

| 7% | $5,600 | ~$1,400,000 |

| 10% | $8,000 | ~$1,700,000 |

| 15% | $12,000 | ~$2,200,000 |

Each additional percentage point of contribution adds roughly $100,000 to $150,000 to the final retirement balance when invested over a 35-year period. The 401k Calculator makes this arithmetic vivid and immediate — converting an abstract percentage into a concrete dollar impact that is impossible to ignore.

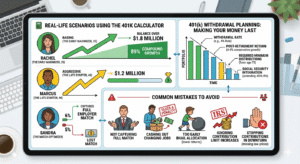

Real-Life Scenarios Using the 401k Calculator

Scenario 1 — The Early Maximizer: Rachel starts her career at 25, earns $65,000, contributes 10% with a 4% employer match, at 7% annual return. Her 401k Calculator projection to age 65 shows a balance exceeding $1.8 million — built on total contributions of just over $200,000. Compound growth accounts for nearly 90% of her final balance.

Scenario 2 — The Late Starter Who Catches Up: Marcus begins contributing to his 401(k) at age 40 with a $30,000 existing balance. He earns $95,000, contributes 15%, receives a 3% employer match, at 7% return. His 401k Calculator projection to age 67 shows a balance of approximately $1.2 million — proof that even late starters can build significant retirement wealth with aggressive contributions.

Scenario 3 — The Match Optimizer: Sandra earns $70,000. Her employer offers a 50% match on contributions up to 6%. She uses the 401k Calculator to discover that contributing exactly 6% ($4,200) generates $2,100 in employer matching — and that dropping to 5% costs her over $700 in annual matching. She immediately adjusts her contribution rate to capture the full match.

401(k) Withdrawal Planning: Making Your Money Last

Building a large 401(k) balance is only half the challenge. Making that balance last through 20 to 30 years of retirement requires equally careful planning — and the withdrawal module of the 401k Calculator is designed specifically for this purpose.

Key factors in withdrawal planning include:

Withdrawal rate. Financial planners traditionally recommend the 4% rule — withdrawing no more than 4% of your balance in the first year of retirement, then adjusting for inflation annually. This strategy historically sustains a portfolio for 30+ years.

Post-retirement return rate. Once retired, most people shift to more conservative investments that earn lower returns. Use a rate of 4-6% for withdrawal planning, versus 7-8% for the accumulation phase.

Required Minimum Distributions. From age 73, you must withdraw a minimum amount each year regardless of whether you need it. The 401k Calculator can help you anticipate these distributions and their tax implications.

Social Security integration. Your Social Security income reduces the amount you need to draw from your 401(k), extending its lifespan significantly. Factor your expected Social Security benefit into your withdrawal planning for a complete picture.

Common Mistakes to Avoid in 401(k) Planning

Even with a powerful 401k Calculator at your disposal, these common mistakes can undermine your retirement outcome:

Not contributing enough to capture the full employer match. This is the most costly and common mistake in 401(k) planning. As shown earlier, leaving any employer match uncaptured costs you tens of thousands in lost retirement savings.

Cashing out when changing jobs. When you leave an employer, you have the option to roll over your 401(k) to a new employer’s plan or an IRA. Cashing it out triggers taxes plus a 10% early withdrawal penalty and destroys years of compounding. Always roll it over.

Using an overly conservative investment allocation too early. Young savers sometimes allocate too heavily to bonds and stable value funds out of fear of market volatility. Over a 30 to 40-year horizon, equities historically deliver far superior returns. The 401k Calculator assumes an 8% return based on equity-weighted allocations — make sure your actual portfolio allocation supports this assumption.

Ignoring contribution limit increases. The IRS increases 401(k) contribution limits periodically. Maximizing contributions up to the annual limit, especially as your income grows, can add hundreds of thousands of dollars to your final balance.

Stopping contributions during market downturns. Markets recover over time, and contributions made during downturns buy more shares at lower prices — amplifying future growth. Never stop contributing based on short-term market movements.

Strategies to Maximize Your 401(k) Balance

Now that you understand the mechanics and the common pitfalls, here are the most effective strategies for building maximum retirement wealth using the insights from your 401k Calculator:

Always capture the full employer match first. Before any other financial priority, contribute at least enough to your 401(k) to receive every dollar of available employer matching. This is your highest guaranteed return investment.

Increase contributions with every raise. When your salary increases, immediately increase your 401(k) contribution rate by at least half the raise amount. Your take-home pay still increases, but your retirement account accelerates.

Aim to max out annual contributions. Once your cash flow allows, target the IRS maximum contribution limit. For 2024, that is $23,000 — or $30,500 if you are 50 or older.

Take advantage of catch-up contributions. From age 50, you can contribute an extra $7,500 per year. Use the 401k Calculator to see how maximizing catch-up contributions affects your balance if you started saving late.

Choose a diversified equity-weighted allocation. Especially in your 20s, 30s, and 40s, allocate heavily to equities. The long time horizon absorbs volatility and delivers the compounding returns your 401k Calculator projects.

Consolidate old 401(k) accounts. If you have left old employer accounts behind, roll them into your current plan or a consolidating IRA. Scattered accounts are harder to manage, optimize, and track.

Revisit the 401k Calculator annually. Your salary, contribution rate, market returns, and retirement timeline all change over time. An annual recalculation ensures your strategy stays optimally aligned with your goals.

Frequently Asked Questions (FAQs)

What is the best age to start contributing to a 401(k)?

The best age is as young as possible — ideally the moment your employer offers the plan. The earlier you start, the more time compound growth has to work. Using a 401k Calculator, you can see that starting at 25 versus 35 can easily result in double the retirement balance, even with identical contribution rates and returns. Every year of early contribution is disproportionately valuable.

How much should I contribute to my 401(k)?

At minimum, contribute enough to capture your full employer match. Beyond that, a widely cited guideline is to save 15% of gross income for retirement, including employer matching. Use the 401k Calculator to determine exactly what contribution rate will produce your desired retirement balance given your specific age, salary, and timeline.

What is a good annual return rate to use in the 401k Calculator?

For a diversified equity-weighted portfolio over a long investment horizon, 7-8% is a historically grounded and commonly used estimate. More conservative portfolios (more bonds, fewer stocks) may average 4-6%. As you approach retirement and shift to more conservative allocations, reduce your assumed return rate in the 401k Calculator to reflect the change.

What happens to my 401(k) if I change jobs?

When you leave an employer, you have three options: roll over the balance to your new employer’s 401(k), roll it over to an Individual Retirement Account (IRA), or cash it out. Always roll it over — cashing out triggers income taxes plus a 10% penalty and permanently destroys the compounding trajectory. The 401k Calculator can show you exactly what that lost compounding costs over your remaining career.

How does the employer match work in the 401k Calculator?

You enter two values: the match percentage (e.g., 100%) and the match limit (e.g., 4% of salary). This means the employer matches 100% of your contributions up to 4% of your salary. If you contribute 7%, the employer still only matches on the first 4% — so the match limit is the critical threshold to hit. The 401k Calculator shows your exact annual employer contribution based on these parameters.

Can I contribute to a 401(k) and an IRA at the same time?

Yes. Contributing to a 401(k) does not prevent you from also contributing to a Traditional or Roth IRA, subject to income limits for deductibility. For 2024, the IRA contribution limit is $7,000 ($8,000 if aged 50+). Maxing both accounts significantly accelerates retirement savings beyond what the 401k Calculator shows for the 401(k) alone.

What is the 4% rule for withdrawals?

The 4% rule is a widely used retirement income guideline suggesting that withdrawing 4% of your portfolio in the first year of retirement, then adjusting annually for inflation, will sustain a 30-year retirement in most market scenarios. Use this rule in the withdrawal section of the 401k Calculator to determine whether your projected retirement balance will generate sufficient income to meet your needs throughout retirement.

Conclusion

Retirement security does not happen by accident — it is built through consistent contributions, smart strategy, and the clarity to understand exactly where you stand at every stage of your career. The 401k Calculator provides that clarity instantly, transforming complex retirement mathematics into actionable, personalized projections.

The key lessons are clear: Start contributing as early as possible. Always capture your full employer match — it is free money that compounds into hundreds of thousands of dollars over a career. Increase your contribution rate whenever your income grows. Stay invested through market volatility. And plan your withdrawals as carefully as you planned your contributions.

Whether you are just entering the workforce or approaching retirement, the 401k Calculator is the most important planning tool at your disposal. Run your numbers today. Understand what your current trajectory produces. Identify the adjustments that will make the biggest difference. And then act — because every year of delay in maximizing your 401(k) is a year of compound growth your future self will wish you had not missed.

Your retirement is not a distant abstraction — it is the financial destination toward which every working day is a step. Use the 401k Calculator to make sure you are heading in the right direction, at the right pace, with the right strategy.